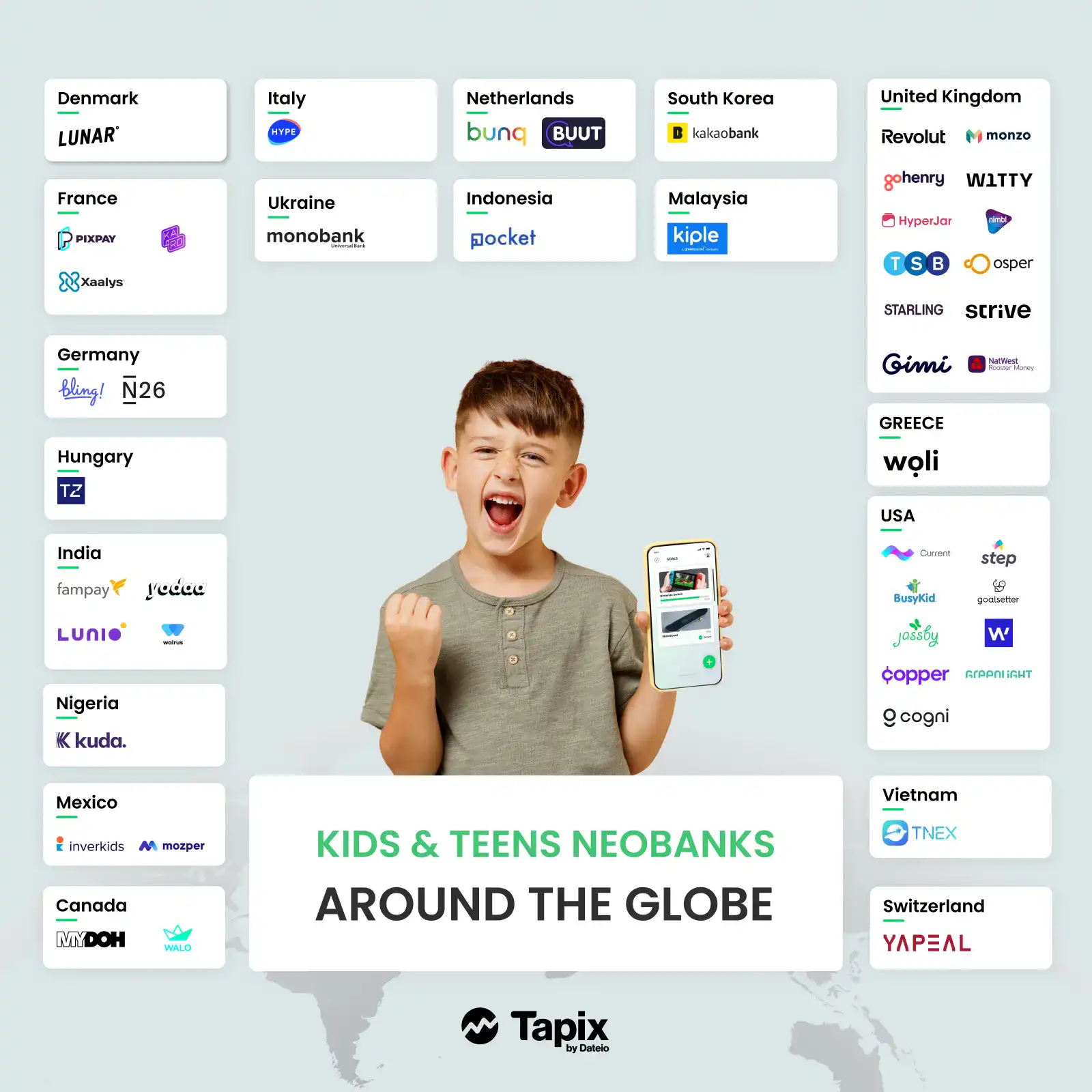

While traditional banking is undergoing a rapid transformation and growth, a new phenomenon is emerging – Kids Banking. This concept not only represents a revolutionary way for children to learn about money but also offers a unique opportunity to develop financial literacy from a very young age. Fintechs such as Pocket, GoHenry and neobanks such as Revolut are already pursuing the trend. In this in-depth analysis, we look at the key aspects of Kids Banking, its benefits, challenges and impact on future generations.

