The way we handle financial transactions has evolved significantly. Contactless payments, mobile wallets, and digital-only banking apps have redefined what it means to manage money. Despite all the technological progress, many banks still struggle in one important area: categorising transactions effectively. This is essential for almost every digital banking service.

Most institutions continue to rely on outdated Merchant Category Codes (MCCs) as the primary method of classifying purchases. These codes provide a basic structure, but they can be too broad or wrong. This often leads to many transactions being mislabelled or placed into vague categories like “Retail” or “Other.”

When the data is not clean or specific, the whole customer experience suffers. This affects everything from budgeting tools to targeted offers.

Take a moment to compare a non-enriched vs. enriched transaction feed, and the difference is immediately obvious. One is just a list of charges; the other tells a story.

Enhanced data providers like Tapix offer a solution to this problem by providing more detailed and accurate bank transaction categorisation. In this article, we will look at common transaction challenges and discuss the benefits of better categorisation, which can help both banks and their clients.

What Is Enhanced Categorisation and Why It Matters

Merchant Category Codes (MCCs) were initially introduced to standardise the way transactions were classified across industries. While they provide a basic structure, they fail when applied to modern consumer behavior. Banking needs to adapt to the unique needs of every client and MCCs are not the way.

Today’s banking customers might book a flight, stream a movie, order lunch, and pay a utility bill — all in one afternoon. And with more merchants offering multiple services under one brand, a single MCC often can’t capture what’s actually happening. Let’s say you order groceries and household items from the same platform — is that “Grocery,” “Retail,” or “Other”?

The truth is, the label isn’t helpful unless it’s specific. Context that can bring banks even more valuable data, and customers even more unique services. This is where accurate, deeper categorisation comes in.

Enhanced categorisation solves this by introducing more structure and logic to transaction data. Instead of using one broad category, transactions are split into several categories based on levels. This helps banks understand not just what was spent, but also why and how.

Providers like Tapix offer a four-tiered categorisation model that adds much-needed accuracy:

- Level 1: Merchant Category — Broad sector (e.g., Food & Dining, Utilities, Transportation)

- Level 2: Tag Level 1 — Specific vertical (e.g., Restaurants, Streaming Services, Ride-Sharing)

- Level 3: Tag Level 2 — Refined classification (e.g., Fast Food, Fine Dining, Public Transit)

- Level 4: Tag Level 3 — Merchant-level or context-specific detail (e.g., Starbucks – Takeaway – Prague)

This method helps financial institutions go beyond just raw transaction data. They can start to actually categorise bank transactions. This supports real-time insights, relevant products, and personalised engagement. It’s about making banking feel more personal after all.

Practical Use Cases for Banks and Fintechs

There are plenty of applications of detailed transaction categorisation, focusing on delivering tailored and personalised services to clients:

Real-time notifications

Tapix enables banks and fintechs like Twisto to use data in many ways. For example, real-time notifications to customers, showing the transaction category in real-time - during the payment process. Transactions are categorised in just 6 milliseconds and users get detailed notifications right when they make a purchase.

So when a customer pays for a taxi ride or orders lunch, they get a message that shows exactly what they bought, not just a random merchant ID. This gives them clear insight into their financial activities.

Payment category overview

Advanced categorisation features in Personal Financial Management (PFM) platforms help users see their spending patterns. It allows them to plan their budgets better, so they can easily track and analyse their spending.

This includes essential costs like housing and utilities. It also covers discretionary purchases like dining and entertainment. This allows for additional features like a spending cap for a specific category or transaction splitting for more flexibility.

And the benefit extends beyond individuals. For small businesses or freelancers, these tools can help keep personal and business spending apart. This can be hard when using one account for both.

