Short answer: accurate transaction data. Long answer: accurate transaction data plus the ability to treat different payment behaviours as different problems. That is the core of any true detection solution when it comes to subscriptions.

Most banking apps still process transactions as one big, flat stream. But in real life, customers experience spending in three distinct ways:

Offline transactions are mostly in-person card payments. They’re anchored to physical context: location, POS patterns, and often clearer merchant identity. Customers usually recognise them instantly because they remember being there.

Online transactions are e-commerce, in-app purchases, wallets, and stored credentials. The context is weaker. Merchant naming can be inconsistent, and customers are more likely to ask “what is this?” because there’s no physical memory attached.

Subscription and recurring transactions are different species entirely. They are defined by repeat behaviour over time, not by where they happened. They have lifecycles (start, renew, upgrade, pause, cancel), they can change amounts, and they are the most likely to trigger churn if the bank can’t make them understandable.

And they are not a niche edge case: between 15% and 50% of all card transactions are recurring in nature, depending on the market and customer segment. Yet the majority of them are fragmented across thousands of merchants, and many are not flagged as recurring by payment schemes at all.

That’s why subscription management cannot be solved with the same logic as offline and online spending. Recurring payments are not a payment type. They’re patterns you discover through data enrichment and multi-level categorisation.

Tapix processes over 2 billion enriched transactions per month across 96+ active markets, with a data accuracy rate of 99.99%. That scale is what makes reliable pattern detection possible - rare or regional merchants can only be identified when the model has seen enough of them.

Want to know more?

Learn about unique data points and APIs behind bank transactions.

A subscription engine needs to recognise recurring payments through a mix of signals:

- Repeat frequency (monthly, weekly, annual)

- Stable or semi-stable amounts (including acceptable variance for usage-based billing)

- Merchant identity even when names are inconsistent (normalisation across descriptors)

- Flexible billing windows (real subscriptions drift, they don’t behave like a metronome)

- Lifecycle clues: first seen (start), last seen (possibly inactive), price changes, failed payments, and renewal gaps

How to Build Subscription Management | Webinar | 18/6 11 CET | Get your seat

Why this matters in 2026 and further

Banking is turning into an interface business. People don’t want more banking products, they want clearer understanding of their money, fewer surprises, and fewer manual tasks. Subscription behavior is exactly where those expectations connect with reality.

There is also a regulatory deadline accelerating this: Visa requires issuers in certain European markets to support subscription management functions - including identification of recurring, instalment, and unscheduled credential-on-file transactions - effective 18 April 2026. Banks that have not yet built detection infrastructure are already running late.

Recurring payments are predictable by nature. That means they’re perfect for building proactive experiences. But only if the bank can recognise them across messy data, multiple payment rails, and changing merchant behavior.

Banks that get this right win in the places that matter:

- Retention improves because customers anchor their financial routine to the app.

- Engagement improves because the app becomes a regular check-in.

- Revenue improves because recurring payments keep flowing through the bank’s rails.

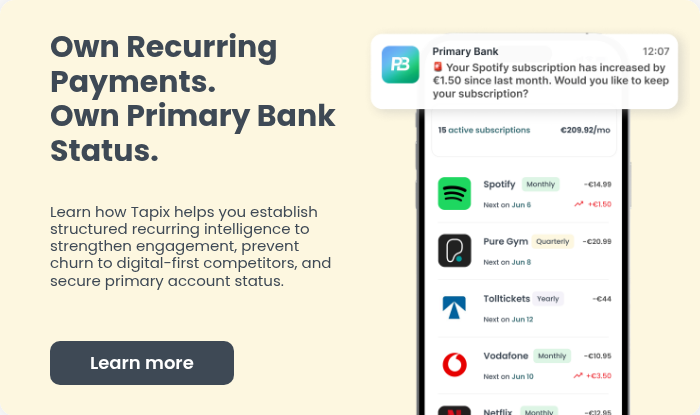

Tapix recurring payments intelligence is designed to detect and label recurring payments across real-world transaction data, including recurring card payments, subscriptions, and direct debits, then turn them into structured objects a bank can build features on top of.

That structure becomes the foundation for:

- subscription visibility customers trust

- cleaner personal finance experiences

- proactive alerts and insights

- smarter retention and lifecycle messaging

- stronger product and tier strategy

Because the bank that helps customers manage their recurring life becomes the bank they stop wanting to leave.

For more details on how enrichment solutions can benefit your bank, explore the Tapix offerings and our Recurring payments intelligence.