Industry insights

How AISPs Are Rewiring Financial Connectivity

When PSD2 came into effect in 2018, Account Information Service Providers got a formal identity. Banks had to open their APIs to licensed third parties, and consumers gained the legal right to let those third parties access their payment account data. Seven years later, hundreds of AISPs are registered across Europe, and the model has spread to the UK, Brazil, Australia, and parts of the Middle East.

.webp)

Industry insights

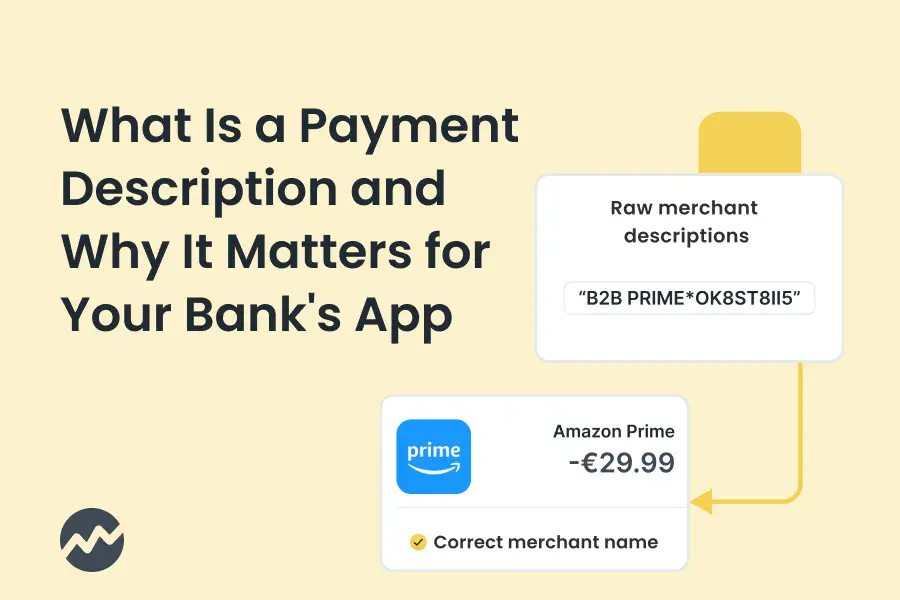

What Is a Payment Description and Why It Matters for Your Bank's App

Open any banking app, scroll a recent transaction feed, and the friction usually starts in the same place: a row of cryptic capital letters where a merchant name should be. That row is the payment description - the short text string that comes through with the transaction and lands in the app next to the amount. It is the single field that most determines whether a customer recognises what they bought, who they paid, and whether the charge is legitimate. Banks rarely control it, and in its raw form, it is rarely good enough to display.

.webp)

Industry insights

Transaction Data Enrichment Tools: What to Compare, and How to Choose the Right One

When you’re looking for transaction data enrichment tools and their features, six vendors usually come up: Tapix, Tink, Ethoca, Salt Edge, Fiserv, and Plaid. Most comparison posts treat them as interchangeable API swaps. They are not. They sit at different layers of the stack, they solve different problems, and picking the wrong one means paying for capabilities you do not need while missing the ones you do. This article walks through what each tool actually does, what it does not, and how to match them to the problem you are trying to solve.

Industry insights

What Card Network Transaction Data Do Banks Receive?

When a customer taps their card, the bank's issuer system receives a tightly structured but surprisingly thin bundle of card network transaction data. The fields are standardised, the values are constrained, and most of what an end user expects to see in their app - clean merchant names, logos, recognisable categories, exact shop locations - is simply not in the message. Everything from statement clarity to credit decisioning is built downstream of this raw payload, which makes the gap between what arrives and what a customer needs the single most consequential data problem in retail banking.

Industry insights

What Is CCD2? The Context, the Timeline, and What It Actually Means for Lenders and BNPL

The EU's revised Consumer Credit Directive (CCD2 for short) is about to change the rules for consumer lending and BNPL across Europe. By November 2026, lenders will need to prove that borrowers can actually afford what they're signing up for. That puts transaction data at the centre of every credit decision.

Industry insights

Trends, Initiatives and the Future of Green Banking Products

The topic of global warming, long-term sustainability and overall respect for planet Earth has been discussed for decades, across human activities and industries. Today, there is little doubt that climate change poses a real and significant political and economic risk to humanity.

