Introduction

The framing has shifted sharply since 2023. Green banking is no longer a challenger narrative about nimble start-ups pushing traditional institutions forward. It's a regulated discipline with enforcement actions, simplified reporting rules, and a widening gap between regions. The EU has just adopted the Omnibus I Directive (in force 18 March 2026), which narrows mandatory CSRD reporting to companies with over 1,000 employees and €450m+ turnover while simplifying ESRS standards. The US, by contrast, has reversed on federal climate commitments, and ESG funds there saw $84 billion in net outflows in 2025.

Against that backdrop, the question for banks is how to do green banking credibly without being fined for greenwashing or sued for non-compliance.

Green Europe: Demand Determines Supply

The underlying demand hasn't gone anywhere. The European Commission's 2025 Eurobarometer on Climate Change - surveying 26,319 EU citizens across all 27 member states - found that 85% consider climate change a serious problem, 81% support the EU reaching climate neutrality by 2050, and 88% want the EU to accelerate renewables and energy efficiency. Nearly four in ten Europeans (38%) now say they feel personally exposed to climate-related risks in daily life.

Consumer behaviour has followed. A 2024 EY Future Consumer Index found that 61% of European consumers feel they need more information to make sustainable choices, 51% want to buy more sustainably but lack clearer data, and 64% are willing to change their behaviour when they're given reliable numbers to act on. That last figure is the important one for banks: data quality is the main demand.

But awareness doesn't always translate into switching behaviour. An iResearch Services retail banking survey found that while 54% of consumers believe their bank should focus more on sustainability, only 22% actually factor it into their choice of bank. Greenwashing concerns are a big part of that gap - 87% of financial services leaders acknowledge greenwashing as prevalent in the industry.

Where there is demand, there is supply, and more institutions and initiatives are emerging to focus on clients who care about the planet and the environment.

Green and Climate Fintech: What It Is and What Role It Will Play

The climate fintech category has matured into an institutional market. Sustainable finance is embedded into mainstream bond issuance, core banking product lines, and central bank supervision. Bloomberg Intelligence projects ESG assets under management will hit $40 trillion by 2030. Growth has cooled from the 2020–2022 surge as regulators tightened definitions and investors scrutinised labelling, but the underlying direction hasn't reversed in Europe.

Activities combining the environment, finance, and digital technologies are most often mentioned in the context of alternative players, like financial technology startups and companies, collectively referred to as green banking initiatives, or climate fintech.

Green Finance: Banks Are Waking Up

Despite the emergence of green banking products at alternative financial institutions, they are now the rule rather than the exception even at traditional banks. The model of collaboration and partnership with new players and fintech startups is often applied here, bringing technology that banks can successfully use and integrate into their existing systems or mobile apps with relative ease.

Green savings, green bonds, and green loans are the most visible parts of this shift. In 2021, Raiffeisenbank Czech Republic launched its Green Bond Framework and issued €350 million in green bonds. Green mortgages are now standard across most European markets - properties with a higher energy rating typically qualify for longer terms and slightly lower interest rates (often a tenth of a percentage point), which changes consumer economics for EV-ready homes, heat-pump retrofits, and new energy-efficient builds.

Banks that want to surface these products effectively need to know which customers are already behaving sustainably - and that requires merchant-level transaction data. This is exactly the gap Tapix's Green-Products Awareness solution is designed to close: identifying sustainable spending patterns in the transaction feed and flagging the right moments to offer green financial products.

Current Trends in Green Banking

Green banking initiatives can be found across all sections of the financial industry. According to the Green Digital Finance Alliance, there are a total of 8 product categories within green fintech. Let's take a look at some of these in more detail.

Payments

Payments are key mainly because the overall volume of consumer transactions is huge and purchasing behaviour is closely linked to carbon footprint. The potential to bring about change towards sustainability is therefore significant for payments. Typical examples of payment initiatives include carbon offsets, eco-friendly packaging for online purchases, or rounding up the purchase amount and using the difference to plant trees.

