When banks treat transaction enrichment as an afterthought, everything downstream breaks. Spending insights? Generic at best. Carbon footprint? Ballpark. Compliance? Painful. Disputes? Endless. And every product manager knows the domino effect: low data trust means disengaged users, low NPS, and higher churn.

The smartest banks and fintechs now treat transaction enhancement as non-negotiable infrastructure - a capability that cuts across UX, operations, compliance, and even brand trust.

Here are five real stories that show how banks enrich their transaction data to power features their competitors still struggle to deliver.

1. Raiffeisenbank Czech Republic — Merchant-Level CO2 reporting

Like many banks, Raiffeisenbank wanted to give customers insight into the carbon footprint of their spending - but the typical method just maps MCC codes to broad emissions factors. The trouble is that these categories are too blunt: a high-end organic shop and a discount supermarket can share the same MCC, so the estimate is basically an average. That disconnect makes the numbers feel generic and easy to ignore.

Solution

Raiffeisenbank used Tapix’s Eco Track™ on top of its merchant-level enhancement to get more granular. The question is what are the benefits of using a data enrichment API? It’s much simpler than you’d think, each payment isn’t just mapped to an industry code, but to a specific type of merchant, which is matched with more precise emissions factors that vary by country. That means a grocery transaction is no longer lumped into a single food retail average but reflects whether it was an organic store, a convenience store, or a large chain. The bank also adds local context and tips that help customers understand what drives their footprint.

"When it comes to sustainability, we knew that relying solely on MCC wasn't providing meaningful results. That's why we turned to Tapix - to ensure that the information our clients see is as accurate as possible."

Michal Putna, Sustainability Officer, Raiffeisenbank Czech Republic

Perspective

If you’re offering any kind of carbon reporting in digital banking, you can’t rely on MCC alone - it’s too generic to be credible. Merchant-level enhancement makes the estimate realistic enough that people might actually pay attention and change their habits.

Read the Raiffeisenbank case study

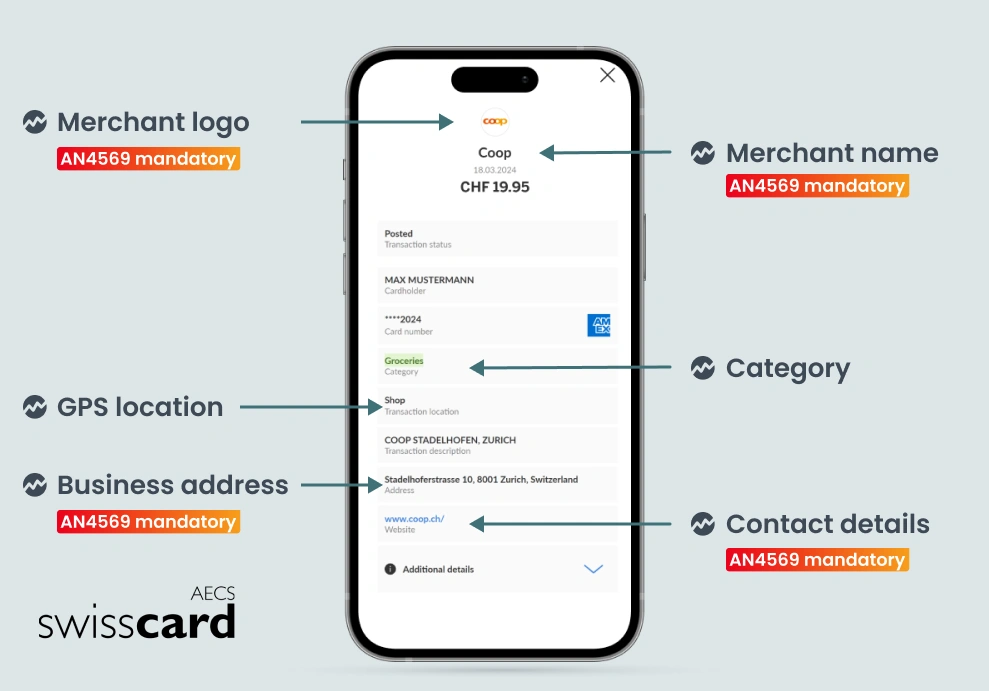

2. Swisscard — Mastercard AN4569 Compliance & UX Trust

When Mastercard introduced AN4569, Swisscard, like other issuers, suddenly needed to show verified merchant names, logos, addresses, and contact details for every card transaction. Without consistent data, the same merchant could appear in multiple forms, or with missing info - which frustrates customers and clogs up support when people don’t recognise charges.

