Raw card data has always been half measure. You can barely read the merchant, the MCC looks “fine-ish,” and context is missing. Enrichment APIs fix that. They turn noisy payment strings into readable stories - complete with merchant identity, category, channel, location, and recurring or refund signals. The faster this happens, the better the experience for all bank transaction types. Every second of latency is a lost moment to reassure, reward, or retain a customer.

But not every transaction looks the same. An online payment, a coffee on a street corner, and a monthly Netflix renewal all need different datapoints to make sense. Let’s look at how enrichment connects these worlds - and why the details matter.

What You Send vs What You Show

Banks and fintechs send input identifiers: network or acquirer merchant IDs, free-text strings, terminal hints - essentially, chaos. Tapix turns that into a canonical merchant identity: a clean brand name, proper logo, consistent category, and brand lineage that hold across borders. In other words, you send the clues; enrichment gives you the full picture.

A single low-latency API delivers multiple datapoints in one response - from merchant identity and category to geo hints and recurring flags. Surrounding it are companion APIs like Eco Track for sustainability overlays, ATM Nearby for cash utility, and Invalidations for keeping everything honest when data drifts. When you link Tapix with the Dateio Platform, that enriched data powers something bigger: real, measurable engagement through bank-channel card-linked offers.

Let's explore different bank transaction types and what data points they actually require:

Online Transactions

Online transactions are the fastest, but also the messiest. A cryptic line like “AMZSTOR-4829”* doesn’t tell users much. For banks, that means higher support volume; for fintechs, it means confusion in budgets and insights.

What matters here:

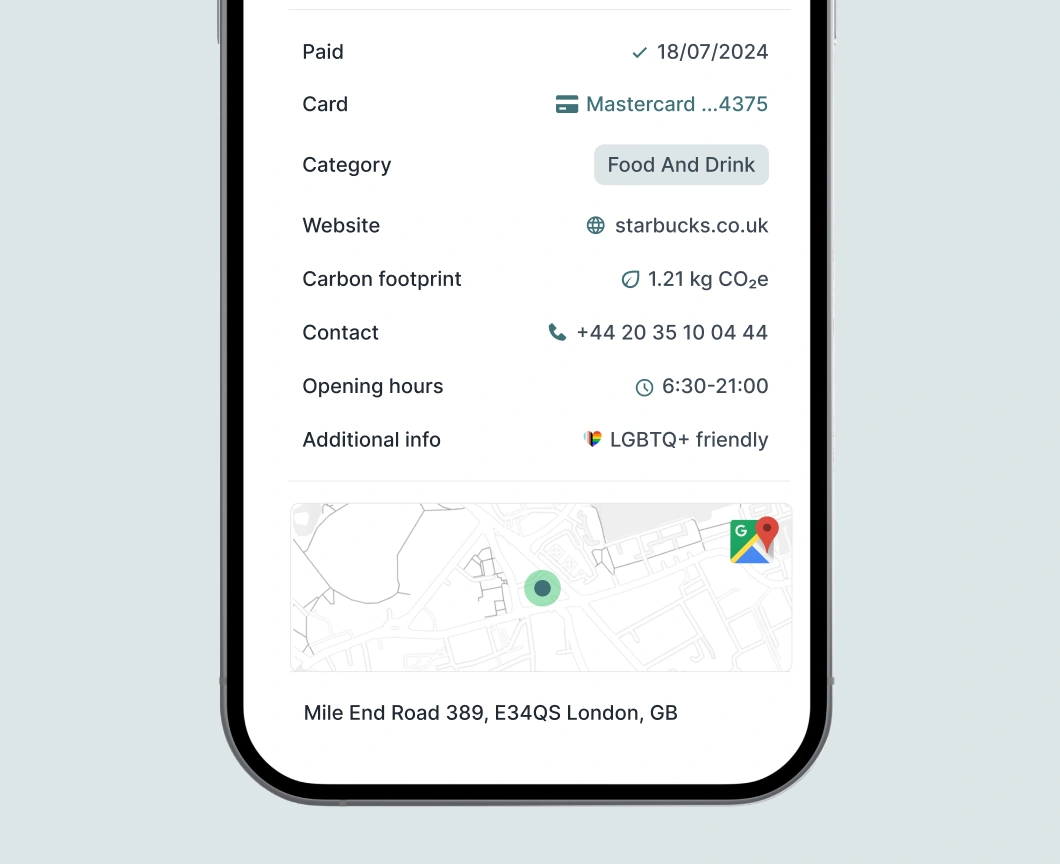

- Merchant Identity & Logo: Users want to recognise where their money went. A clear name and logo build trust and reduce chargebacks.

