Transaction UX used to be a product decision. Some banks invested in recognisable merchant names and clean feeds. Others shipped raw descriptor strings and MCC codes. Today, Visa and Mastercard are increasingly turning transaction clarity into issuer requirements, and the minimum bar is rising for everyone.

This article covers all Visa/Mastercard transaction data requirements from issuers and how they affect banking UX.

Why networks care about transaction clarity

Card networks care about transaction clarity for one reason: disputes.

They do this by setting standards for what a cardholder must be able to recognise and control, and by pushing issuers toward specific data points that make recognition and recurring management feasible at scale.

When a cardholder cannot recognise a transaction, the issuer absorbs support costs, disputes increase, and chargeback processes start. Therefore, penalties for unclear transactions usually land in operational places with escalations that issuers pay for. Visa and Mastercard have each responded with issuer programmes that push toward recognisable merchant identity and recurring payment transparency.

What Visa and Mastercard each require

The two networks share the same intent - recognisable merchant identity, reachable contact details, and workable controls - but arrived via different programmes and timelines.

Enhanced merchant identity

Both networks expect a cardholder to recognise who got paid and be able to reach them. In practice this means a recognisable DBA (doing business as) name, address, phone, and website.

Subscription and recurring controls

Recurring payments are where unclear information becomes measurable cost.

- Clear identification of recurring and subscription patterns

- Stop and cancel flows with clear guidance pathways

- Correct handling of decline codes specific to recurring scenarios

- Transparency that cancellation may be contractual with the merchant - not always resolvable inside the bank

Cardholder controls

Issuers are expected to support cardholder-driven controls and present them clearly as user actions - not issuer-imposed blocks:

- Freeze and unfreeze card usage

- ATM blocks, in-store and online restrictions (issuer-dependent feature set)

- Clear labelling so users understand these are their own controls, to reduce unnecessary support contacts

Neither network mandates UX patterns directly. They define the minimum information a cardholder must be able to recognise and act on.

Want to know more? Download our Compliance Guide for banks!

Where compliance meets UX reality

Take a simple scenario: a cardholder sees a charge they don’t recognise. They open their banking app. What they see next determines whether this becomes a support ticket, a dispute, or a resolved moment of clarity. This is where compliance requirements and UX reality diverge - and where banks either absorb cost or eliminate it.

