The Mastercard AN4569 mandate refers to a set of regulatory standards and requirements to ensure a consistent and secure framework for digital payment transactions. These standards encompass various data points and compliance measures that financial institutions and businesses must adhere to when processing Mastercard payments. The mandate aims to enhance security, promote transparency, and streamline digital payment processes for both businesses and consumers.

While complying with the minimum requirements of the mandate is important for regulatory purposes, there are several compelling reasons for businesses to go beyond these mandatory data points. It's an opportunity to revolutionize the digital payment landscape. By doing that, businesses can unlock a suite of powerful features that redefine the user experience and enhance operational efficiency.

In this article, we explore five compelling use cases that showcase the transformative potential of Mastercard AN4569 when enriched with additional data points.

1. Clean & Visual Payments Overview

Mastercard AN4569 compliance serves as the foundation for a clean and visually intuitive payments overview. However, by incorporating additional data points such as GPS location, purchase category, and merchant URL, businesses can elevate the user interface to provide a seamless and aesthetically pleasing transaction experience. This not only meets the minimum requirements but surpasses them, offering users a comprehensive and visually appealing representation of their financial transactions.

2. Credit Risk Scoring and Fraud Detection

Going beyond the AN4569 mandate by including detailed data points allows for a more robust credit risk scoring and fraud detection system. Enhanced merchant information, coupled with GPS location and category specifics, enriches transaction data, providing a holistic view for risk assessment. This enriched data not only facilitates more accurate credit risk scoring but also enhances the ability to detect and prevent fraudulent activities, such as friendly fraud for example. A US market study revealed that nearly 25% of all transaction disputes could be avoided by delivering more details. The proactive approach to compliance ensures a secure and trustworthy payment environment, safeguarding both businesses and consumers.

3. Customer Behavior Analytics

The mandate sets the stage for basic analytics of payment data, but true insights emerge when businesses delve deeper. By incorporating Google Places ID, CO2/Eco-tags, and additional metadata, institutions can perform advanced customer behavior analytics. Understanding spending patterns, preferences, and ecological impact enables businesses to tailor services, enhance customer experiences, and stay ahead in a competitive market.

4. Overview of Recurring Payments

While the AN4569 mandate covers transaction details, diving into recurring payments requires additional insights. By enriching data with features like merchant URL and detailed category information, businesses can offer users a comprehensive overview of their recurring expenses. Picture a dashboard that not only lists recurring transactions but also provides insights into each subscription, be it an electrical bill, Netflix or mortgage.

