When you’re looking for transaction data enrichment tools and their features, six vendors usually come up: Tapix, Tink, Ethoca, Salt Edge, Fiserv, and Plaid. Most comparison posts treat them as interchangeable API swaps. They are not. They sit at different layers of the stack, they solve different problems, and picking the wrong one means paying for capabilities you do not need while missing the ones you do.

This article walks through what each tool actually does, what it does not, and how to match them to the problem you are trying to solve.

Transaction data enrichment tools at the core

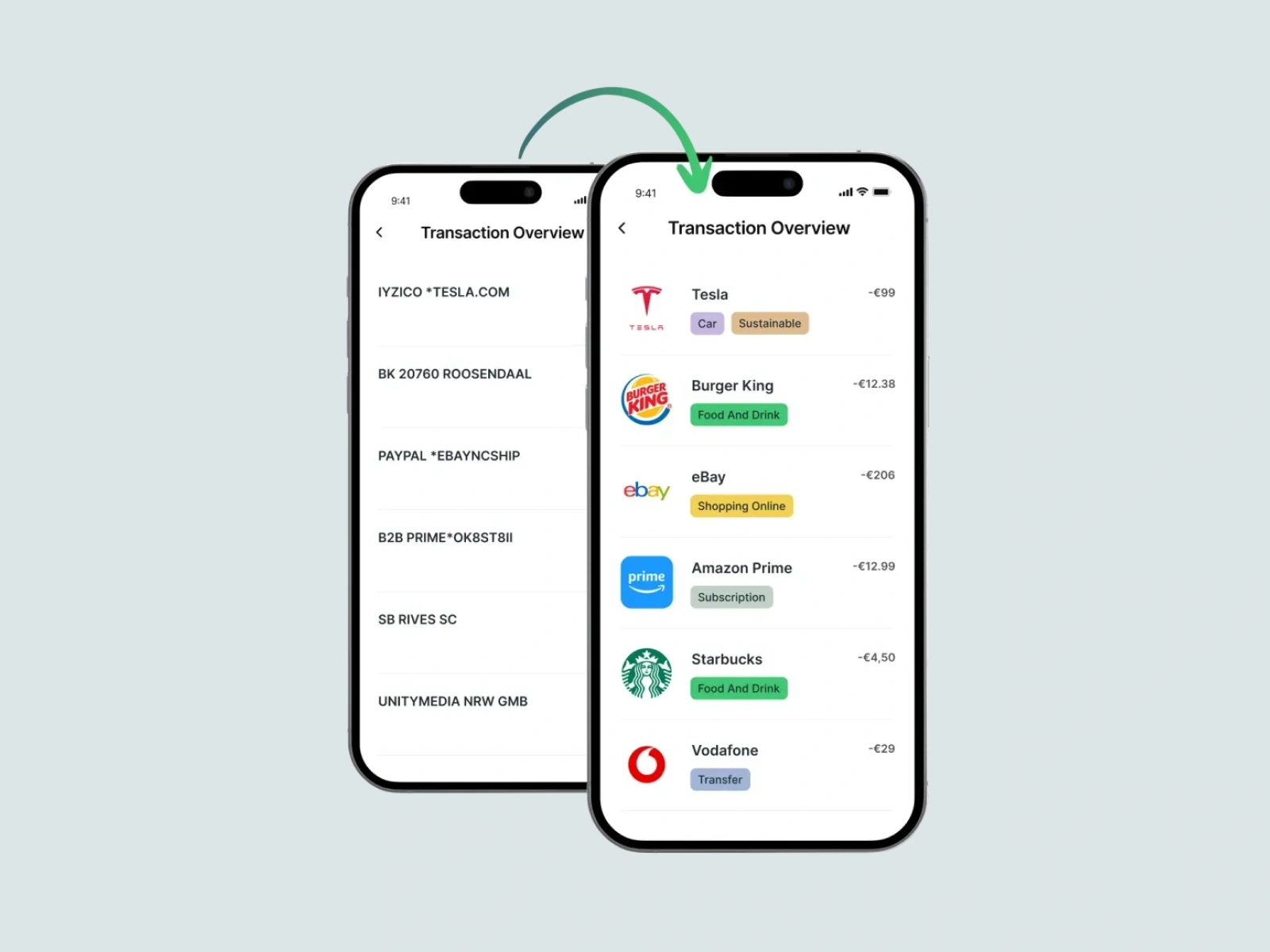

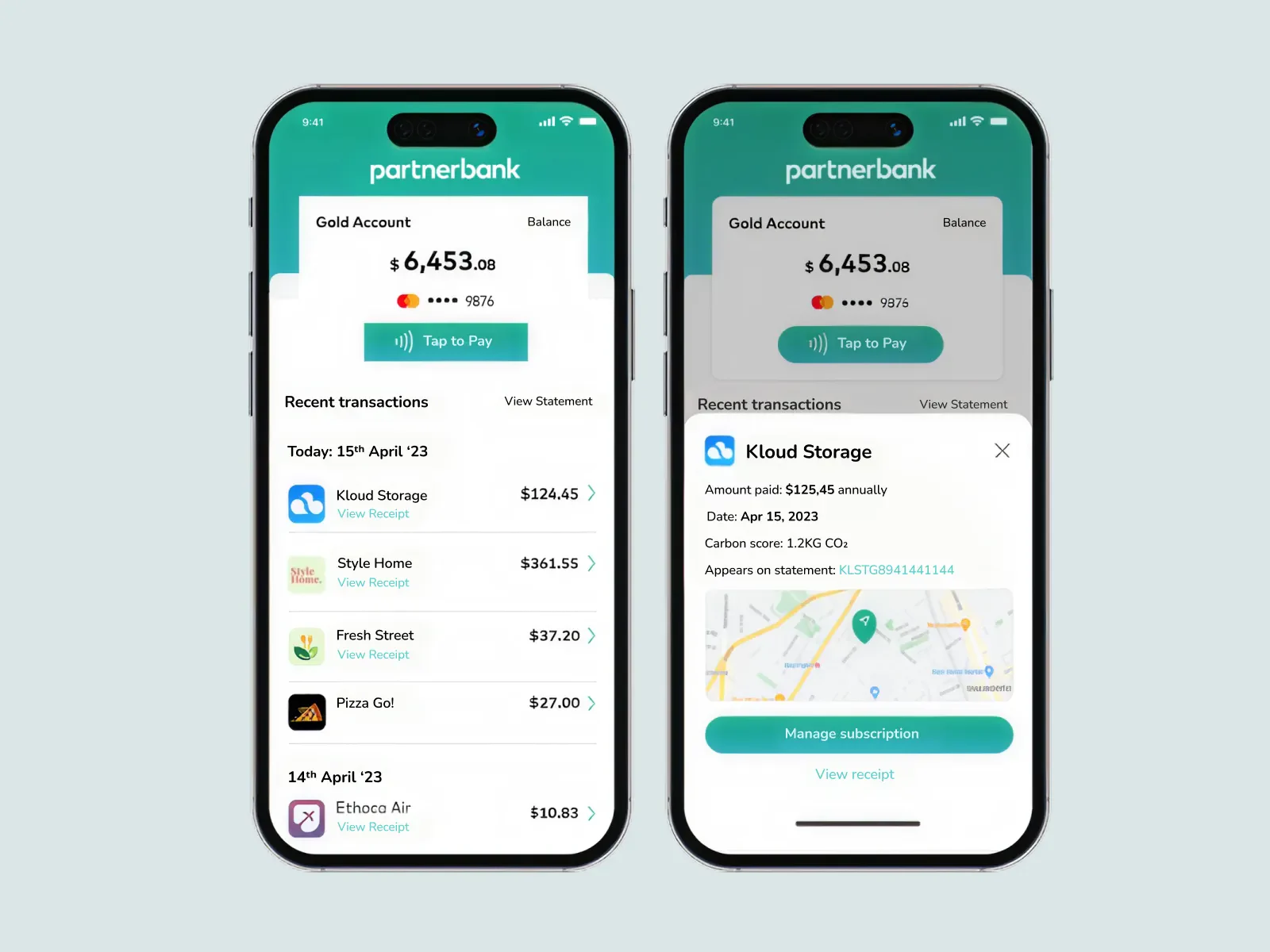

