It is worth saying that the digital maturity of the banks in the region is rising. We see more banks offering remote account openings for business customers, digital lending or factoring processes, and the implementation of VAS in digital banking channels. And SME digital banking customers started to expect more and more from the banks. Below are the top five things that can be defined as the most important benchmarks in digital banking at the moment.

1. User Experience Within Digital Banking Channels

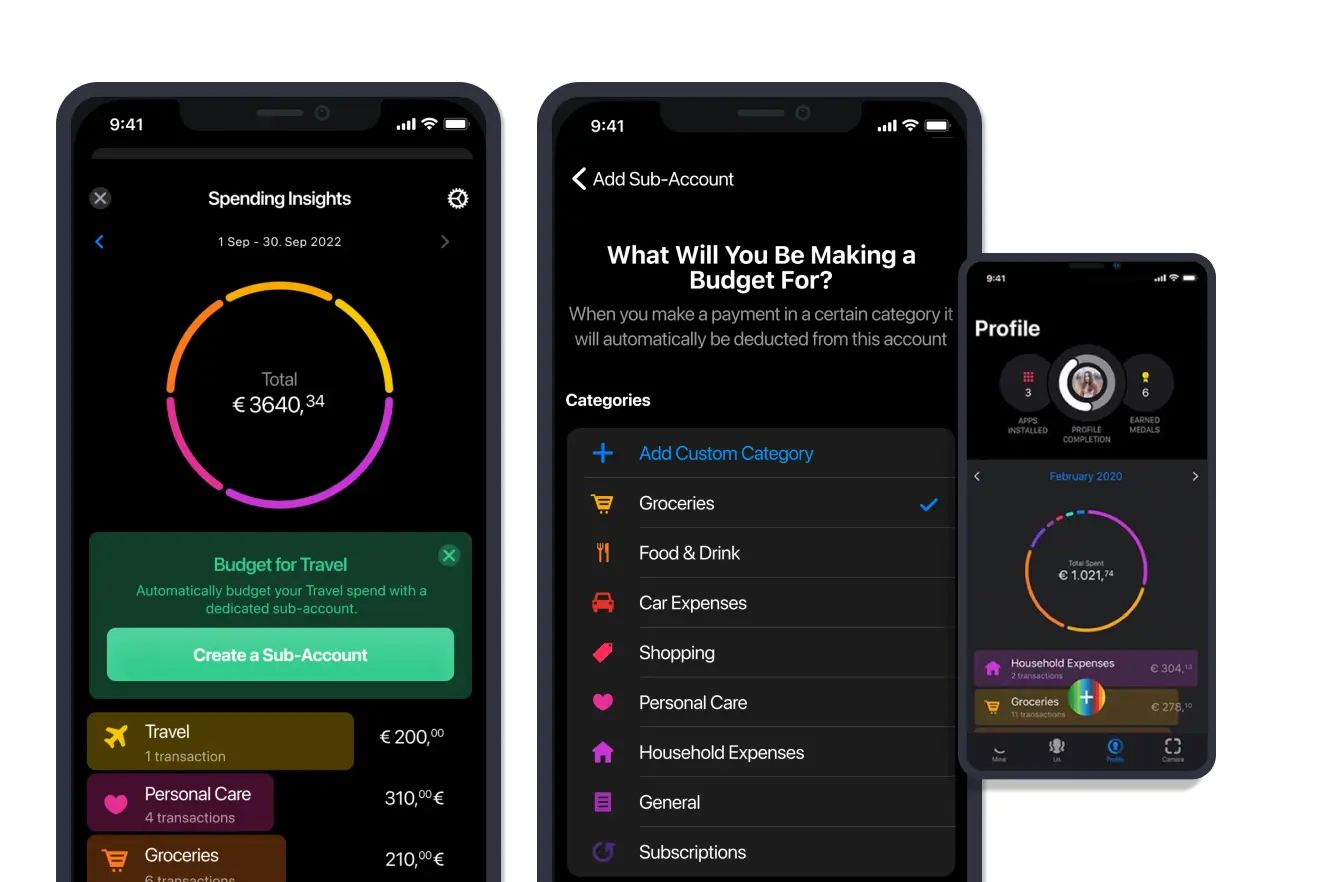

The user experience (UX) has become one of the most critical differentiators in SME banking. While over 70% of banks in the CEE region have already implemented core banking features - like LCY/FCY transfers, business account access, and currency exchange - the competition has shifted from functionality to usability. A smooth, intuitive, and responsive interface now plays a bigger role in user satisfaction and retention.

According to our research, the post-functionality era in digital banking means that usability, speed, and clarity outweigh even the number of features provided. This is backed by recent findings from Deloitte, which revealed that 76% of SME customers consider UX as a top-3 factor when choosing their primary banking provider.

