On paper, building your own data enrichment solutions sounds smart. You’ve got capable engineers, a decent data science team, and a roadmap that seems to allow for it. But here's the thing: enriching transaction data isn’t just a technical project, it’s a constantly evolving project. And for many banks and fintechs, what starts as a quick fix turns into a long-term liability.

So, let’s dig deep - the unexpected costs, time traps, and edge-case chaos that tend to blindside teams chasing in-house data enrichment solutions. And of course, the reason we think Tapix solution might be a great pick for you.

Transaction Enrichment is Not a Simple Categorisation Task

Transaction enrichment might look like a simple matter of mapping merchant names and applying rules to identify categories. But real-world data rarely behaves so predictably. With chaotic merchant descriptions like “F.LLI MARINO SNC” or “B2B PRIME” in the “Other” category, it’s nearly impossible to accurately determine what the customer purchased without contextual intelligence. Customers expect clarity, and when their banking apps display cryptic or misleading information, trust goes away quickly.

That’s where dedicated APIs come into play. If you’ve asked, “How can I implement payment categorisation in my banking software?” - the answer usually involves tapping into a transaction data enrichment API designed to handle messy real-world inputs at scale.

In practice, building an enrichment platform that adapts to ever-changing merchant behaviors, regional nuances, and inconsistent formatting is not a one-time project. It’s a continuous investment in data science, machine learning, feedback loops, and global coverage.

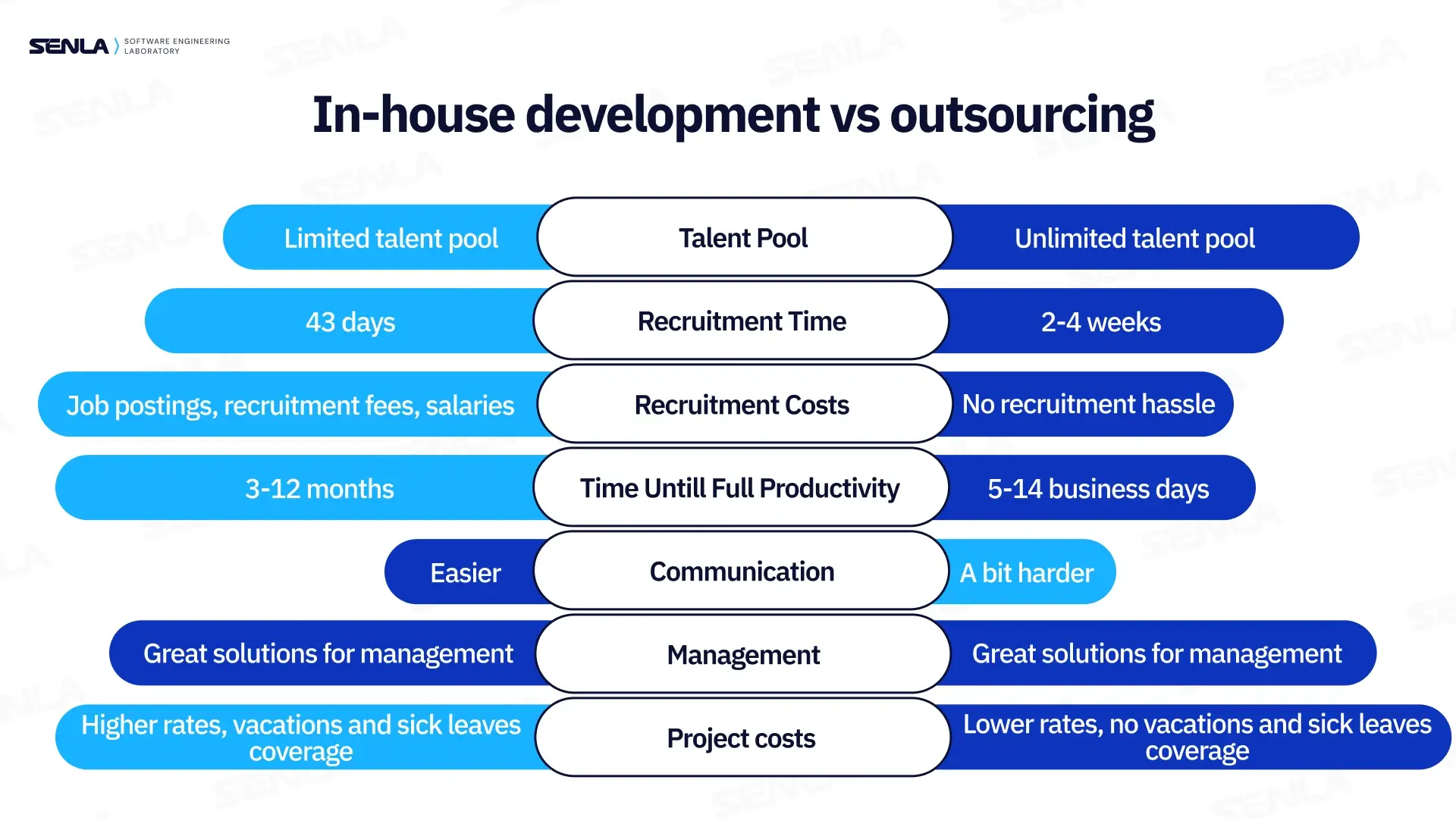

Talent Is Not the Constraint. Focus Is

Most fintech teams are capable of hiring talented engineers and data scientists. The challenge isn’t availability. It’s prioritisation.

