SME clients have higher expectations than retail clients, and for good reason. Banking is not a background activity for them - it is part of their daily operations, reporting cycles, and financial planning. SME transaction categorisation is not a visual convenience. It directly influences cost control, tax handling, internal reporting, and how accurately a business understands its own financial position.

The problem is that most banks still serve SME clients with logic built for retail. This is one of the clearest gaps in SME banking today, and closing it represents a significant opportunity for banks looking to deepen relationships with business clients. Let us tell you how.

What makes SME banking different

In consumer banking, categorisation helps individuals understand where their money goes. The categories are intuitive, the stakes are relatively low, and the occasional mistake is a minor inconvenience. In SME banking, the same mistake can mean a cost booked to the wrong department, a tax deduction misapplied, or a cashflow report that management cannot trust. The consequences are operational. This is exactly where SME transaction categorisation differs fundamentally from retail approaches.

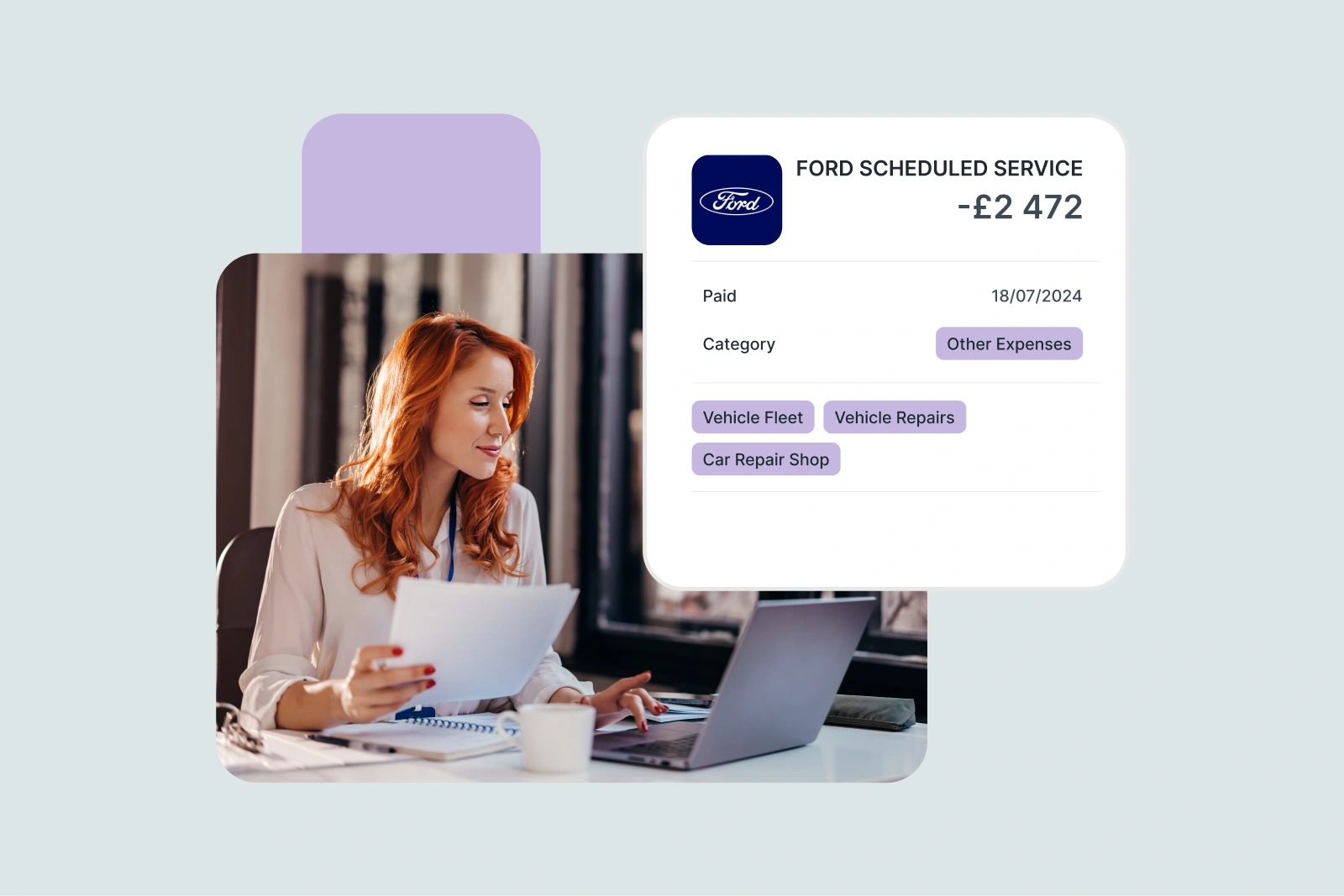

The key challenge is that the usefulness of categories is specific to each company. The best example is the distinction between production costs and operating costs. This depends entirely on what the company produces. Fuel may be:

