Every payment tells a story. But too often, that story is buried under messy codes, cryptic abbreviations, and raw transaction strings that customers can’t understand. For banks, fintechs, and payment providers, this lack of clarity creates frustration, higher support costs, and missed opportunities to deliver value.

Payment data categorisation solves this problem by transforming unstructured payment data into clean, structured, and enriched information. It’s the foundation for better customer experiences, stronger analytics, and innovative financial products. In this guide, we’ll break down what categorisation is, why it matters, how it works, and how financial institutions can evaluate and implement the right solution.

The Challenges of Raw Transaction Data

On its own, payment data is chaotic. Merchant names come in distorted variations. One customer might see “AMZ*12345,” another “AMAZON EU SARL.” Context is often missing altogether - no logos, no geolocation, no hint whether the purchase was online or in-store. And then there are the Merchant Category Codes (MCCs): outdated, blunt instruments that throw wildly different businesses into the same bucket.

The result is predictable. Customers fail to recognise transactions, open disputes unnecessarily, and lose trust. Banks and fintechs, meanwhile, struggle to analyse spending, personalise services, or detect risks effectively. What should be a goldmine of behavioural data becomes a swamp of inconsistencies.

What Payment Data Categorisation Does

Payment data categorisation acts as the translator between raw data and human-readable insight. It takes a tangled string of characters and turns it into something people can instantly understand.

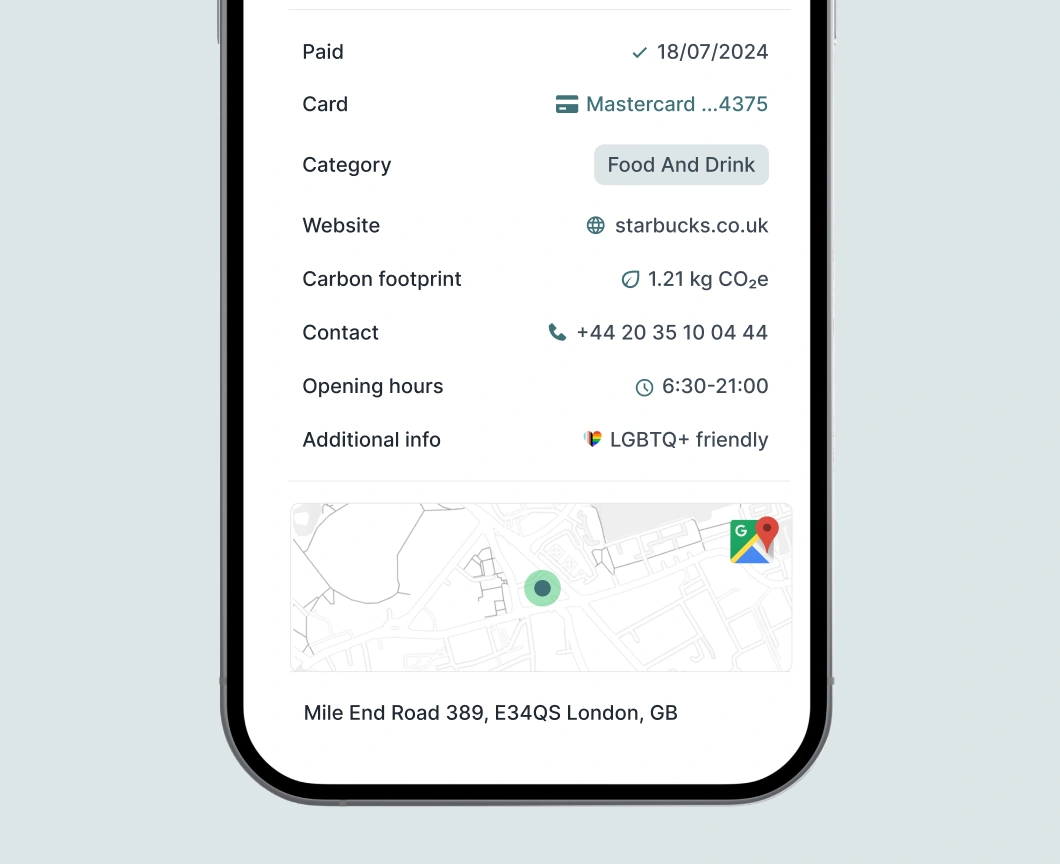

- Merchant recognition replaces “AMZ*12345” with “Amazon Marketplace.”

- Categorisation assigns transactions to useful groups like groceries, utilities, or travel.