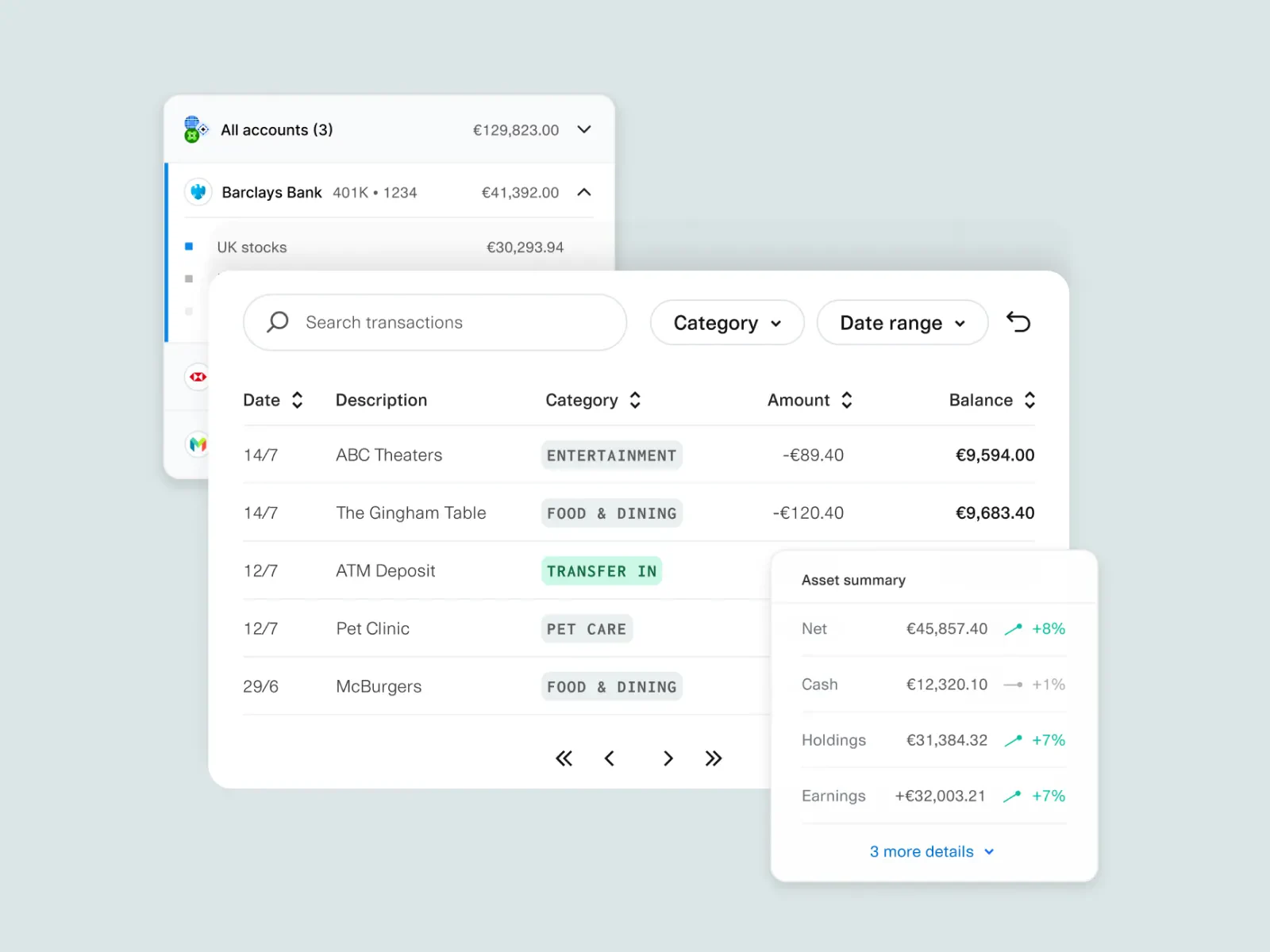

Transaction data enrichment turns the raw, cryptic strings that arrive with card transactions, and bank transfers into something a customer can recognise. A line that reads “SQ *SB 4378262 FRA US” becomes "Starbucks", with a logo, a category (Food & Drink → Café), and a location.