Solution

They needed to enhance transaction data and asked what solutions are available. Instead of patching gaps one by one, Swisscard worked with Tapix to apply a tested banking transaction enrichment layer that standardises merchant information in line with AN4569. They also went beyond the baseline requirements by adding GPS data and clear category tags, so users see more than just the legal name. This extra context reduces confusion and makes statements clearer. The rollout took three months - a timeline that would have been unrealistic with an in-house fix.

„In a quick 3-month integration, Tapix's data met and surpassed AN4569 standards, enhancing the overall payment experience for our users. We value our cooperation with Tapix as it grants us instant access to accurate global merchant data.“

Alex Friedli, Chief Operating Officer at Swisscard

Perspective

Every compliance update that touches your transaction feed is an opportunity to clean up recurring friction. If the data is consistent and complete, you spend less time on manual corrections and user disputes - and your statements feel more reliable by default.

Read the Swisscard case study

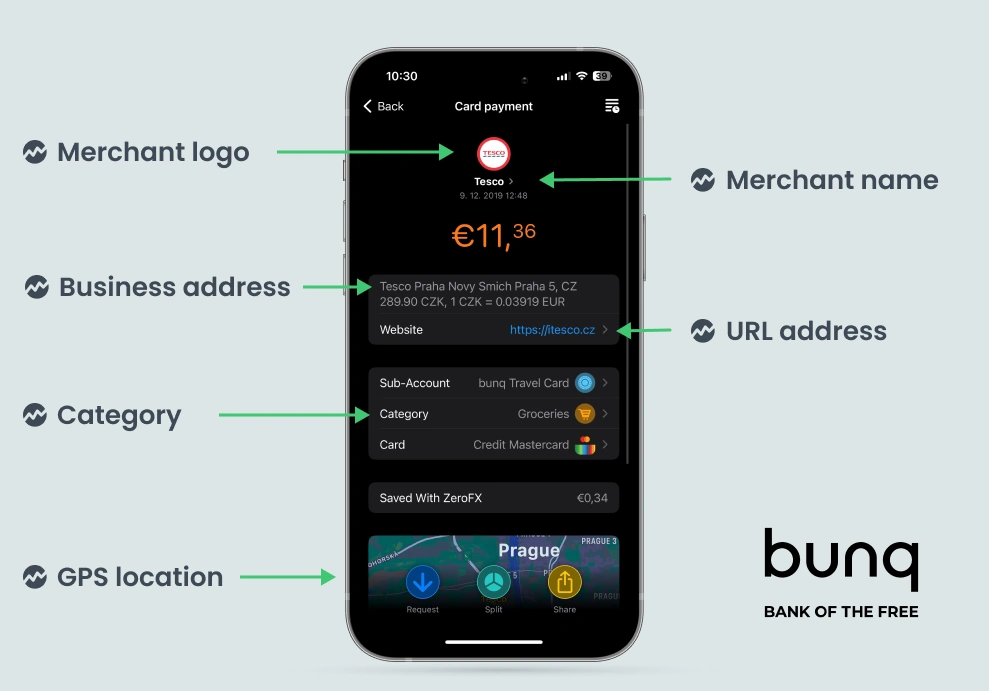

3. bunq — PFM, Budgeting, Subscriptions Through Banking Transaction Enrichment

When bunq started offering budgeting tools and spending insights, their merchant database was small - about 300 logos, manually maintained, with basic rule-based categorisation. That worked for a small footprint, but with expansion across the EU, it quickly became a bottleneck. The product team couldn’t launch new insights if they couldn’t trust that the underlying merchant data was correct and up to date. So, after a while they asked themselves a question: What solutions are there for payment data enrichment?