- Enrichment adds logos, metadata, and geolocation for extra context.

- Intelligence identifies recurring payments or subscriptions and highlights whether purchases are digital or in-store.

What emerges is a user-friendly transaction history that reduces doubt, builds trust, and enables new layers of financial services.

Why Payment Data Categorisation Matters

This is not a technical side project. Categorisation directly impacts business outcomes. Customers armed with clear, accurate information are less likely to flood support lines or dispute charges. Budgeting apps and savings dashboards depend on categorised data to function. Fraud detection and credit scoring models sharpen when they can rely on structured insights instead of messy strings.

In short, clean data equals stronger engagement, fewer operational costs, and the ability to design financial products that genuinely reflect customer behaviour.

Key Components and Techniques

Not all categorisation platforms are created equal. Institutions must weigh accuracy, speed, and compliance. High recognition rates with minimal errors are a given, but equally important is latency: can the tool categorise in real time, or only in batches? Global coverage matters, as does the depth of enrichment. A clean merchant name is useful - but pairing it with a logo, metadata, and subscription detection creates far more value.

Integration is another consideration. Developer-friendly APIs and seamless onboarding can mean the difference between a smooth launch and a stalled project. And, of course, compliance with GDPR and local regulations is non-negotiable.

Want to know more?

Learn about data quality and how it affects your business!

Common Use Cases of Payment Data Categorisation

The true impact of categorisation emerges when you look at how it’s applied in real banking products and customer experiences:

Personal Finance Management (PFM): PFM apps live and die by their ability to make money management effortless. Categorisation powers the very features customers now take for granted - instant budgeting, automatic savings allocation, and subscription tracking. A user who sees their Spotify and Netflix payments grouped under “Entertainment” no longer has to dig through cryptic transaction logs. Beyond convenience, this clarity helps customers set goals and track progress automatically.

Transaction Histories: The bank statement used to be a list of numbers. Today, customers expect it to look like a digital diary of their spending - complete with merchant logos, clear names, and contextual details. Categorisation transforms dull, ambiguous entries into recognisable transactions. That transparency reduces the anxiety of unrecognised charges and gives people a reason to open the banking app more often.

Spending Insights & Alerts: Categorised data is the fuel behind proactive money management. When the system recognises that a customer spent 25% more on dining out compared to last month, it can generate a meaningful alert. Alerts aren’t just warnings about overspending; they become nudges that help customers adjust habits before they spiral into financial stress.