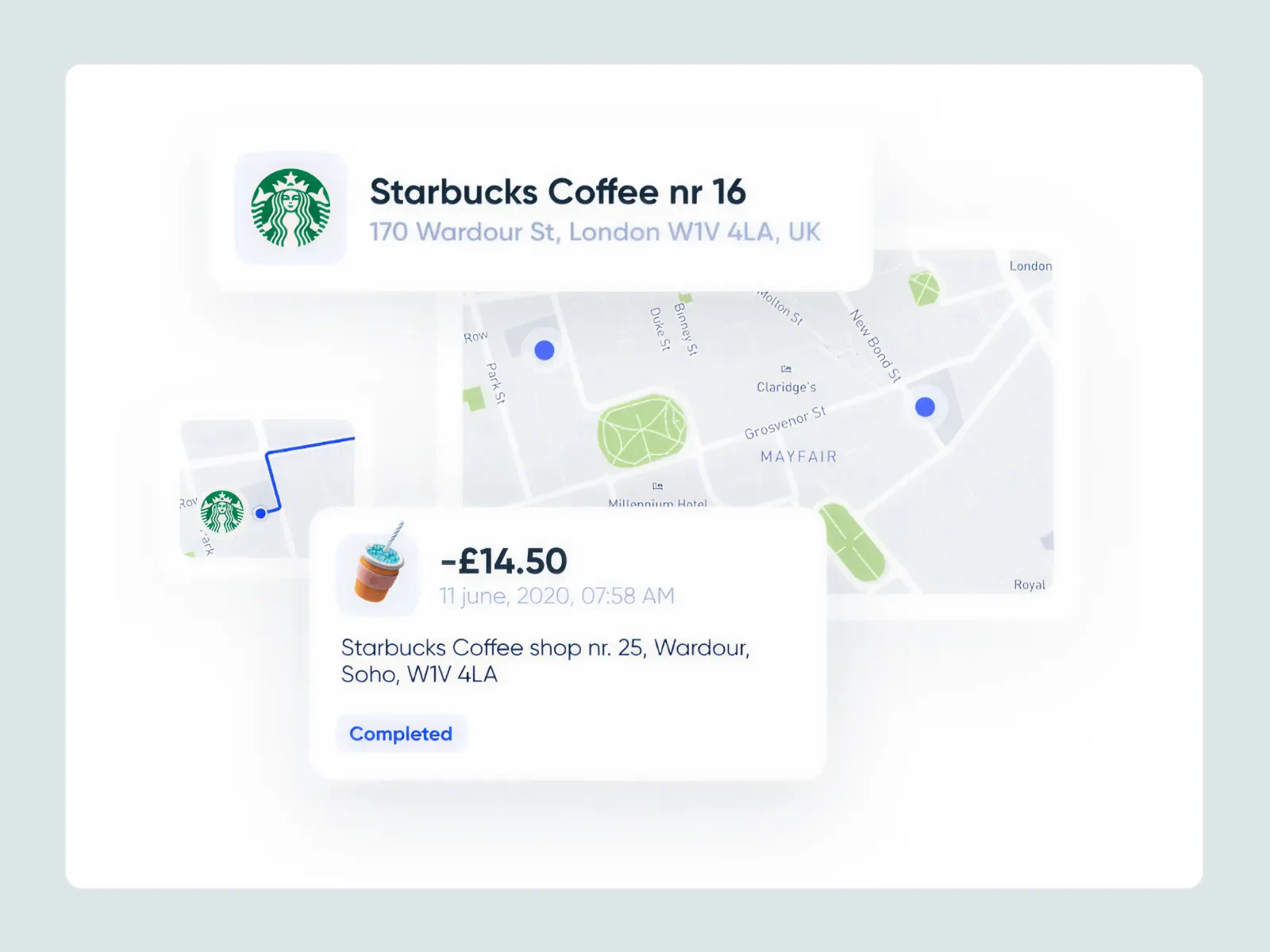

The data points produced typically include merchant name, merchant logo, category, location (GPS, address, store-level), website, payment channel (in-store, online, subscription), and sometimes contextual signals like CO2 estimates or recurring-payment patterns.

For more information on what is vital for a perfect PoC, read this article.

Enrichment matters because raw payment data is unusable for almost every modern banking feature. PFM, fraud detection, dispute prevention, credit decisioning, sustainability dashboards, loyalty offers, push notifications - they all assume the transaction feed is clean. When it is not, every product on top of it inherits the chaos.

Five archetypes to choose from

The six vendors covered here all sit somewhere in the transaction data enrichment market, but they belong to four distinct architectural archetypes. Understanding which archetype a vendor belongs to matters more than any individual feature comparison.

Specialist API enrichment is a standalone enrichment-only product. Tapix sits in this category. The vendor does not aggregate accounts, does not run a card network, and does not sell core banking. It enriches transaction data, full stop.

Network-level enrichment sits on a card network's rails. Mastercard's Ethoca is the clearest example: it shares structured purchase data between merchants and issuers via Mastercard infrastructure, primarily to prevent disputes. It is not an API you point at your transaction feed.

Aggregation-bundled enrichment comes packaged with bank account aggregation. Tink, Plaid, and Salt Edge all started as open banking aggregators and added enrichment as a layer on top. If you are also pulling account balances and transactions through the same vendor, this bundle is efficient.