Generation A and Z are growing up in an era of instant shopping through online apps and brick-and-mortar stores with contactless cards or fingerprint authentication. Even their pocket money is often given digitally: while half of the parents (52%) who took part in the survey still give it in cash, a significant number (43%) pay it by bank transfer.

This proportion naturally increases with age. By the age of 11, at which they can open their own bank account, most children receive their pocket money in coins and banknotes. At age 12, they are equally likely to receive money by bank transfer. By the age of 16, this proportion rises to 62%, as stated by the survey from TheTimes.co.uk.

Further research from Finder.com shows that the average pocket money for children in the UK is £7.11 a week. Nine out of ten children (92%) receive pocket money. Four-fifths of children (84%) save at least some of the pocket money they receive. Three in five children (61%) in the UK manage their money using an app. One in eight parents (13%) admit that they have never taught their children about money, which is something that banking apps such as GoHenry or Pocket can help with.

The amount of pocket money increases on average with the age of the children. The average weekly pocket money for a four-year-old starts at £3.21, while for a 17-year-old it averages at £14.52. Entering adolescence also brings an increase in pocket money, with the average amount rising from £7.37 to £8.93 between the ages of twelve and thirteen. By the age of 14, the average pocket money is £10.67 per week. This is therefore a substantial market for banks to tap into.

Why Do Parents Want Controllable Accounts?

It's no wonder parents are looking for financial apps for their children. Why? The many benefits include things like parental control directly in the app, notifications on children's spending, easy-to-set limits for certain types of transactions, and some banks even allow parents to set up kids draws that release a locked amount of money when met. With these options, who would want to give their kids cash?

So why are fintechs and financial institutions going in this direction in the first place? For parents, it's often a dealbreaker because they can easily control everything from one app. What does the bank get out of it? Often, the whole family will switch to such a bank, taking advantage of one ecosystem, resulting in the benefits of issuing multiple cards, joint savings, and investment products. Thus, an interesting cross-sell from the bank's perspective and builds a long-term revenue stream. This is the direction taken by the US SoFi, for example, or the UK's Revolut.

