The August financial literacy survey by the Czech Banking Association and the financial market agency Ipsos showed that the current situation threatens the family budget of 71% of Czechs. A similar trend at the European level was confirmed by a McKinsey & Company survey in July 2022, according to which rising prices are the main concern for 53% of Europeans.

Time favors the prepared. And those who have a handle on their money

Finances need to be in order today (and not just today), and personal finance management (PFM) apps are slowly but surely becoming an essential tool for maintaining (and ideally improving) the financial health of individuals and households. Most banks and financial institutions already offer them, and it's certainly the right direction: more and more people are reaching for tools to help them keep their spending in check. And it's not just those whose accounts are empty a week before payday.

According to the Czech Banking Association, the vast majority of Czechs manage their money online, with more than 60% of them using their mobile phones. Financial institutions such as Revolut, as well as traditional banks, have their own PFM tools for taking care of personal finances. It is probably safe to say that in most countries, it would be difficult to find a single bank that does not offer at least a basic mobile app and budgeting tools (for better or worse). And then, of course, there are specialist apps such as the highly rated Spendee or Wallet from Czech developers. Both of these can be linked directly to a user’s bank account.

Anyone who doesn't provide at least some functionality to help manage personal finances is as good as gone. But those who can offer more (data, tools, and reports) will gain a competitive advantage in an increasingly saturated market.

3 obstacles to effective financial management

The 21st century, and specifically the post-pandemic era, favors online payments and cash is taking a backseat, making personal finance management apps even more important. This, in turn, requires the PFMs to be even more user-friendly. The complicated manual process of writing receipts and entering one’s spending is no longer necessary. The data already exists or can be pulled directly from the bank account history, thus eliminating a time-consuming task for consumers.

But what that data looks like is another question altogether, and it's related to the 3 main problems that most people have when managing their money:

1. Transaction recognition

An incomprehensible jumble of letters and numbers doesn't help much with payment identification and often ends up with reports of seemingly fraudulent payments that cost banks time and money to resolve. At the same time, it is an unnecessary hassle for the user.

2. Sorting payments

Sorting transactions into categories by type, merchant, or service provider (supermarket, mom-and-pop drugstore, Netflix, etc.) can make it much easier to decide where to slow down and where there is room to spend.

3. Canceling subscriptions

Yes, we're talking mainly about subscriptions, whether it's to TV services, magazines, or the increasingly popular boxed diets. While subscribing to these is a matter of a click, unsubscribing from them often becomes a nightmare. Even the smallest of payments that disappear discreetly from your account each month can be the final straw that causes the cup of balanced finances to overflow.

Personal finance management tool providers who can tackle these 3 obstacles to effective money management will not only have happier clients but also a leg up on the competition.

The key to top personal finance management tools? Data, data, and more data!

There are a number of factors behind the success of the best personal finance management tools, but one of the most important is financial data enrichment: additional information that the provider is able to obtain by linking existing data to external sources without having to ask the customer for it.