Core-banking-bundled enrichment is built into a core banking platform. Fiserv's Integrated Transaction Enrichment is the example here - it lives inside Fiserv's authorisation stream and integrates natively with Fiserv-issued cards and core systems.

These archetypes are not better or worse than one another in the abstract. They serve different buyers with different problems. The next sections cover each vendor in detail.

Tapix

Tapix is the specialist option in this comparison. Instead of focusing on aggregating accounts or running a card network, it enriches transaction data for banks and fintechs across 112+ markets with superior accuracy.

Vendor highlights include 99.99% data accuracy, 800,000+ unique merchants in the database, 1.5 billion+ monthly transactions processed, 70+ active clients including bunq, Société Générale, UniCredit, Erste, and Raiffeisen Bank, an average API response time of 3ms, and 11+ years building enrichment as a single focused product.

Main solutions include:

Multi-layer categorisation beyond MCC. MCC codes are a flat list of roughly 600 categories, designed for card scheme reporting rather than consumer-facing UX. Tapix uses a four-level hierarchy that breaks "Transportation Services" into taxis, public transport, bike sharing, and electric scooters. This depth is what makes a real budgeting feature different.

Subscription identification with pattern insights. Most enrichment vendors flag whether a transaction is recurring. Tapix returns the frequency, the next billing date, and the amount pattern - the data structure needed to build a working subscription manager.

Native sustainability data with Eco Track. CO2 estimates per transaction, calibrated at the merchant level rather than averaged from MCC categories.