- Category & Channel Tags: Distinguish e-commerce from in-store purchases to make PFM summaries meaningful.

- Payment Gateway Recognition: In online payments, the actual charge may not come directly from the merchant - it might go through a gateway like Adyen, Stripe, or PayU. Recognise that layer and trace the payment back to the real brand.

- Website & Contact Links: Add direct merchant links so customers can reach support or manage orders without leaving the banking app.

- Geo Accuracy: Even online, geo helps - it differentiates local online merchants from cross-border ones, which matters for fraud detection and personalisation.

- QR Payments: QR-based payments, where users can withdraw cash from ATMs or pay in small stores without a terminal, break the old categories. A convenience store might not appear under “retail” at all, and enrichment has to work harder to classify it correctly.

- Invalidations: Descriptors and routing data change constantly; the Invalidations API ensures that when a merchant’s setup shifts, your mapping doesn’t break.

Clean, recognisable online transactions do more than calm users - they anchor digital trust. Once clarity is in place, banks can use enriched data for smarter fraud rules and faster post-purchase experiences.

Physical Transactions

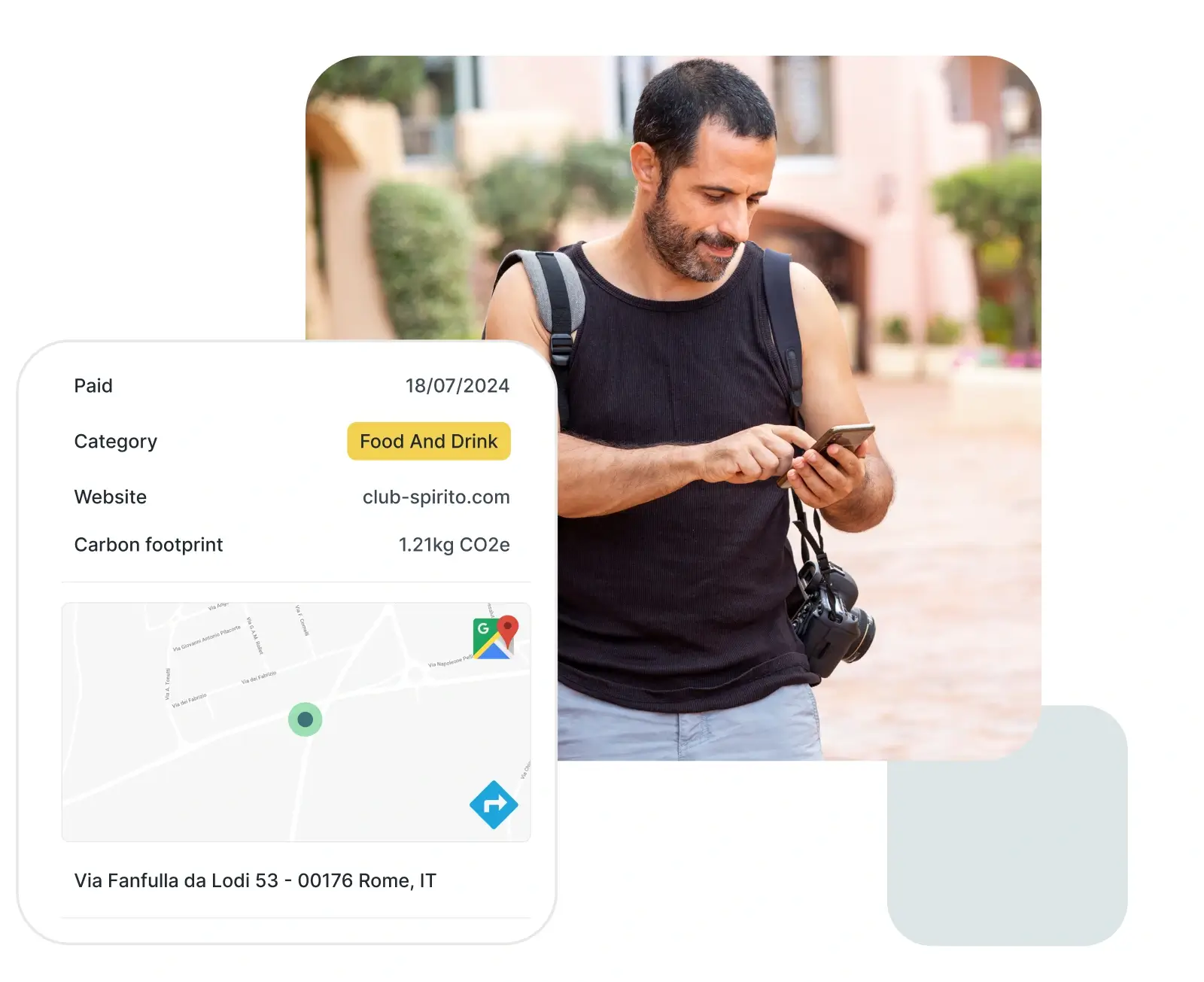

In-store payments bring a physical dimension that online data can’t: the “where.” Knowing the store location, not just the merchant brand, gives customers tangible confidence - Yes, that was the café by the office, not some random charge.

What matters here:

- GPS & Store-Level Matching: Enrichment uses terminal configurations, merchant routes, and history to infer the most likely outlet. With GPS, it can identify the exact branch or even nearby ATMs.

- Merchant Category: Refined MCCs group similar merchants together while keeping behavioural precision - “lunch spots” instead of “food.”

- Local Campaigns via CLM: For merchants, that data drives local promotions. With Dateio Platform, offers can target the store’s actual visitors, not just generic audiences.

- ATM Nearby: Enrichment extends beyond purchases; it supports utility. When a customer searches for cash access after paying at a store, context turns into convenience.

Every clear in-store transaction means one less dispute, one less support ticket, and one more touchpoint where the brand feels reliable. For banks, it’s also the groundwork for credible footfall analytics and regional engagement strategies.