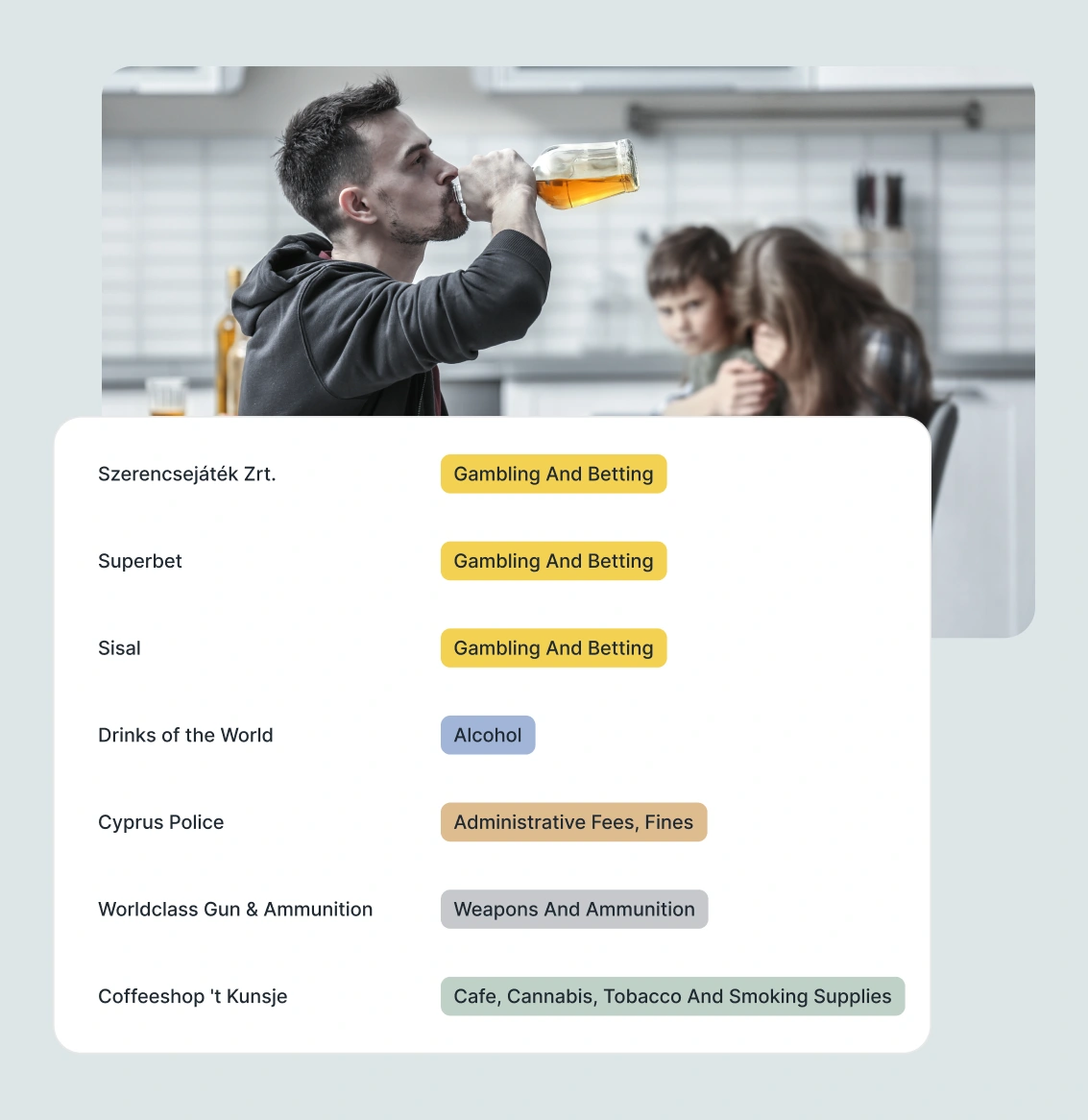

Credit Scoring: Traditional credit scoring models rely on static metrics - payment history, outstanding loans, and income data. Enriched payment categorisation adds another layer of behavioural insight. Knowing that a customer reliably pays utility bills on time, maintains consistent grocery spending, and avoids high-risk categories like online gambling offers a far more accurate picture of creditworthiness. This opens doors for “thin-file” customers, such as young people or new immigrants, who lack conventional credit histories but generate plenty of valuable transaction data.

Fraud Detection: Fraud often hides in plain sight, disguised as ordinary-looking payments. Categorised data helps separate the unusual from the expected. For example, a sudden charge in the “Luxury Retail” category from a user who typically spends only on groceries and transport is a red flag. Similarly, distinguishing between recurring subscription charges and one-off payments helps prevent false positives in fraud alerts. By aligning categorisation with anomaly detection systems, institutions can strike the balance between vigilance and customer convenience.

Steps to Implement Payment Data Categorisation

Rolling out a categorisation system is not a plug-and-play task. It requires deliberate planning, testing, and continuous refinement. The process typically unfolds in several key stages:

Pilot Program: Implementation begins with a controlled pilot. A subset of real transaction data is fed into the categorisation engine to test how well it performs in practice. It’s about seeing whether merchant recognition works across local brands, niche e-commerce platforms, and cross-border payments. Institutions should measure coverage, accuracy, and enrichment depth.

Feedback Mechanisms: No system is perfect from the start. Customers will inevitably encounter transactions that are miscategorised or incomplete. The rollout should therefore include feedback loops - ways for users or internal teams to flag errors and suggest corrections.

Integration: Categorisation only creates value if it reaches the customer-facing layer. That means connecting APIs directly into transaction feeds, mobile banking apps, and personal finance dashboards. Integration also extends to internal systems such as risk engines and data warehouses, ensuring categorised data fuels both customer experience and operational analytics.

Monitoring: Once live, categorisation systems need constant monitoring. Key metrics include accuracy (how often transactions are correctly labelled), coverage (how many merchants are recognised), latency (how fast categorisation happens), and processing stability under peak loads.

Iteration: The payments landscape changes daily. New merchants appear, subscription models evolve, and consumer behaviour shifts. A static categorisation system quickly becomes obsolete. Continuous refinement of taxonomies, merchant databases, and AI models is essential.

This approach ensures categorisation adapts as customer needs evolve.

Conclusion

Payment data categorisation is more than a back-office function. It’s a strategic capability. It transforms raw, unreadable data into a valuable resource for customers and institutions alike. By investing in accurate, real-time categorisation, financial institutions reduce disputes, unlock innovation, and build trust.