Once the initial enrichment framework is built, the real work begins: refining models, incorporating user feedback, monitoring classification accuracy, handling edge cases, and updating logic as new merchants and payment patterns emerge.

This is why many growing institutions begin to ask: What are the benefits of using a payment data enrichment API? The short answer? Faster time to value, better accuracy, and zero distraction from your core product goals.

Hidden Operational and Compliance Burdens

The long-term costs of an internal enrichment platform often go beyond headcount. Maintaining and improving such a system introduces several additional layers of responsibility:

- Data infrastructure: Managing real-time ingestion, cleaning, and secure storage

- QA and accuracy monitoring: Ensuring classification reliability at scale

- Ongoing updates: Keeping pace with global merchant changes and consumer behavior

- Regulatory compliance: Especially important when models are trained on sensitive data

- Security: Protecting enriched data against breaches or misuse

Additionally, implementing enrichment that functions across languages, currencies, and regional merchant structures adds considerable complexity - particularly for institutions operating in multiple markets.

The Total Cost of Enrichment Solutions Ownership

The real cost of building and maintaining an in-house enrichment solution is often underestimated. While initial projections might account for engineering salaries and server costs, the hidden and recurring expenses soon start to surface:

Constant model retraining and manual corrections: Even the most advanced machine learning models degrade over time as new merchant formats, payment flows, and spending patterns emerge. Teams end up dedicating entire sprints to refining merchant databases and debugging incorrect labels.

Cross-departmental coordination: Product teams demand rapid iteration, compliance teams need to verify categorisation logic, and engineering must balance accuracy improvements against roadmap priorities. The overhead of aligning these functions grows month by month.

Customer-facing issues: Mislabelled transactions frustrate users, leading to higher volumes of support tickets, refunds, or even churn. Each error requires manual review, internal escalation, and patching - diverting attention from other projects within the company.

Accuracy audits and testing pipelines: Internal QA teams are often forced to run extensive checks to avoid performance drops. Maintaining a 90%+ accuracy requires continuous data pipeline tuning and merchant-level validation.

Regulatory and legal oversight: Data enrichment solutions touch sensitive data. Any missteps - such as incorrect merchant names or miscategorised gambling transactions - can lead to regulatory headaches, fines, or customer mistrust.

In contrast, third-party solutions like Tapix offer accuracy rates exceeding 95%, thanks to billions of processed transactions and proprietary enrichment models built from years of domain expertise. Tapix maintains a merchant database covering hundreds of thousands of brands worldwide, complete with logo recognition and metadata standardisation, all updated in real time.

For example, Deblock, a crypto banking app, integrated Tapix to improve clarity around complex blockchain-related transactions and saw merchant coverage increase 25% and logo coverage reach 66%. Similarly, bunq, one of Europe’s leading neobanks, used Tapix to deliver intelligent insights to its users across personal and business accounts. The result? More than 90% transactions categorised and 99,9% data accuracy achieved.

E-commerce Transactions Pose an Additional Challenge

Accurately identifying e-commerce transactions remains one of the most persistent and frustrating pain points in data enrichment. For banks and fintechs serving consumers and SMBs, the challenge is simple to describe but hard to solve: payment processors like Stripe, PayPal, Adyen, and others often mask the true identity of the merchant.

This becomes especially problematic when building budgeting tools, small business analytics, or customer support systems that rely on clear merchant identification. A user seeing “STRIPE.SNL” won’t know whether they bought shoes or booked a service.

Tapix addresses this issue directly through a specialised Payment Gateways enrichment module. By resolving transaction patterns from all major gateways - including Stripe, PayPal, Adyen, Square, and Braintree - Tapix can accurately reconstruct the original merchant name, assign it the correct category, and attach consistent visual metadata like logos and location.

Rather than relying on raw transaction descriptors, Tapix leverages:

- Internal merchant graphs connecting gateway aliases with verified brand names

- Dynamic metadata lookups that interpret structured but ambiguous gateway data

- Real-time updates to reflect emerging e-commerce brands or reseller platforms

- Contextual enrichment tailored to consumer and SMB use cases

Building something similar in-house would require access to vast merchant network data, consistent feedback loops, and direct partnerships with processors - none of which are trivial to establish. Tapix solves this at scale, enabling institutions to offer cleaner transaction data without compromising their own resources.

Final Thoughts

Building your own enrichment framework may seem like a smart, strategic move, but for most banks and fintechs, it ends up being a costly diversion from core priorities.

Hiring brilliant people who understand your data is absolutely essential. But they shouldn't be the ones reinventing enrichment pipelines from scratch. Their time is better spent interpreting the data - turning insights into action, and strategy into growth. The data itself? That’s what we’re here for.

For more details on how enrichment solutions can benefit your bank, explore the Tapix offerings.