Companies like Adyen or Svalna have built credible products in this space. Worth noting: carbon-offset integrations at the point of sale have come under increased regulatory scrutiny in 2024–2025 for the quality of voluntary carbon credits, so any bank integrating offsets needs to vet the underlying registry carefully.

Banking

Challenger banks still offer some of the clearest examples of consumer-facing green banking, though the landscape has consolidated. Tomorrow (Germany), bunq (Netherlands), and Triodos Bank lead the European category - Tomorrow partners with ecolytiq to surface carbon footprint data in-app, bunq integrated Tapix Eco Track to give customers transaction-level CO2 estimates, and Triodos remains the benchmark for values-based banking with a balance sheet built entirely on sustainable lending.

Incumbent banks have caught up faster than most expected. Raiffeisenbank Czech Republic integrated Tapix's Eco Track into its mobile app for more than one million active customers, displaying estimated carbon footprints at the merchant level rather than relying on MCC-based averages. Raiffeisen in Albania became the first bank in the country to launch a carbon footprint feature for retail customers. HSBC rolled out an ecolytiq-powered carbon view for its Kinetic SME customers in Europe in 2024. KBC in Belgium has scaled its point-of-sale bike loan programme. These are features reaching millions of users through the primary banking app.

The cautionary note comes from the US. Aspiration, once the poster child of climate-focused neobanking, collapsed in 2025 after a $248 million fraud scandal; its co-founder pleaded guilty to wire fraud, and the company had been under DOJ and CFTC investigation for misleading customers about carbon offset quality. The consumer brand was rescued and rebranded as GreenFi in April 2025. For banks adding climate features, the lesson is that sustainability claims now carry the same regulatory and reputational risk as any other product disclosure.

Loans and Investments

These two areas, including pensions, have seen a number of positive changes in recent years thanks to fintech and the use of new technologies. They brought speed, transparency, and options such as P2P lending or micro-investments.

Initiatives to reduce climate change and environmental impact include lending for green projects (including green mortgages) and investing in ESG assets. Earlier projections from Bloomberg Intelligence and Barclays had forecast ESG assets worth over $53 trillion by 2025, but the market matured more slowly than those early forecasts assumed. The substance has shifted from headline AUM numbers to product credibility: how are green bonds verified, how is ESG fund labelling audited, how can a green mortgage actually prove the underlying property's energy performance?

KBC, for example, offers bicycle retailers the possibility to provide credit financing to their customers at the point of sale. Spain's Micappital Eco offers sustainable investments, and in May 2025 La Banque Postale launched ESG offerings across its entire savings portfolio - life insurance, ordinary securities accounts, and share savings plans.

Insurance

Insurance companies are the world's largest asset managers after pension funds, so their role in efforts to reduce climate change and environmental impacts is crucial. They are themselves highly vulnerable to climate change which reinforces their motivation to act.

Green initiatives by insurers include discounted rates for low-emission or electric vehicles, eco-friendly appliances, and ridesharing-specific coverage, among others.

Cryptocurrencies and Blockchain

Blockchain's role in climate finance has stabilised around a narrower set of use cases - mainly tokenised green bonds, carbon credit registries (though these have faced greenwashing scrutiny after Verra and Aspiration controversies), and renewable energy certificates. The energy intensity of proof-of-work chains like Bitcoin remains a credibility problem for the broader climate fintech story. Ethereum's 2022 shift to proof-of-stake cut its energy consumption by over 99%, making it the more common backbone for tokenised sustainability instruments.

In April 2025, China issued its first sovereign green bond on the London Stock Exchange's Sustainable Bond Market, and Denmark launched the first sovereign bond under the EU Green Bond Standard as a "green twin bond" - innovations that rely on transparent, verifiable infrastructure rather than crypto speculation.

Carbon Footprint Insights

Clients want to know what effect their purchases are having on the environment. They are turning to sustainable brands and fair trade products in preference to mass production, and they are asking their financial institutions to give them the data to act on.