Clean Merchant Information

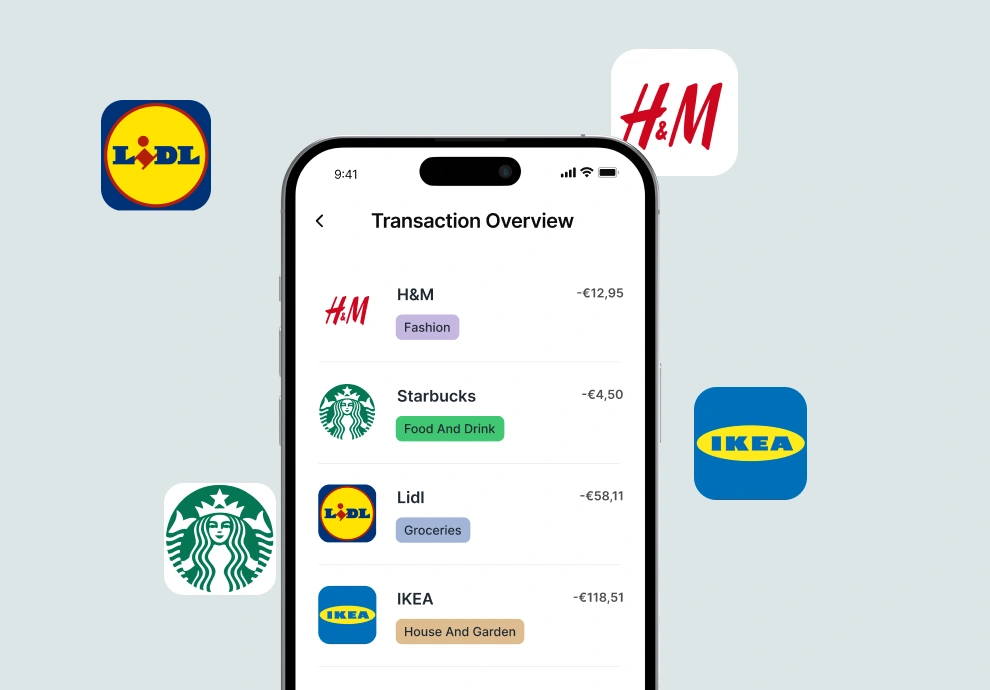

One of the most important features of Kids Banking is the emphasis on "clean merchant information". This feature ensures that merchant and transaction information is presented clearly and transparently, allowing parents to easily monitor and approve their children's purchases.

In practice, this means that every transaction is documented in detail, including the name of the merchant and the type of goods or services purchased.

Clean merchant information is becoming a compliance and trust baseline, driven by network standards such as Visa’s enhanced merchant data requirements and the industry’s shift beyond MCC-only labelling.

For youth-focused banking and fintech apps, transaction clarity is not a cosmetic upgrade. It directly shapes how young users understand money. If a payment appears as a vague label or a generic MCC category, the learning moment is lost.

Tapix works with banks and fintechs including Bling card to enrich each transaction with a consistent merchant identity, recognisable name, logo, and accurate merchant-level category. The result is a transaction feed that is understandable by design - for children and transparent for parents.

With enriched transaction-level data, banks can:

- Present a truly clear transaction history suitable for kids and parents

- Reduce reliance on MCC-only labels that obscure what the purchase actually was

- Support parental controls and limits using accurate merchant/category identification

- Strengthen financial literacy by making spending understandable, not guesswork

Main Points Parents Seek Out

Clean Payment History

Often, children's transactions are mirrored into the parents' app, who can set various restrictions, budgets, etc. This transparency is key not only for security and control but also as an educational tool. It helps children understand the value of money and the consequences of their financial decisions.

Automating Pocket Money

Parents can set up a regular weekly allowance that can increase in certain circumstances. They can also set up a to-do list where a portion of the allowance is released upon completion. For example, €10 for washing the dishes, a better grade at school, etc.

Blocking Merchants

Parents can block payments for gambling, betting shops, newsagents, alcohol and other inappropriate merchants for underage children. Or conversely, they can set a limit - for example, monthly payments at McDonald's, limiting the child's visits to 2-3 per month.

Displaying the Logo In Notifications

Neither the child nor the parents don't have to spend a lot of time searching for the merchant where the payment was made and then making a decision. By correctly identifying the merchant with category and logo, they can make decisions immediately.

Learning Responsibility

Kids' banking apps often include budgeting tools and expense tracking features, allowing kids to learn the basics of money management. Parents can set weekly or monthly budgets, create savings goals, and track progress with their kids. Thanks to the categorisation, this activity and tracking of spending is fun and creates a positive habit for children. This interactivity not only promotes healthy financial habits but also strengthens the relationship between parents and children through joint financial planning and discussions.

Gamification: Learning Through Fun

Gamification, or the use of gaming elements in the learning process, is another key element of Kids Banking. Apps often use badges, trophies and challenges to motivate children in learning about financial concepts and money management principles. This strategy increases engagement and interest in financial education.