Some banks are leveraging enriched transaction data to enhance UX further. For instance, platforms like Tapix use merchant name cleaning, logo enrichment, and category tagging to transform cryptic transaction logs into clear, easy-to-understand records - improving UX at the most-used point in digital banking: the transaction history.

Banks like mBank and Raiffeisenbank have also invested heavily in UX design, winning awards in 2024 for best SME digital platforms by integrating predictive search, streamlined dashboards, and guided onboarding tutorials. Banks that fail to improve UX risk seeing higher churn rates, especially as fintechs and neobanks continue to offer frictionless, design-first alternatives.

2. Instant Payments

Real-time payments - where funds are transferred and settled in under 10 seconds - are becoming more and more useful in the modern age. SMEs rely on fast liquidity access to manage suppliers, payroll, and cash flow, making instant payments a key operational need rather than a luxury.

In 2024, Hungary and Romania made significant strides by rolling out instant payment rails for business clients, largely driven by regulatory frameworks. Other countries in the region, like Slovakia and Bulgaria, are currently piloting similar systems as part of their alignment with the European Commission's Instant Credit Transfer initiative.

From a global perspective, the push for ISO 20022 standards is also streamlining cross-border instant payments. Companies like Tapix help SMEs and their banks track, clean, and categorise these transactions in real-time, providing transparency and reducing reconciliation errors.

Moreover, real-time payments unlock new use cases like real-time lending, instant credit checks, and pay-as-you-go services - expanding the embedded finance opportunities discussed later. The sooner banks implement instant payments, the sooner they can enable these higher-value offerings.

3. Mobile Banking

While online banking remains more functional today, mobile banking is rapidly catching up - and it’s where future battles for SME engagement will be won.

Mobile devices have become central to how SMEs manage their businesses, from payments and invoicing to authentication and approvals. Yet, most SME banking apps still lack parity with their desktop counterparts. In CEE, mobile banking apps for business customers typically offer only 50–60% of the functionality of online banking platforms.

That’s changing fast. Banks like Bank Pekao, OTP Bank or Partners Banka are leading the way with mobile-first strategies, building apps that are not only responsive but also enriched with value-added services like budgeting tools, payment tracking, e-invoicing, and in-app credit offers.

Mobile apps must also evolve to meet new cybersecurity expectations. Fingerprint/face ID login, secure app isolation, and AI-powered fraud detection are no longer optional. According to an IBM report, 60% of SMEs would switch providers if mobile security fails, underscoring the importance of trust on mobile platforms.

Platforms like Tapix contribute by embedding enriched transaction intelligence directly into mobile apps, giving users clean, merchant-branded transactions and real-time categorisation that fits small business workflows.

4. Embedded Finance and Contextual Finance

Embedded finance is revolutionising how banks interact with SME customers by offering financial products at the point of need - within e-commerce platforms, accounting software, or even logistics apps.

Contextual finance builds on this by using real-time data, enriched transactions, and behavioral patterns to present ultra-personalised offers. For example, if an SME regularly pays logistics partners and sees a seasonal cash flow dip, the bank can automatically offer a short-term working capital loan - without the customer ever needing to apply.

Tapix enables this kind of contextual finance by transforming raw transaction data into insights about spending behavior, merchant types, recurring expenses, and subscription patterns. This information can be used by banks to create tailored financial services embedded in a business’s daily activities. (Source)

According to Accenture, over $7 trillion in global embedded finance revenue is projected by 2030, with SME lending and payments among the fastest-growing segments. Leading banks in CEE are starting to integrate e-invoicing, insurance, and accounting tools within their platforms, giving SMEs a one-stop ecosystem for financial operations.

5. Integrations and Interoperability

The age of open banking is maturing into the era of open ecosystems. What began as a compliance requirement under PSD2 has evolved into a new business model for banks - Banking-as-a-Platform. APIs have become the gateway to both external innovation and internal modernisation. Instead of building every solution in-house, banks can now connect seamlessly with fintech partners, ERP tools, and e-commerce platforms.

Enrichment APIs from providers like Tapix connects directly with banks, allowing them to clean and label transactions in real time, delivering a better customer experience and improving data quality across services.

SMEs are also demanding interoperability. They don’t want to use five separate apps for accounting, invoicing, banking, and payments. Banks that build or integrate modular platforms - offering plug-and-play features - will gain a serious advantage.

Open ecosystems also support multi-bank aggregations, enabling SMEs to see their full financial picture from one dashboard, regardless of provider. This trend is especially strong in countries like Estonia, Lithuania, and the Netherlands, where financial innovation hubs drive API-first banking.