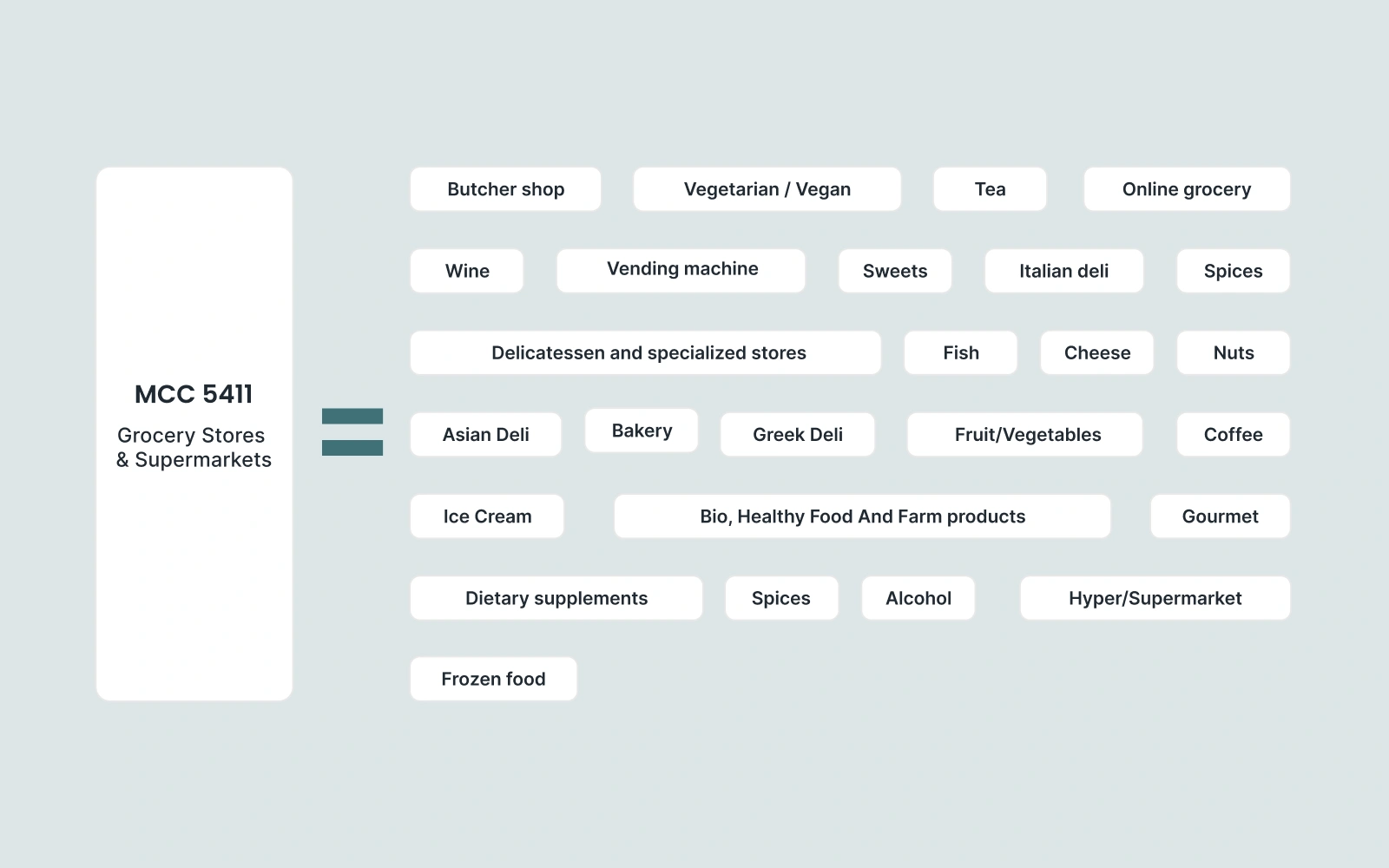

Calculating the carbon footprint of a transaction is harder than it looks. It's still overwhelmingly determined by the MCC code - a four-digit number for each transaction processed by Visa or Mastercard that classifies businesses based on the type of goods or services they sell. The problem is granularity. Take MCC 5411 - Grocery and Supermarkets. Tapix's database includes 31 different store types under that single code, from hard discounters to organic specialists to gas-station convenience shops. Each has meaningfully different consumer behaviour and a different emissions profile, yet MCCs treat them as one. When banks calculate a carbon footprint on top of MCC alone, the result is an average of averages - easy for customers to dismiss, and hard to build a product on.

Eco Track is an API-based data enrichment service from Tapix that goes deeper, all the way to the merchant level. Built by Kateřina Linhartová and her team at Dateio, Eco Track combines Tapix's core enrichment (merchant name, logo, GPS, URL, category) with country-specific emission coefficients tuned at the merchant-type level. The result is a qualified estimate for individual transactions rather than a category average. As Kateřina put it in a recent interview on the Tapix blog, a raw figure like "3.5 kg of CO2" doesn't mean much on its own - users need context to turn data into behaviour.

A carbon footprint without data? Information is power

Climate change and mitigation initiatives have significantly increased the demand for new and more accurate data sources in recent years. Data is a key enabler for global change towards reducing environmental impacts of human activity.

While an overall figure on the carbon footprint of individual clients or portfolios is interesting, it isn't nearly as useful as it could be without supporting data. To take specific action — for example, to reduce purchases of goods and services with a high carbon footprint — it's necessary to know which transactions contributed to emissions and by how much. The predictive power of MCC codes, which are most commonly used to determine carbon footprints, is limited. A 2023 Tapix case study showed that up to 63% of transactions categorised on the basis of MCC codes are erroneous.