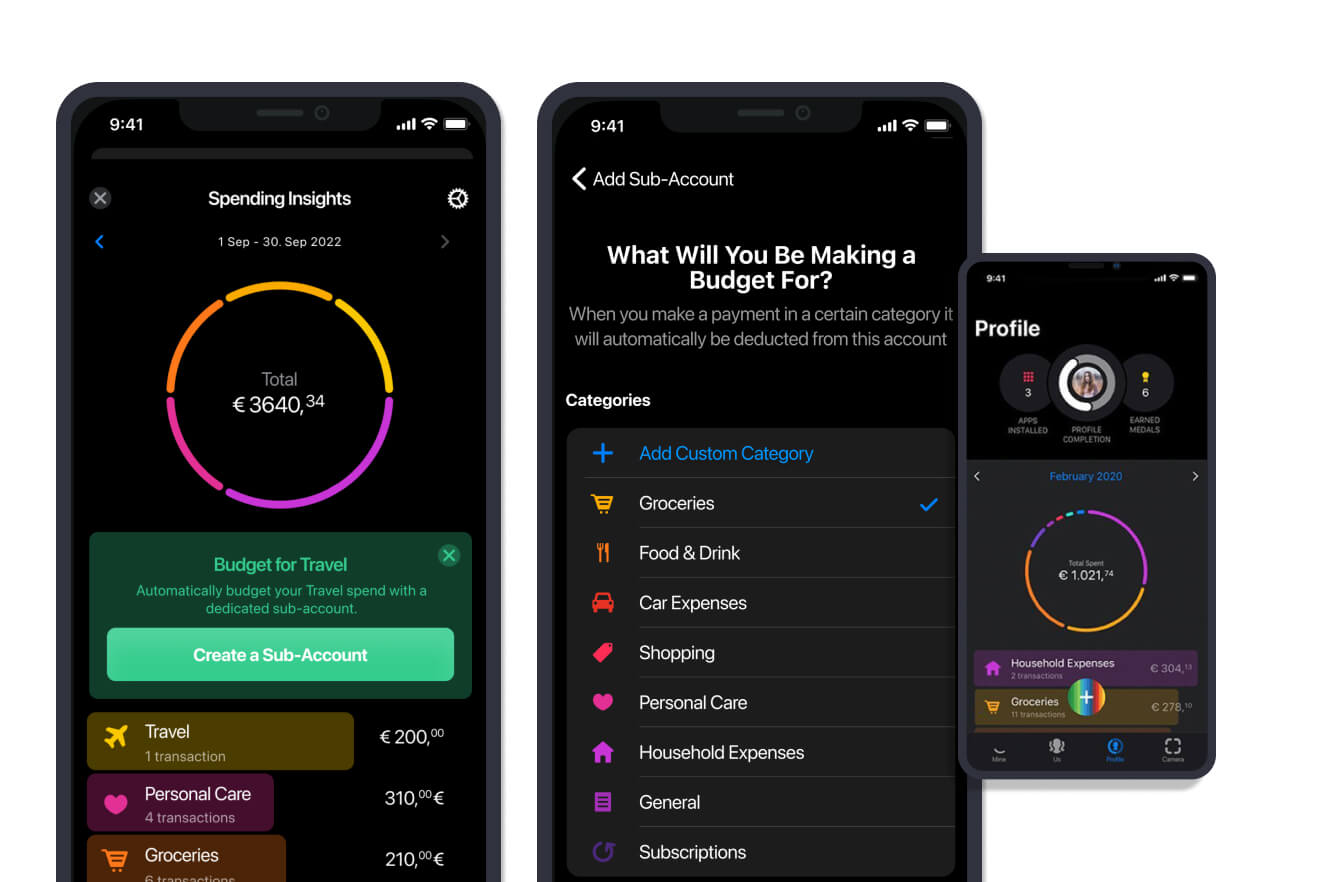

5. PFM & Data-Driven Spending Insights

Personal Finance Management (PFM) goes beyond basic compliance. To provide users with meaningful spending insights, institutions can leverage AN4569 compliance by including GPS location, purchase category, merchant URL, Google Places ID and CO2/Eco-tags. Users can receive personalized insights into their spending behavior, complete with actionable recommendations. This not only enhances financial literacy but also fosters responsible financial management, creating a more engaged and informed customer base. The enriched data allows users to make informed decisions about their finances, contributing to a healthier financial ecosystem.

Each use case for going beyond the Mastercard AN4569 mandate's minimum requirements opens up new possibilities for businesses. Whether it's enhancing the user experience, fortifying security measures, gaining deeper customer insights, or providing comprehensive overviews, the proactive approach to compliance transforms regulatory obligations into opportunities for innovation and customer-centric financial services. This not only fulfills the mandate but also puts control in the hands of users for effective financial planning.

Appendix A: Details of scheme compliance requirements

Sourced from AN4569 Revised Standards for Mastercard Rules (published 4 April 2023)

Enhanced Merchant Data. Effective 14 October 2023, an Issuer in Albania, Andorra, Austria, Belgium, Bosnia, Bulgaria, Channel Islands, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Gibraltar, Greece, Hungary, Iceland, Ireland, Isle of Man,

Italy, Kosovo, Latvia, Liechtenstein, Lithuania, Luxembourg, Macedonia, Malta, Moldova, Monaco, Montenegro, Netherlands, Norway, Poland, Portugal, Romania, San Marino, Serbia, Slovakia, Slovenia, Spain, Sweden, Switzerland, Ukraine, United Kingdom or Vatican City must provide to a Cardholder enhanced Merchant data, when available, to help the Cardholder recognize a Transaction when it is queried by the Cardholder. Such enhanced Merchant data includes, when available, without limitation, the Merchant’s public facing or ‘doing business as’ name, location, contact details and logo. The Issuer must provide the enhanced Merchant data via the Issuer’s banking application, mobile wallet, Internet banking interface, or other digital means that provides at least equivalent ease and accessibility for the Cardholder.