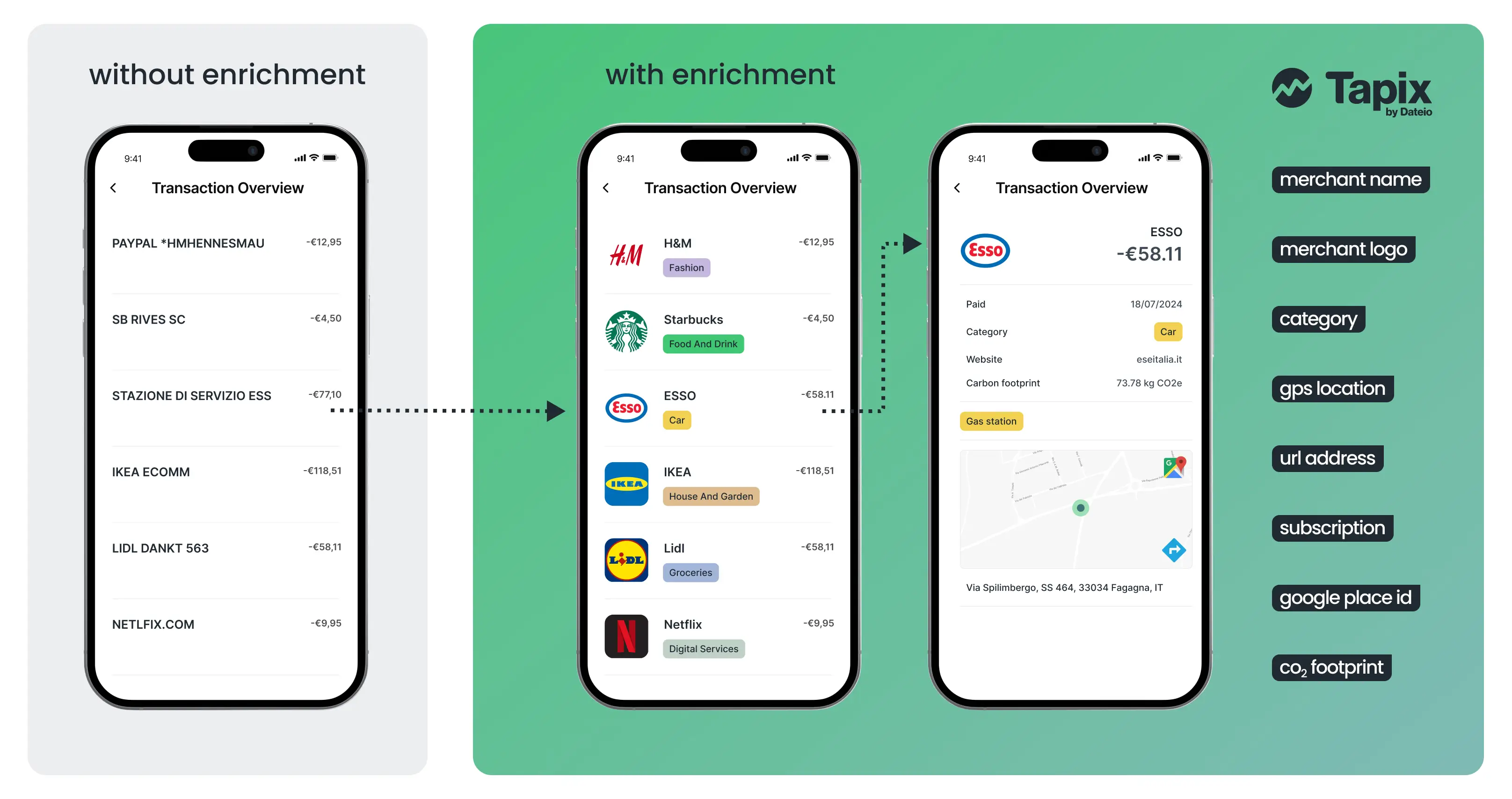

Data Enrichment turns a string of numbers and letters into a comprehensive set of detailed data about each transaction, including the merchant's name and logo, store address, date, time, amount, and category of the transaction, and more.

In practice, it looks like this:

With the additional information, users can not only easily recognize their transactions, but they can also sort them into related categories. They can quickly see, for example, how much they spend each month on groceries, how much gas costs, and how much goes to watching their favorite movies. Deciding where to cut back is then much easier.

The same then applies to canceling unused subscriptions: in a well-categorized list of transactions, it's not difficult to spot services that regularly steal (albeit not huge sums) from the financial pie.

Data enrichment: a relief for clients, but also for the bank

It is not only clients who benefit from transactions in which people do not get lost and which they can easily verify, but also the bank or financial institution itself. It significantly reduces the number of disputes and refund requests in cases of 'friendly frauds' (payments that people do not recognize on their statements due to insufficient information), and thus unnecessary administrative costs.

The logical consequence is, of course, higher customer satisfaction and ultimately a competitive advantage in an increasingly saturated market. Low service charges are far from being the only thing people expect from their bank.

Choosing a data enrichment partner matters

There are a number of payment data enrichment providers to choose from. But if you offer an app or other financial management tools and are thinking about a new partner (or changing an existing one) to help you with your data, choose carefully. Not everyone can enrich all data, and not everyone can do it equally well.

Among the 6 criteria to consider are the quality of the data offered, the ease of integration into existing systems, and of course, the cost of the solution.

If you make the right choice, you win in many ways. Those who can offer their clients a well-functioning and efficient personal finance management tool in today's economic mummery will continue to benefit in the future.