Industry insights

Top 5 SME Banking Trends Shaping Digital Services in 2026

Business banking product teams have spent the last few years arguing about SME banking trends and UX while the regulatory and competitive ground shifted. Mastercard AN4569 is live. Visa’s mandate hits in 2027. CCD2 is moving the BNPL in a new direction. And challengers that were niche five years ago are now credible.

Industry insights

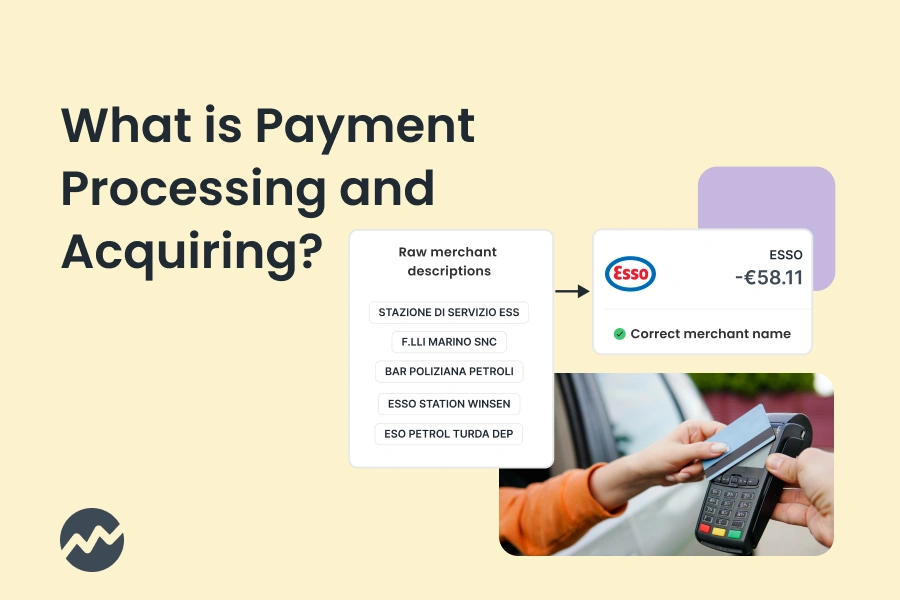

What Is Payment Processing and Acquiring? How Payments Work

Every card payment processing triggers a chain of events - money moves between banks, transaction records are created, and what customers see in their banking app is shaped by decisions made long before they tapped their card.

Industry insights

Transaction Data Explained: POS ID, Merchant ID & MCC

Every time a card is tapped, swiped, or entered online, a stream of raw transaction data is generated behind the scenes. Banks, payment processors, and fintechs all receive this data - yet very few of them can make it immediately useful.

Industry insights

Card-Present vs Card-Not-Present Transactions: What Banks Need to Know

For most payment teams, the card-present vs card-not-present transactions distinction gets filed under processing operations. It determines routing, compliance checklists, and interchange rate categories. But this framing is becoming a liability.

Industry insights

How Visa and Mastercard Impact Banking UX

Transaction UX used to be a product decision. Some banks invested in recognisable merchant names and clean feeds. Others shipped raw descriptor strings and MCC codes. Today, Visa and Mastercard are increasingly turning transaction clarity into issuer requirements, and the minimum bar is rising for everyone.

.webp)

Industry insights

How to Tailor SME Transaction Categorisation to Each Business Client

SME clients have higher expectations than retail clients, and for good reason. Banking is not a background activity for them - it is part of their daily operations, reporting cycles, and financial planning. Transaction categorisation is not a visual convenience. It directly influences cost control, tax handling, internal reporting, and how accurately a business understands its own financial position.

Industry insights

Future Trends in Mobile Banking: Trends, Features and What's Missing in 2026

Mobile banking has crossed the threshold from a convenient channel into the primary interface through which most people manage their financial lives. According to SQ Magazine, there are over 2.17 billion mobile banking users worldwide as of 2025, with Europe reaching 76% penetration and Nordic countries exceeding 87%.

Industry insights

How are Digital Banking APIs Transforming Finance in 2026

As banking gets more digital, the need for simplification and automation is becoming more apparent. A significant part of that leads to the adoption of APIs in banking. While APIs (Application Programming Interfaces) have been here for a long time, the current surge in digital banking is driven by the demand for real-time payment solutions, advances in open banking regulations, and the necessity for enhanced customer engagement.