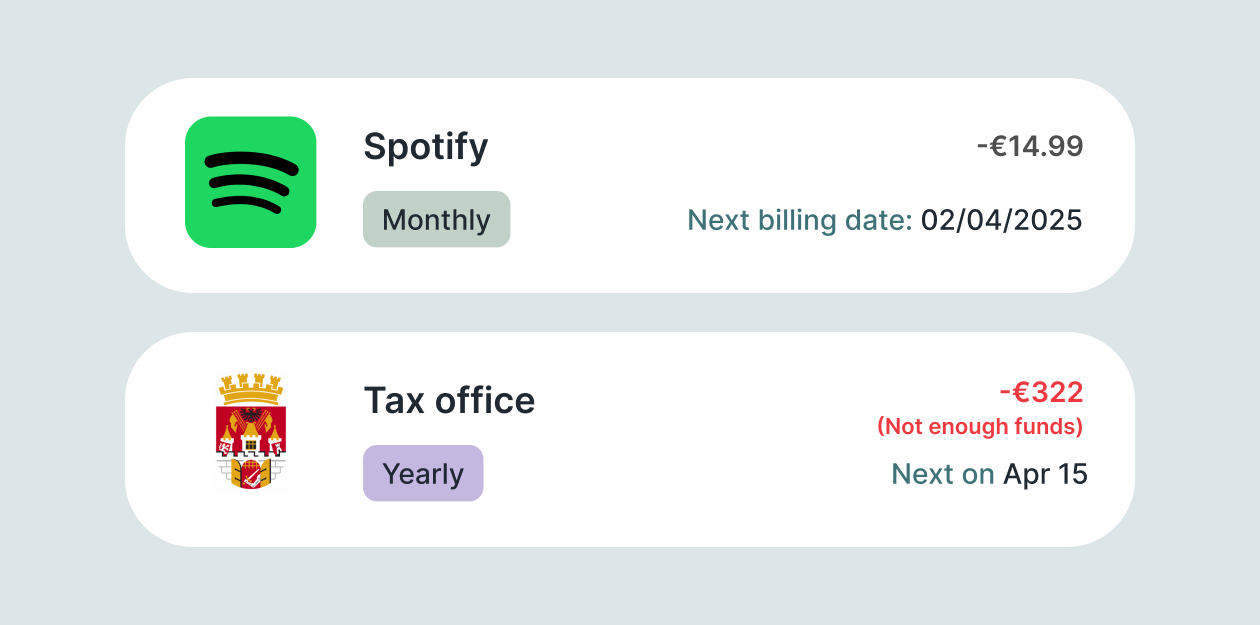

Recurring payments overview

Distinguishing between different types of recurring payments is essential for effective financial management. By correctly tagging transactions with subscription labels, banks can give customers a clear view of their financial obligations. This includes details like electricity bills, entertainment, and services.

By categorising these correctly, users can make smarter decisions, like cancelling unused services or prioritising essential ones. Banks can use this information to create subscription management tools and bundled deals. Additionally, they can alert customers before a price increase happens.

Strategic Value for Financial Institutions

Detailed categorisation has strategic benefits across multiple departments beyond just simplifying UX:

- Marketing & Product Teams can launch more relevant campaigns based on customer behavior. Imagine offering travel insurance right after someone books a flight. You could also suggest a business credit card to users with rising expenses.

- Customer Engagement teams can use enriched data to support personalised coaching or financial wellbeing tools.

- Risk and Compliance units gain from clearer classifications. These help to identify suspicious activity, improve credit models, and lower false positives in fraud detection.

- Support and Ops can more easily resolve customer inquiries when transaction data includes clear merchant tags and context.

Banks that correctly categorise transaction data can better meet customer needs. They can also create products based on real usage patterns and improve their internal operations. From onboarding to retention, every interaction is more informed, more personal, and more aligned with real-life behaviors.

By embracing enhanced categorisation tools like Tapix, banks can unlock deeper insights, offer more personalised experiences, and ultimately, strengthen their relationships with customers. Because in the end, it’s not about the data itself. It’s about what you do with it.

For more details on how enrichment solutions can benefit your bank, explore the Tapix offerings.