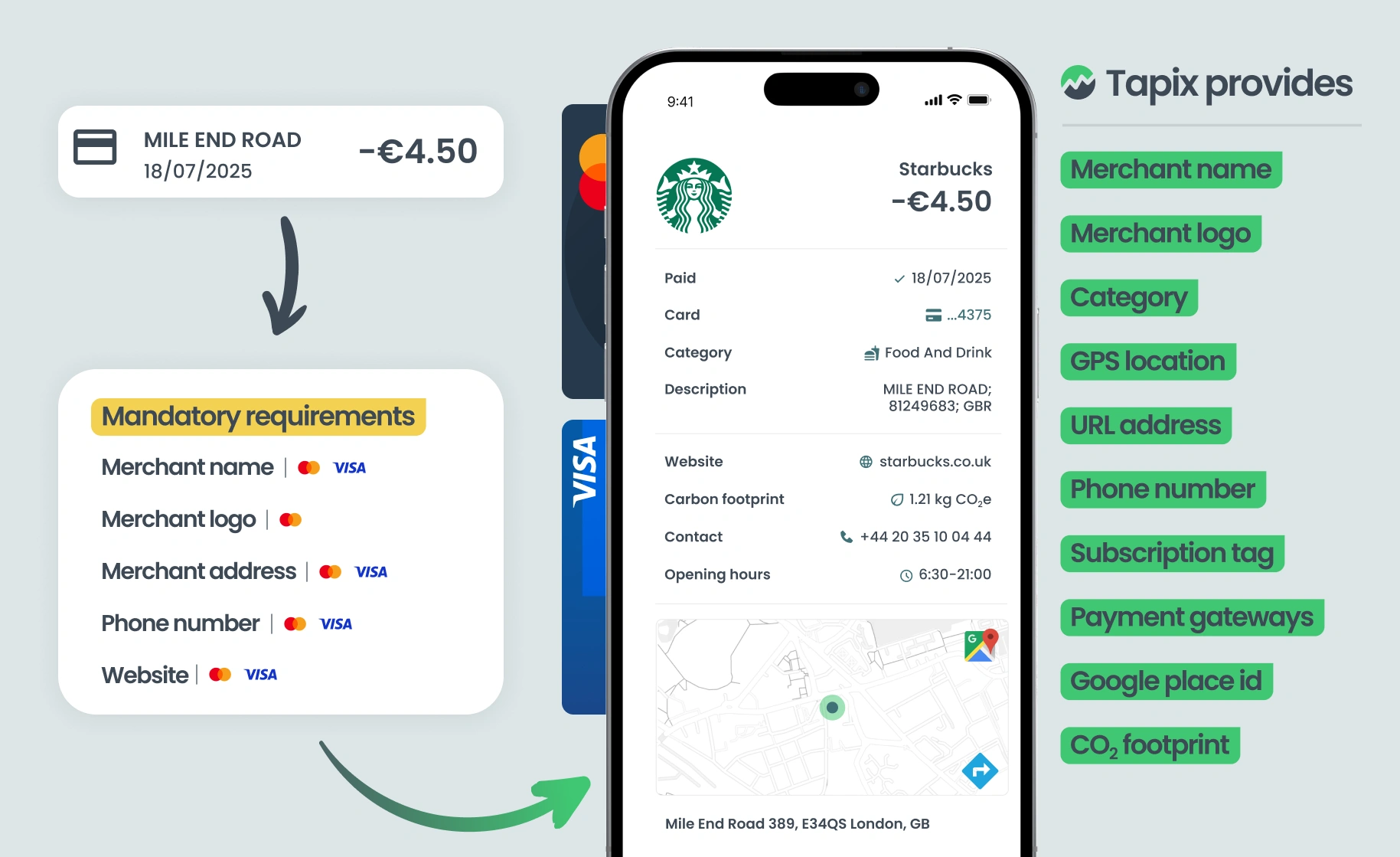

Showing the merchant's name

The common mistake is displaying the raw description or a legal-entity label. That can be technically “a name,” but it fails at helping a cardholder instantly recognise the brand they interacted with.

Best case scenario is to show brand or DBA (doing business as) name the customer knows and recognises. Keep the original description available in the details for operational purposes. Where possible, go deeper to the specific store or location (useful in shopping centers and chains).

Logos multiply awareness

Visa does not mandate merchant logos - but logos are one of the highest-leverage recognition tools in a transaction list. A cardholder will recognise a Netflix or Spotify logo instantly, even if the legal entity name means nothing to them. When a logo is missing, UX needs structured fallbacks: category icons, payment-type badges, or merchant initials.

Gateways create a recognition gap

The description often contains multiple identifiers: the payment gateway (PayPal, Stripe), the platform (Google), and the actual service/brand the user cares about (YouTube). The issue is that many banks apply cleaning rules that accidentally strip the meaningful brand and keep the gateway or do the opposite inconsistently.

Want to know more? Read How to detect gambling transactions in digital banking.

The biggest mistake usually lands in categorisation. If you treat PayPal as the merchant, you push the transaction into financial services, which destroys purchase intent. If you resolve it to YouTube, you can classify it as streaming / subscription, which matches what the user is actually paying for.

Best decision is to preserve both layers - still surface the real merchant as the primary identity with gateway context as supporting info. Use tags to further differentiate the categories.

MCC codes classify merchants, not purchases

Networks regulate identity fields. They don’t regulate categorisation quality. MCC codes tell you what type of merchant was paid - not what was actually bought. A payment at Amazon can be groceries, electronics, or a Prime subscription. Most modern banking apps layer proprietary categorisation on top precisely because scheme codes don’t carry purchase intent.

Keeping the data layer compliant over time

Compliance ensures the merchant is recognisable. Good UX ensures the transaction is understandable. The gap between those two outcomes is where most banks struggle - because networks can mandate identity fields, contact details, and recurring controls, but they do not maintain the data quality required to keep clarity intact month after month.

In practice, these are the areas that drift:

- Merchant data change frequently (~25% annually) - brand structures shift, contact endpoints update, store metadata drifts.

- Logo assets require lifecycle management as brands refresh and visual identities evolve (logos change ~8% yearly).

- Recurring classifications must stay stable as descriptors, amounts, and billing cadences change.

- Gateway mappings need consistency, or recognition defaults back to generic labels.

This is why compliance should be treated as the floor, not the ceiling. Visa sets the minimum merchant data layer. Mastercard raised the baseline earlier. Banks that build the infrastructure properly can use the same maintained data layer to do more than pass mandates. They can:

- reduce disputes

- improve push notifications

- power subscription management

- enable smart search

- build CO2 insights

If you are already investing to meet Visa and Mastercard expectations, you need a dedicated data layer that continuously keeps merchant identity accurate, keeps recurring logic stable, and prevents mistakes before they show up in the app.

With Tapix, this work is not focused solely on Visa/Mastercard. It is our core job: keeping your transaction data compliant as requirements evolve, keeping it up to date in production, and giving you a structured foundation you can build on immediately. The same maintained enrichment layer that satisfies network baselines also unlocks higher-value UX outcomes. We map these capabilities and the way to implement the features in our Data in Action catalogue.