Industry insights

Digital Banking KPIs: 7 Metrics That Predict App Growth

Key Performance Indicators (KPIs) serve as crucial tools, allowing banks to measure how effective their digital banking apps are in engaging customers. In this guide, we'll explore seven essential customer success KPIs, complete with straightforward formulas, designed to help banks improve customer engagement, foster loyalty, and reduce churn rates.

Industry insights

Top digital banking and fintech influencers to learn from

The fintech industry can be a crowded place. As it continues to grow and evolve, staying updated on the latest trends and innovations becomes more important than ever. LinkedIn is a goldmine for discovering influential thought leaders who provide valuable insights, news, and ideas that shape the sector.

Industry insights

What Is the Top 10 Digital Banking Trends to Look Out For in 2026?

Digital banking in 2026 will be defined by tighter regulation, higher UX expectations, cleaner data structures, and the slow disappearance of card-centric logic. Banks that treat data quality and transaction clarity as their core product layer move faster than institutions that still operate through legacy feeds and fragmented interfaces.

Industry insights

Top 135+ Fintech Conferences of 2026: Must-Attend Events for Industry Insights

Fintech and digital banking event lists exist, but they are often fragmented, incomplete, or hard to compare. Relevant conferences are spread across multiple sources with little structure. This curated overview brings them together in one place for 2026.

Industry insights

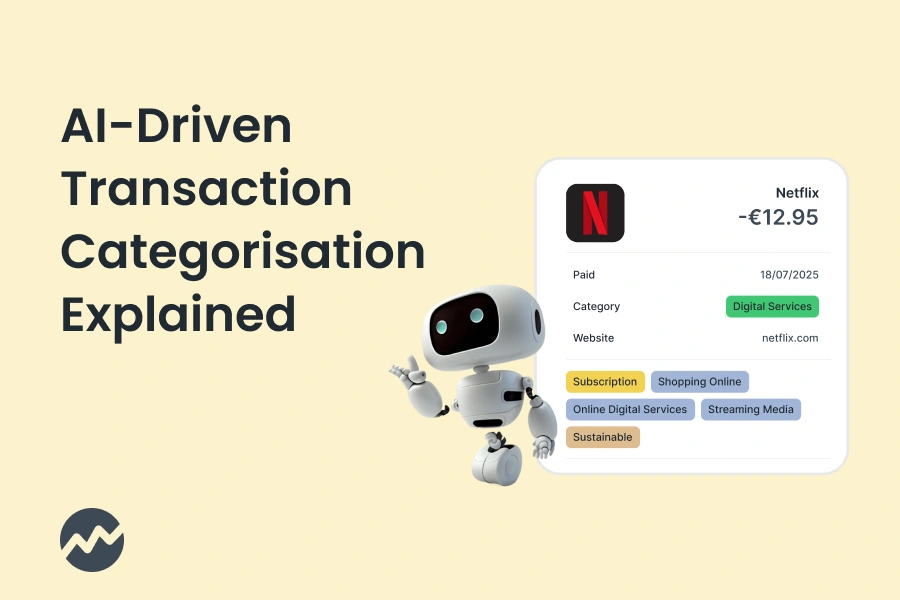

Transaction Enhancement Services: AI-Driven Categorisation Explained

Transaction enhancement services increasingly rely on AI and machine learning to automatically categorise transactions, enrich merchant data, and normalise transaction descriptions. These services analyse transaction strings, merchant identifiers, MCCs, geolocation, and historical behavior to assign accurate categories. AI-driven categorisation improves accuracy compared to rules-based systems and is widely adopted by banks, fintechs, and expense platforms to power insights, budgeting tools, fraud detection, and reporting.

Industry insights

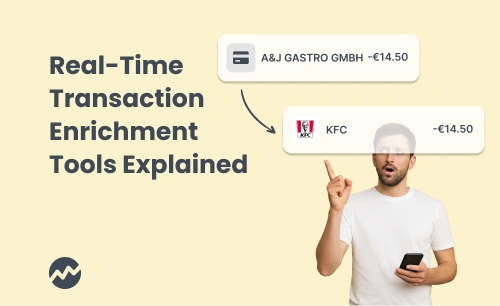

Real-Time Transaction Enrichment Tools: Key Questions Answered

Transaction data is only valuable when it’s clear and usable. It helps banks and fintechs transform raw payment strings into meaningful insights customers can instantly recognise - improving trust, experience, and engagement. Let’s dive deeper.