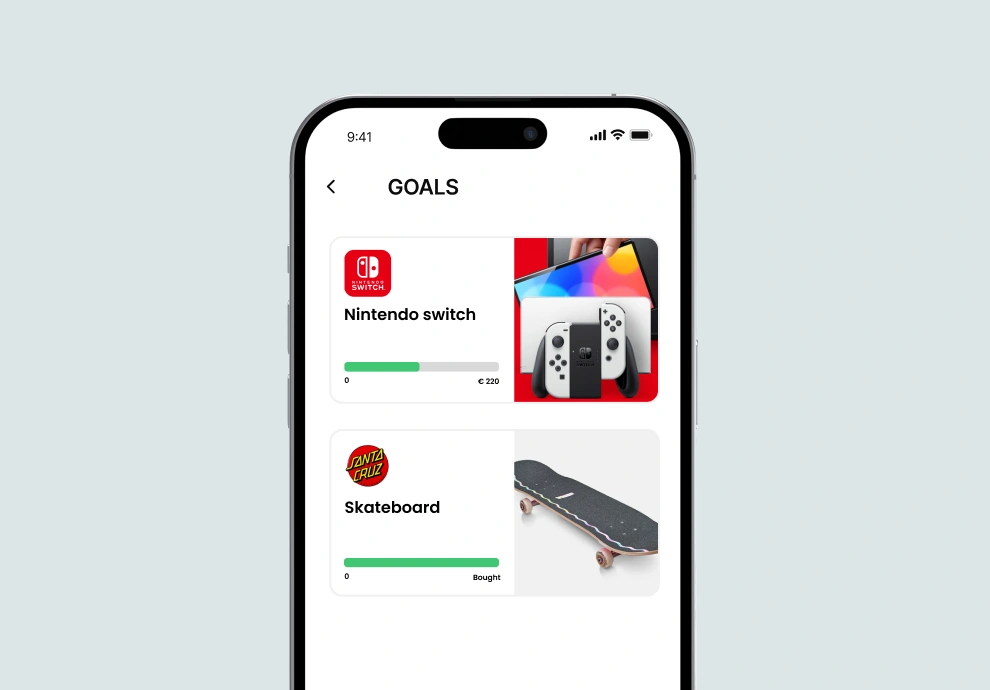

Some of the goals you can set for children might include saving up for a new bike or gaming console, and improving the child's saving habits. Or they can set aside a portion of their allowance for regular investments. GoHenry's fintech allows parents to set up a reward in the learn section that children receive for completing learning courses.

This gives you a win-win situation where you are giving your children pocket money for acquiring knowledge that will be useful in the future. We have nicely described the effects of gamification in the article: How gamification increases user engagement in banking apps?

Outlook for the future

Kids' banking is more than just a trend. It is a cornerstone for building a financially literate society. Generation Alpha no longer wants to receive their pocket money in cash, they want it on a smart payment card that is accepted by their favourite merchants. After all, cash can't buy a game on Steam. With the increasing integration of financial technology into everyday life, it is expected that children who grow up with access to these tools will be better prepared for the financial challenges of adulthood.

"Never before have we had such immediate access to our money and financial information, giving people great power to engage with their money and make more informed decisions. It is important that young people learn good money habits for the digital age early on."

Andy Bickers, savings director at Lloyds Bank for TheTimes.co.uk

Again, according to Visa's research, balancing control and independencies important.

Parents want to create a "safe space" where their children can manage their money safely. This level of supervision reduces over time and control is eventually handed over to the child completely:

- Between the ages of 8 and 11, 80% of parents want to know what their children are spending their money on.

- By the age of 11-14, this drops to 66% of parents

- By the age 15, parents no longer see this as a priority and usually want to step back and encourage positive behaviour rather than control spending

Conclusion

Kids banking opens new horizons in children's financial education, adapting to the digital age with tools that are close to their hearts. This approach lays the foundations for financial literacy from an early age. With the shift from cash to digital transactions,Kids banking reflects current trends and prepares children for the financial challenges of the future.

The role of parents and educators in this process is essential. By encouraging financial education and responsibility from a young age, parents can create a safe space for children's financial experimentation, gradually handing them more control and independence. As Andy Bickers of Lloyds Bank points out, never before has there been such instant access to financial information, giving us a huge power and responsibility to teach younger generations to manage their money properly.