Solution

bunq handed over data enhancing to Tapix’s API, which recognises over 700,000 merchants and auto-categorises transactions with 99.99% accuracy, including transfers and recurring payments. That made it practical to introduce the Insights section, automatic budget breakdowns, and subscription overviews. They also added CO₂ reporting for customers who want to see the environmental impact of spending. Because enrichment updates run automatically, bunq can keep scaling without spinning up more manual data work.

“People are looking for a clear idea of what they spent and where. It’s so much easier for people to understand their spending habits when they can visually see what’s happening. While looking for a solution to this, we found Tapix. They’ve helped us give people a much better insight into their spending, and we’ve saved a tonne of time in the process. Using Tapix gave us a really high-quality product, in a very short period of time.” Tom Bilske, Product owner at bunq

Perspective

Data enhancement is what makes budget tools stick. PFM tools stand or fall on the quality of the data underneath. If you rely on a small, manually curated database, you’ll hit a wall fast. A robust enrichment layer gives you breathing room to focus on the actual product, not endless merchant corrections.

Read the bunq case study

4. Deblock — Merchant Coverage at Scale

Deblock combines a fiat account with a non-custodial crypto wallet and cards that work internationally. That creates a messy mix of local and cross-border merchants — many small or new — and an internal enhancement process that only handled about half of transactions. Users often couldn’t tell who a charge was from, especially when paying abroad.

Solution

Have you ever wondered how to improve the data quality of payment transactions? Deblock did too, and that’s why they integrated Tapix’s cloud enrichment API, which lifted merchant coverage from about 50% to 75% in a month. They also backfilled millions of older transactions so the improvement applied to past spending too. Even with large volumes, the enrichment runs in real time with minimal delay, so transaction feeds feel clear and consistent.

“In a product that connects traditional and decentralised finance, you don’t want your users lost in the transaction list. Tapix helped us deliver the kind of experience that feels native — clean, fast, and easy to trust.” Eugene Shulitskyi, Head of Fiat Products, Deblock

Perspective

When your customers spend across borders — and especially when you add crypto — ambiguous transaction data makes everything harder to trust. Merchant clarity isn’t a ‘nice UX touch’; it’s basic hygiene for hybrid financial products.

Read the Deblock case study

5. Partners Banka — Built-In Enrichment for Digital Bank Launch

Partners Banka didn’t have legacy systems but they knew poor transaction clarity could make their new mobile app feel unfinished on day one. That’s why they were Looking for best-in-class transaction data enrichment services.

Solution

They made transaction enrichment part of their core build. Tapix’s API was set up early so every transaction shows a clean merchant name, logo, GPS location, and category from the start. This foundation now supports Chytrá bilance, which blends categorisation with advisory features — so customers get a feed that’s understandable and useful without needing extra explanations.

“From the start, we saw enhanced transaction data as a core part of our UX strategy. If users can’t tell where they paid, it undermines the basics of what a banking app is supposed to deliver. Showing merchant names, logos, and adding context to a transaction might seem like small things—but for us, they were among the first things we decided to build. Working with Tapix helped us implement this quickly and at a high standard, which was essential during such a fast-moving launch phase.”

Lukáš Klíma, Product Owner, Partners Banka

Perspective

When you’re starting fresh, you don’t get a second chance at building user trust. Good data clarity is cheaper and simpler to get right up front than to retrofit after customers start asking, “What is this charge?”

Read about their 5 priorities before launch

The Patterns: 5 Things Every Digital Bank Can Learn From This

- Stop depending on MCCs. Merchant-level data is the new minimum standard.

- Treat enrichment as core infrastructure, not a side tool. It affects UX, ops, disputes, and future features.

- Leverage mandates to do better. Compliance deadlines justify upgrading legacy data.

- Use real-time and historical enrichment together. Users judge you on old data too.

- Data trust is UX. Clean transaction feeds build confidence, boost NPS, and reduce tickets.

For teams working on carbon footprint features, regulatory compliance, PFM, or hybrid wallets, the lesson is the same: clean, enriched transaction data is quiet infrastructure. It’s what lets everything downstream - from dispute reduction to budgeting tools - work without surprises.

Learn more about how Tapix helps banks build that foundation