Industry insights

Beyond Banking: Bridging Payments, Play and Personalisation

Banking is stretching its legs. Its main mission might still be balances and bills, but it’s also phones, travel data, game culture, groceries, even sports pits. In Europe, the most interesting shifts are practical, a little playful, and surprisingly useful.

Industry insights

The Hidden Costs of Building In-House Data Enrichment Solutions

On paper, building your own data enrichment solutions sounds smart. You’ve got capable engineers, a decent data science team, and a roadmap that seems to allow for it. But here's the thing: enriching transaction data isn’t just a technical project, it’s a constantly evolving project. And for many banks and fintechs, what starts as a quick fix turns into a long-term liability.

Industry insights

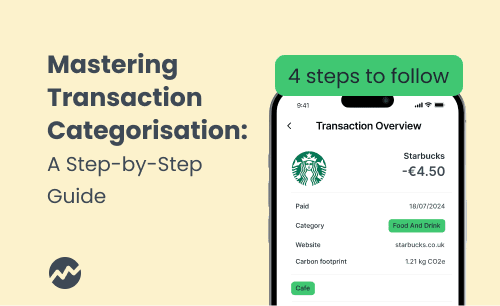

How to Categorise Transactions: A Step-by-Step Guide

If you've ever looked at a bank statement and seen chaotic strings of data, you’re not alone. Customers expect clarity. They want to know what they spent, where, and on what. On the other hand, the backend needs to know how to handle data correctly so both sides are happy.

Industry insights

Responsible Banking Done Right: The Top 5 Banks and How They Lead

In recent years, more and more banks and financial institutions focus on sustainability as a core component of their operations. This shift towards responsible banking (also known as ethical banking) is mostly a response to the pressing global challenges of climate change, social inequality, and environmental degradation.

Industry insights

Mobile Banking Innovations: The Role of UX & UI in Next-Gen Digital Banking

The financial industry has undergone a pretty radical transformation in the last decade, with mobile banking becoming a primary interface between banks and their customers. As highlighted by recent research from Branch, the mobile app industry has been seeing significant growth during the past several years and this trend extends to the financial sector.

Industry insights

Cracking the Code: The ABCs of Transactional Data Enrichment

Have you ever been in a meeting or conference, nodding along as industry experts toss around terms and abbreviations that sound like a foreign language? It can feel overwhelming, especially in the financial world, where terms and slang evolves fast.

Industry insights

Better Banking App: How To Increase Active Users in 6 Effective Ways

Banks have good reasons to encourage customers to use their mobile apps more often. First, it helps them make more money by offering products and services directly in the app. Second, it improves the customer experience - for example, by showing clearer payment information - and helps the bank work more efficiently.

Industry insights

Beyond MCC Codes: Why Accurate Transaction Categorisation Is the Future of Banking

Merchant Category Codes (MCCs), initially designed as a universal standard for categorising transactions, have long been the baseline for transaction classification in banking. However, their limitations have created challenges that resonate across banking operations, customer experience, and sustainability initiatives.

Industry insights

From enemies to allies: The Cooperation Between Banks and Fintechs

This gathering of experts and professionals not only provided a valuable opportunity for us to learn about the latest trends and developments within the industry but most importantly, our Head of Partnerships, Simon Koci, had a chance to host and moderate a panel discussion on the topic of Cooperation Between Banks and Fintechs.

Industry insights

How Data Shapes the Future of Banking UX

User experience (UX) today goes beyond a nice-looking interface or a conveniently usable application; it is about making data actionable, intuitive, and applicable in whatever interaction is made by the user.

.png)

Industry insights

Biggest Myths in Digital Banking Busted

Digital banking has advanced considerably, but like in any other industry, many myths and misconceptions are floating around. These often cloud understanding and limit the adoption of new technologies and ways to level up digital banking.

Industry insights

Top 5 Digital Banking Features for Generation Z

With technology moving forward faster and faster every day, digital banking is becoming the new main way we interact with our finances. And Gen Z is setting the pace. Born into a digital age, Gen Z demands more from their banking experience than ever before. Let's take a deep dive into the top 5 most used and demanded digital bank features and how is modern financial sector adapting to the needs of the new generation of users.