- A production cost for a logistics company

- An operating expense for a consulting firm

- A project cost for a construction company

MCC codes were never designed to carry this kind of nuance. With roughly 600 to 800 codes in circulation globally, they provide a rough taxonomy at best. Most modern SMEs have internal cost structures far more granular than MCC allows - multiple departments, project codes, cost centres, and reporting categories that reflect the actual shape of the business.

This is why SMEs already process many transactions manually. They have no choice. The goal of a well-designed banking product is not to replace that intelligence with generic labels. It is to capture it once and automate it going forward.

The Foundation: High-quality categorisation and merchant recognition

Before any meaningful logic SME transaction categorisation can be built, the underlying transaction data needs to be clean. This sounds obvious, but in practice it is frequently overlooked.

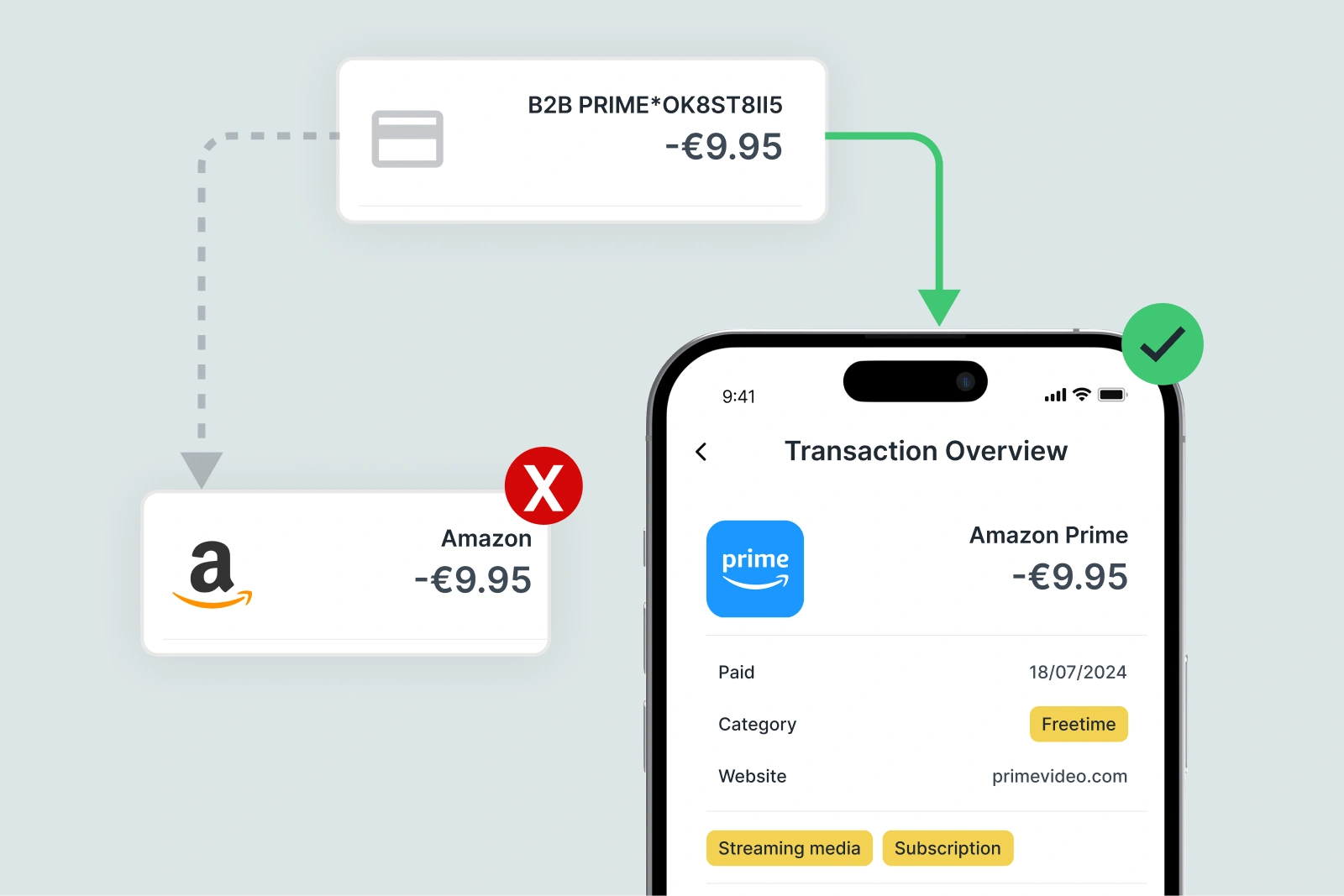

Raw bank feeds are messy. Merchant descriptions arrive as chaotic strings, payment gateway references, or internal billing codes that bear little resemblance to the actual vendor. A business owner reviewing transactions should see "Amazon Web Services," not "AMZN MKTP US*AB3K2."

Without accurate, standardised merchant recognition, categorisation becomes unreliable regardless of how sophisticated the rule of logic is. Garbage in, garbage out applies here as much as anywhere in data infrastructure.

Good merchant enrichment resolves raw transactions into clean, recognisable entity names, and maps them into structured categories that go beyond basic MCC. This is the baseline. It reduces the volume of transactions that fall into an unhelpful "Other" bucket, increases confidence in dashboards and reports, and creates the consistent data structure that rule-based automation depends on.

What are MCC Codes and Why Banks Need More for Reliable Payment Categorisation?

What SME Transaction Categorisation Requires: Manual re-categorisation and rule learning

SME transaction categorisation must allow manual correction, simple as that. Companies need to reassign transactions because they understand their own business logic. This is not a weakness of the system. It is a requirement.

The critical design principle is that manual corrections should become rules. When a finance manager reclassifies a transaction, the system should offer to apply that logic consistently going forward. That is where the real efficiency gain lives - not in any individual correction, but in the automation it unlocks downstream.

To be genuinely useful, rule configuration should operate at multiple levels of granularity:

- Merchant level - all transactions from a given supplier mapped to a specific category

