In the world of small and medium-sized enterprises (SMEs), there is an increasing emphasis on efficiency and innovation in financial processes. The introduction of advanced features facilitates the day-to-day operations of these SMEs and allows them to focus on their primary business. This article will focus on the key features that SMEs can use in their day-to-day operations.

Categorisation of expenditure - business vs. retail

Personal Finance Management (PFM) has a different focus for retail and business. In a business environment, it offers customized categorisations for better financial management (e.g., approving expenses to subordinates, etc.). Expense categorisation provides a more detailed view of cash flows and helps the finance team in more effective budget planning. For example, with categorisation, a company can see that a large portion of the company's fuel spend is at a select network of gas stations and negotiate a discount there.

Czech fintech Fidoo allows companies to monitor their expenses and employee spending conveniently and easily. For example, it offers a prepaid card for temporary workers, so the employer does not have to worry about a temporary worker "draining" his account and still has his expenses under control.

Limiting transactions based on GPS location

GPS location-based transaction limiting is an innovative feature that provides businesses with increased control and security. This technology allows you to set rules for transactions based on a user's geographic location, which provides significant benefits for managing corporate spending. In practice, this means that transactions can be allowed or denied based on where an employee is located, increasing security, and preventing fraud.

Did you know your employee is travelling to Brno on business? It stands to reason that he or she could not have made the transaction in Berlin and therefore this likely fraudulent payment will be rejected.

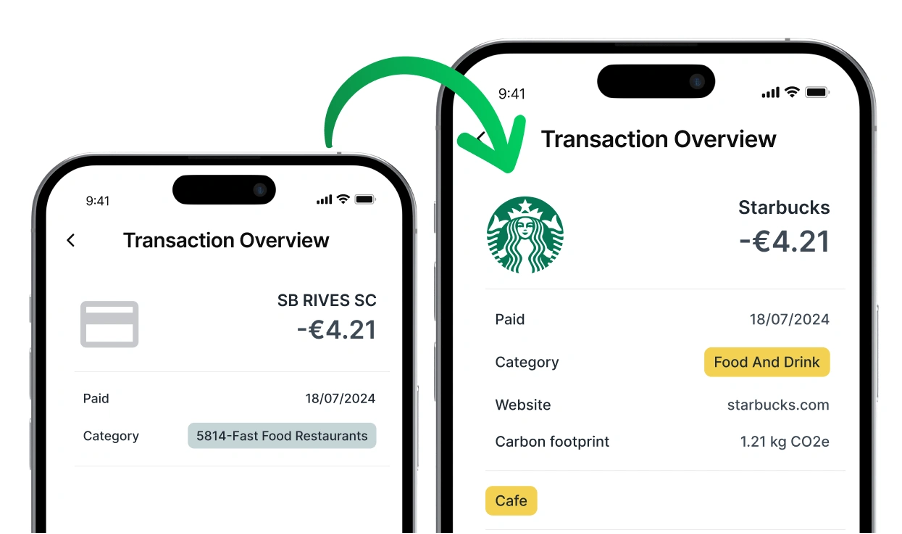

Emissions reporting and our EcoTrack tool

Today, the emphasis on sustainability and environmental responsibility is a major trend. EcoTrack enables banks to offer their SME clients the ability to track and report their Scope 3 emissions, which is key for businesses already struggling to reduce their environmental impact. This feature offers banks and fintechs to provide businesses with the tools to measure and manage their carbon footprint. This is important for the sustainability of the business, but also for their image and compliance with relevant regulations that already are or will be in place. All easily and conveniently managed directly from your banking app thanks to EcoTrack.

Tapix focuses on accurately estimating categories that go beyond transaction categorisation codes, delivering significant synergies. To do this, we use around 500 accompanying labels that enrich the category information and allow for a more detailed determination of CO2 multipliers.

Integration into the system is seamless and simple, with a single interface for data enrichment and CO2 tracking, a fully documented API.

As part of our carbon footprint tracking efforts, we focus on the merchant level, which sets us apart from others significantly. As our €50 spend example shows, simply categorising or using an MCC code could give us an incorrect estimate of our carbon footprint.

However, thanks to our detailed approach, we can say that the carbon footprint of this expenditure is only 2.3 kg CO2. This is key information for correct and meaningful reporting. Our target is still banks, but with our data, companies can build valid Scope 3 reporting for sustainability purposes. This ability to measure both traditional payments and remittances gives us a comprehensive view to better track our carbon footprint. For more information, you can view our graphics that illustrates our unique approach.

Scope 3 emissions cover a wide range of indirect emissions that arise in an organisation's value chain. Examples of emissions that you can easily track include:

- Purchased goods and services

- Transportation and distribution

- Business travel

We've excerpted from the Sustainability Yale report here for a more detailed look at each Scope 3 component.

Automated approval based on payments flow

Automating approval processes based on expenditure categories increases efficiency and reduces administrative burden. This feature allows you to set rules to automatically approve or reject expenses based on their category. The diversity of categories and their tags allows for better efficiency and, more importantly, automation. This means that routine expenses can be approved without the need for manual intervention, saving time and increasing productivity. For example, you can set up approvals for fuel purchases without the need for intervention. Conversely, you can be more careful with purchases from the Entertainment category.

UX and an example of a successful implementation at Soldo

User experience (UX) plays a key role in the adoption and success of payment applications. Fintech Soldo demonstrates how these new platforms combine intuitive UX design with advanced features such as categorisation, GPS transaction limits, budgeting.

Spend Heatmap of Employees

The functionality of the spend heatmap is that it graphically displays the areas where the biggest spend occurs, helping to identify key areas for potential savings. This visualization is organized by various parameters such as geographic location, type of spend or time period.

An example would be a company treasury manager's view of the data. The manager says: "It often happens that employees of our company pay for their accommodation at a Marriott hotel. That's why I try to negotiate a partner discount with that hotel. It helps me better understand where and how our company spends its funds, which can lead to more efficient expense management."

Tapix integration into SME banking

Integrating Tapix functionality into banking or payment systems targeting the SME segment can mean a significant improvement in the efficiency and security of financial management.

Integration may seem like a complex task, but in reality, it is not a difficult process. A key aspect is that Tapix is designed to be compatible with existing banking systems, which greatly reduces the complications associated with its implementation. Due to its flexibility and modular structure, Tapix allows for easy integration without the need for extensive customization or changes to existing infrastructure.

A detailed development overview can be found at developers.tapix.io