Industry insights

8 Strategies to Boost Customer Digital Engagement in Banking

Maintaining customer loyalty has always been and should always be a key priority for financial institutions. With many banks offering similar services and rates, it is imperative to differentiate yourself by creating a unique and satisfying experience tailored to your customers.

.webp)

Industry insights

Account Openers to Profit: A Guide for Banks

Today, the financial world is all about mobile-first convenience. Opening a new account has never been easier. Yet, while an efficient account-opening process gets your foot in the door, it doesn't guarantee a meaningful and, most importantly, long-lasting relationship. The real challenge lies in ensuring that new customers don’t just open an account and fade into inactivity but instead evolve into loyal, profitable clients.

Industry insights

Key Features of Digital Banks: Insights from a Leading Fintech Expert

I’m Ondřej Machač, a FinTech enthusiast with a passion for pushing the boundaries of financial technology. I currently manage over 15 bank accounts across the EU, constantly testing them to stay on top of the latest trends in banking and fintech. I regularly share my insights in Fintree, the largest FinTech magazine in the Czech Republic, which I founded. Additionally, I work at Roger, one of the largest Czech fintech companies, which closely collaborates with banks.

Industry insights

11 UX Laws in Digital Banking

User experience (UX) in digital banking isn't merely about good aesthetics. It's deeply rooted in science and psychology, governed by established laws that guide user interactions and decision-making. Here are 11 key UX laws, explained with examples relevant to digital banking applications.

Industry insights

The Reality of Building a Digital Bank

The total number of digital banking customers now stands at approximately 1.1 billion worldwide, and 20 neobanks now serve 10 million or more customers (and 39 with more than 5 million), placing several of them among the top 5 or 10 largest banks in their country. This article summarizes the best of "How to Build a Digital Bank", a detailed guide to building a digital bank, and insights from The Reality of Building a Digital Bank webinar. To complement this narrative and provide a real-world perspective, we present an article on the reality of building a digital bank.

Industry insights

How to Improve Banking App Store Reviews

For almost any app in the modern digital age, app store reviews are key to success. They serve as a public measure of your app’s quality and can significantly impact user acquisition and retention. Digital banking is no different. According to a survey by Alchemer, 77% of consumers read at least one review before downloading a free app, and 80% of users will not download an app if they see negative reviews about its performance.

Industry insights

Becoming the Bank of Choice: How to Stand Out From the Crowd

Switching banks is more common than one might think. According to a satisfaction survey conducted by J.D. Power, nearly 13% of consumers are expected to switch their primary bank this year. The most common reasons for this shift include high fees, poor customer service, lack of convenient digital banking features, and better offers from competitors. Is there a way to be a part of the client's life journey indefinitely? Let's find out.

Industry insights

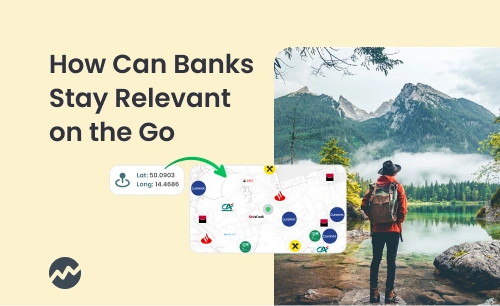

Banking on Travel: How Can Banks Stay Relevant on the Go

Travelling is becoming more popular and digital each year. According to a recent UNWTO survey, international tourist arrivals (overnight visitors) increased by 5% in 2023, reaching 1.4 billion travellers globally. As travel becomes more active, the role of digital banking is evolving accordingly to meet the needs of modern explorers. From seamless transactions to personalised financial services, digital banking is pushing the travel experience to a new level.

Industry insights

A Comprehensive Guide for Banks to Ensure AI Act Compliance

Following the updates to the AI Act, it’s essential for banks to ensure their AI systems comply with these new regulations. This guide breaks down the process into manageable steps, making it straightforward for digital banking experts to follow and ensure compliance.

Industry insights

How to Build a Digital Bank in 2024

As digitalization progresses across markets, a new generation of banks is becoming increasingly popular. We are talking about digital banks, or neobanks, if you will. These banks operate entirely online, offering a suite of financial services without the need for physical branches. APIs, like those from the TapiX team, have been playing a major role in this shift, enabling seamless integration and functionality that enhance user experience and operational efficiency. Let's dive deeper into the process of building a digital bank in 2024.