- Card or user level - categorisation rules tied to how a particular employee or card is used

- Department or cost centre level - transactions routed based on organisational structure

- Combination rules - for example, fuel purchases from Card X assigned to Production Cost and allocated to Cost Centre Z

This reflects real operational logic. Once rules are applied consistently, categorisation becomes infrastructure where transactions are mapped directly into business semantics.

Tapix supports this architecture by combining:

- High-quality merchant enrichment

- Bank-configurable category structures

- Client-level rule capabilities

- APIs that integrate into SME banking platforms

This enables banks to offer flexible categorisation without rebuilding backend systems for each client.

What this architecture enables for SME banks

Research consistently shows that SMEs prioritise banking providers that reduce administrative workload and improve financial visibility. When categories work, dashboards become actionable. Forecasting is becoming more reliable. Expense allocation becomes structured.

SME transaction categorisation affects:

- Cost centre visibility

- Human resources economisation

- Cashflow control

- Financial reporting accuracy

- Internal efficiency

- Trust in SME digital banking tools

For banks, the strategic implication is clear. Generic categorisation keeps SMEs at arm's length from their banking platform. Configurable, client-specific categorisation makes the bank part of the operational workflow. That distinction drives product stickiness, reduces churn, and creates the kind of day-to-day relevance that leads to deeper product relationships over time.

One practical concern for banks is the cost and complexity of delivering flexible categorisation at a scale. Building bespoke category logic for every SME client is not a realistic product strategy, which is why scalable SME banking software must rely on configurable architectures rather than custom builds. The viable path is a layered approach: a high-quality enrichment and categorisation layer that handles the baseline data quality problem, combined with a configurable rule engine that allows client-level customisation without manual intervention from the bank's side.

Tapix is built around exactly this model as a flexible SME banking solution. It provides banks with high-quality merchant enrichment and standardised SME transaction categorisation as a foundation, alongside a configurable category structure and client-level rule capabilities exposed through APIs. This shift reflects the broader future of SME banking, where banks move from service providers to operational infrastructure.

For more details on how enrichment solutions can benefit your bank, explore the Tapix offerings.