Banks can now offer their customers enriched payment data that is more accurate and reliable than that based on MCC codes, while being easily integrated into mobile apps via APIs. One such solution is the Tapix API from Czech fintech Dateio. In its key markets across Europe and the Middle East, Tapix achieves 99.99% data accuracy across 120+ active markets and 1.5 billion+ monthly transactions, enriching payments with clean merchant names, logos, GPS locations, URLs, categories, and eco-tags. Combined with Eco Track, these replace MCC-based carbon footprint estimates and allow institutions to reward clients for genuinely sustainable spending patterns.

Development is Moving Forward

The barriers have shifted since 2020. Technology and data coverage are no longer the bottleneck - the constraint now is regulatory clarity and the credibility of sustainability claims. In the EU, the Omnibus I Directive (adopted February 2026, in force 18 March 2026) has narrowed CSRD reporting to entities with over 1,000 employees and €450m+ turnover, simplified ESRS standards, and introduced a "value-chain cap" to prevent large companies from trickling ESG reporting burden down to SMEs. The European Central Bank has moved into enforcement territory, fining ABANCA Corporación Bancaria for failing to properly assess climate risk - the first high-profile supervisory enforcement of its kind.

In the US, the direction has reversed under the current administration, with ESG funds seeing $84 billion in net outflows during 2025. China, conversely, continued to expand green finance infrastructure through its 15th Five-Year Plan (2026–2030). The result is a three-speed global landscape: Europe tightening and simplifying, the US retreating, and China accelerating. For banks operating across these regions, the practical priority in 2026 is building data architecture that can support defensible, audit-ready sustainability claims regardless of which regulatory regime applies.

AI has become the accelerant the sector lacked a few years ago. AI-driven geospatial analytics and climate-scenario modelling are making physical-risk assessments more comparable across markets, and AI-powered ESG platforms are allowing banks to scale impact measurement without the manual overhead that used to make transaction-level sustainability work expensive.

For banks, the combination of enriched transaction data and AI-based analytics is what turns sustainability from a compliance exercise into a customer-facing product.