Industry insights

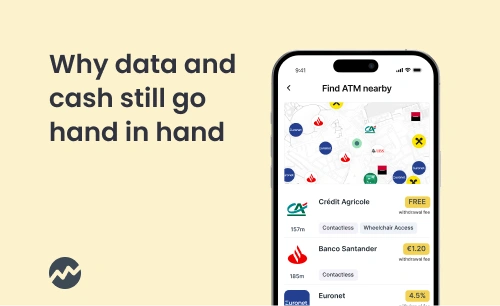

The World of ATMs: Why cards and cash still go hand in hand

Automated Teller Machines have evolved significantly since their introduction in the 1960s. Initially designed to dispense cash outside banking hours, ATMs now offer a range of services, from depositing checks to transferring money between accounts. Today, there are over 3.5 million ATMs worldwide that are visited by users on average at least 8-10 times a month. Even cryptocurrency ATMs are on the rise, with more than 39 000 used worldwide.

Industry insights

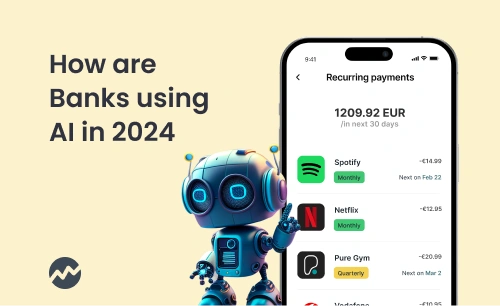

How are banks using AI in 2024

With the implementation of the EU AI Act providing a regulatory framework for ethical and responsible AI adoption, banks and financial institutions are starting to pay close attention. What exactly is AI used for in modern banking? Let's dive into different use cases and what it means for banks.

Industry insights

From Chatbots to Credit Scoring: How the AI Act Affects Banking

For the past several years, AI has captured the attention of many industries, including finance and banking, where it’s been helping institutions to automate many important services and solutions. In the meantime, the European Union has taken a significant step forward with the introduction of the EU AI Act.What exactly is the EU AI Act, and why does it matter? In this article, we'll introduce the basics to provide you with a comprehensive understanding before we explore its implications in more detail and check the AI readiness of the banking sector. According to Arizent survey, 56% of users would welcome the help ofAI in their financial recommendation services while 48% see it as a tool for evaluating credit or loan applications.

Industry insights

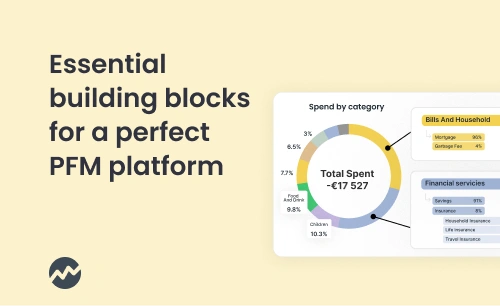

Bending data: Essential building blocks for a perfect PFM platform

With banking going digital and more personal than ever before, Personal Financial Management tools (PFM for short) have become indispensable for individuals seeking to take control of their finances. To build the perfect one...

Industry insights

Youth Banking Trends: Mapping Digital Banks for Kids, Teens, and Gen Z

While digital banking is undergoing a rapid transformation and growth, a new phenomenon is emerging – Kids Banking. This concept not only represents a revolutionary way for today's children to learn about money but also offers a unique opportunity to develop financial literacy from a very young age. Fintechs such as Pocket, GoHenry and neobanks such as Revolut are jumping on the trend.

Industry insights

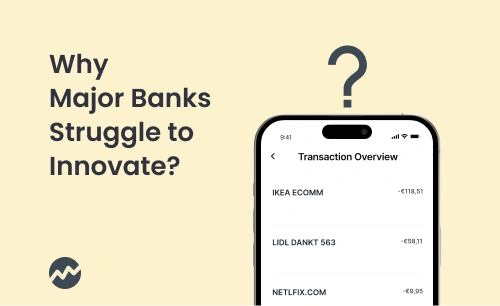

Why Major Banks Struggle to Innovate: A Deep Dive into the Fintech-Bank Collaboration

Banks are at a crossroads between conservative survival or gradual implementation of new technologies and adaptation to their customers' requirements. Although they have considerable resources and a solid client base, they do not always manage to adapt in time. In this article, we will explore the key reasons for this and highlight the importance of building a spirit of innovation, engaging in technology development and partnering with fintech firms.