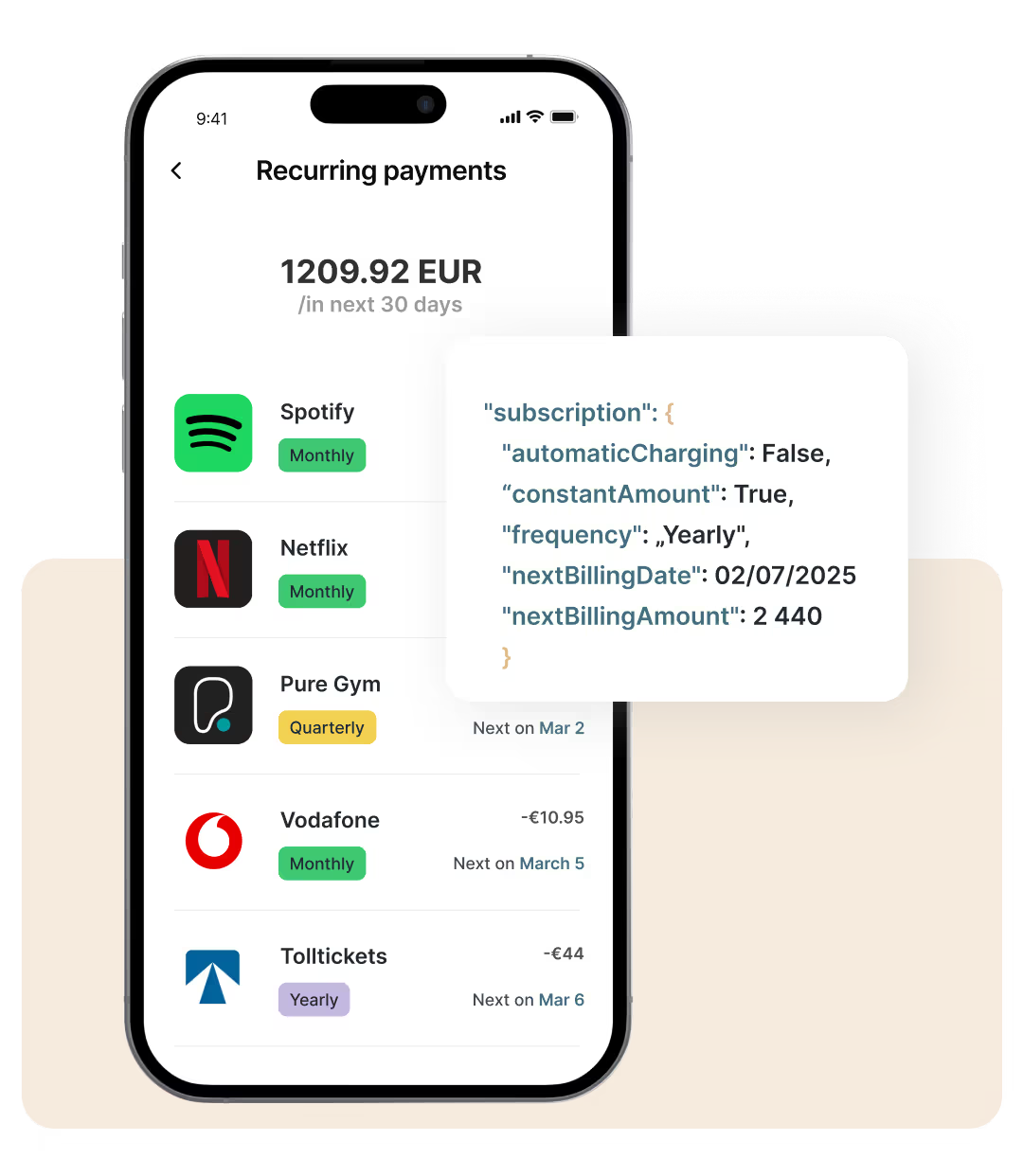

Subscription Transactions

Subscriptions are calm on the surface - recurring, stable, predictable - until there’s a change. A missed payment, a sudden price jump, a free trial that turned paid without warning. Here, enrichment is preventive.

What matters here:

- Recurring & Cadence Detection: Identify repeating patterns, frequencies, and billing intervals to classify subscriptions accurately.

- Price-Change Signals: Detect when merchants alter pricing or bundle structure; banks can alert users early and avoid “I didn’t authorise this” disputes.

- Cancellation Intent: Analyse skipped charges or failed renewals to surface retention opportunities for merchants.

- Brand Identity & Category: Differentiate between Spotify and Spotify Premium Family - small distinctions that shape real support outcomes.

- Integration with Subscription Management: Combine Tapix intelligence with in-app cancellation flows (e.g., Minna or Subaio) for a full user journey.

Banks use this layer for empathetic alerts (“Your streaming plan increased by €2”), fintechs for smarter financial coaching, and merchants for churn recovery. Everyone wins - fewer disputes, happier users, more retained revenue.

Loyalty & Card-Linked Offers

Once transactions are clean and contextual, enrichment turns from passive insight into active engagement. Card-linked marketing (CLM) in banking apps uses real spend to reach customers with relevant offers. Tapix handles the identification and targeting; the Dateio Platform distributes and settles the rewards.

A restaurant doesn’t have to blast everyone - it can target people who actually dined nearby in the last 30 days. Retailers can measure the real lift of campaigns by comparing redemption against enriched merchant IDs. Banks, in turn, benefit from deeper engagement and daily app visits that feel rewarding. instead of intrusive.

Metrics that prove it works? Incremental sales, redemption rate, repeat-visit rate, and post-reward ROAS. When those go up, the loop holds.

From Requirements to Reliability

Enrichment is as much about control as it is about insights. Payment data constantly changes. Descriptors drift, merchants rebrand, acquirers reroute. The Invalidations API acts as a correction mechanism, letting you invalidate wrong mappings and rematch in seconds instead of waiting for things to “sort themselves out.”

Then comes compliance. Different markets impose different boundaries: Saudi Arabia enforces on-prem processing; Europe enforces data residency under PSD2/PSD3. Tapix supports flexible deployment without trading latency for legality.

Conclusion

Every transaction - whether online, in-store, or subscription - tells a different story. Enrichment makes sure that story is legible, timely, and useful. It turns payment noise into context, context into engagement, and engagement into measurable value. One API, three transaction types, endless ways to make payments mean something again.

For more details on how enrichment solutions can benefit your bank, explore the Tapix offerings.