Industry insights

Beyond Transactions: Banks as Lifelong Partners - A Contextual and Marketplace Perspective

Modern banking is becoming more personalized than ever, thanks to strategies like contextual banking and marketplace banking. This article explores how these strategies are changing the way banks help clients in different stages of their lives – from student loans and discounts to mortgages and business loans.

Industry insights

How Gamification in Banking Is Levelling Up User Engagement in Mobile Apps

The concept of gamification, originating from the video game industry, has transcended into various fields of technology in the early 2000s as a novel marketing strategy. As banking apps and platforms continue to rise, gamification is reshaping how banks and fintech companies interact with their users, drawing valuable lessons from engaging video game experiences.

Industry insights

Personalisation in banking - the key to your customers’ heart

Customer expectations of their banking platform are evolving rapidly, especially when it comes to personal finances. As fintech firms continue to innovate, one trend is becoming very apparent: hyper-personalisation.

Industry insights

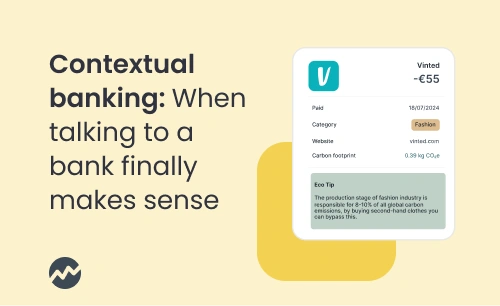

Contextual banking: When talking to a bank finally makes sense

Imagine a world where banks are not just a place you put your money, but they actually understand your needs. They speak in a way that makes sense and help you navigate your finances. If you ask any fintech enthusiast with over 20 bank accounts and a plethora of fintech platforms, they constantly explore and seek the most from their banking apps.

Industry insights

What are MCC Codes and Why Banks Need More for Reliable Payment Categorisation

We decided to provide our insights into the power of strictly MCC-based categorisation and its limits. Categorisation is important for credit risk scoring and it is the basis for Personal Finance Management tools. When we analysed our categorisation with MCCs, we saw that only 53% of transactions could be easily and reliably categorised based on their MCC code. Let's look at the most frequent problems we identified that make MCC usage more difficult than it may seem at first glance.

.webp)

Industry insights

What does Generation Z expect from banking?

Everly and Tapix joined forces to organize a panel on the topic of Future of Banking: Gen Z. Join us for an exciting online discussion with speakers from W1tty, MyMonii, Gimi & Lunar on the 7th of December at 4PM CET. In this article we provide highlights regarding the Gen Z Banking landscape

Industry insights

Why do non-bank issuers offer credit cards?

The market for digital lending from non-bank credit card issuers and fintech firms is becoming increasingly popular among consumers. It is a modern and innovative form of financing that provides a faster and more accessible alternative to traditional methods. The long queues at bank branches have come to an end. Customers want a loan in a few clicks and they want a card full of benefits to go with it. The BNPL trend with players like Klarna, Zip and Twisto shows this.

Industry insights

Sustainability in Digital Banking: Trends and the Crucial Roles of Banks and Consumers

Sustainability is becoming an increasingly key issue in digital banking, both from the perspective of consumers and from the standpoint of banks reflecting their interests as well as their ESG strategy. The interest also reflects a growing awareness of the climate change we are facing. In this article, we take a detailed look at why green direction and green thinking in banks and their banking applications are coming to the foreground now.

Industry insights

How to build top-notch Personal Finance Management tools? Focus on data

Rising inflation, economic recession, rising prices of absolutely everything... The times are not exactly conducive to splurging, quite the contrary.

Industry insights

What are the latest trends in fintech product?

Recently, Simon Koci, the Head of International Partnerships at Tapix by Dateio, was featured in a report, where he discusses his views on the future of fintech. In this article, we highlighted the findings of a recent survey of 100 fintech product specialists and provided insights into latest banking product trends.

Industry insights

CEE22: Cooperation between banks and fintechs. Interview with Šimon Kočí

SME Banking club sat down with Šimon Kočí, Head of International Partnerships for Tapix by Dateio, who will be moderating a panel discussion on the topic of Cooperation between banks and fintechs the upcoming CEE SME Banking Conference in Prague.