ATM-enriched data. ATM network recognition, fee detection, and location. None of the other five vendors in this comparison offer this as a named capability.

All payment types, including local schemes. Card transactions, bank transfers, open banking data, QR payments, and local payment standards including iDeal (Netherlands), Blik (Poland), and Wero (pan-European). Most enrichment products are card-first; transfers and local schemes are gaps Tapix can close.

Hyper-personalisation layer. Enriched data structured for behavioural analytics. This is what enables cross-sell scoring, churn prediction, and segmentation use cases on the same data foundation that powers the app UI.

For more on how this looks in practice, see How leading banks use transaction enrichment.

Tink

Tink is a European open banking platform acquired by Visa in 2022. It connects to thousands of European banks and offers data enrichment as a layer on top of its account aggregation infrastructure.

Tink processes over 6,000 connections to European banks and institutions, and offers enriched and categorised financial data through one API, with over 2 billion transactions per month across all products. The enrichment product covers categorisation via machine learning, recurring transaction detection, and merchant data.

Tink fits well when the buyer also needs PSD2 account aggregation under the same vendor. The bundle makes sense for European fintechs and challenger banks building PFM features on multi-bank data. Tink's enrichment is solid on the basics and benefits from Visa's enterprise reach.

Where Tink is lighter: merchant data depth. Logos and branding are available, but granular store-level data (exact GPS to shop, Google Place ID, payment gateway resolution for online purchases) is less developed than dedicated enrichment specialists. Sustainability data comes via partners rather than as a native data point.

Ethoca (Mastercard Consumer Clarity)

Ethoca is the outlier in this comparison. It is not an API enrichment vendor in the same category as the others - it is a merchant-issuer data-sharing rail operated on Mastercard's network.

Ethoca's Consumer Clarity provides enriched transaction information from 145+ million merchant locations spanning 200+ countries, leveraging the scale of Mastercard's global payment network. The data delivered to issuers includes clear merchant names, logos, geolocation data, fully itemised receipts and even smart subscriptions functionality, shared via issuers' digital banking apps and back-office systems.

The use case is dispute prevention. When a cardholder sees a transaction they do not recognise, their first instinct is often to dispute the charge. Consumer Clarity surfaces enough context that the cardholder remembers the purchase before initiating a chargeback. Unlike chargeback alerts or representment, Consumer Clarity intervenes before a dispute ever begins.

Where Ethoca is lighter: First, Ethoca depends on merchant participation in the Mastercard programme - coverage is wide but not universal, and merchants outside the network are not enriched. Second, it does not categorise transactions, does not enrich bank transfers, and does not produce structured data your engineers can build PFM, sustainability, or analytics features on.

Learn more about Visa Mandate requirements in our special look.

Salt Edge

Salt Edge offers a data enrichment Platform alongside its open banking gateway. The two products can be used together or independently.

Salt Edge's enrichment platform covers a categorisation API that assigns categories to unclear business and personal transactions, a merchant identification API that returns detailed merchant information including location, contact details, and social media, and financial insights based on bank data. The merchant database is large - based on an extensive list of more than 25 million of the most popular merchants from all over the world.

Salt Edge fits best when the buyer needs a single vendor for both account aggregation across European and APAC markets and basic enrichment under one licence. The compliance posture is solid (ISO 27001, PSD2-licensed AISP), and the API supports both personal and business categorisation taxonomies.

Where Salt Edge is lighter: the categorisation API accepts batches of at most 100 objects per request, which can be a constraint at high volume without careful batching architecture. Categorisation depth is lighter than dedicated enrichment-first players, and merchant-level granularity is less developed than vendors that focus exclusively on enrichment.

Fiserv

Fiserv approaches enrichment differently from the other vendors here. Rather than offering a standalone API a bank can point at any transaction feed, Fiserv enriches data inside its own authorisation stream.

The mechanism is simple: machine learning classification models classify transaction types and merchant categories based on the wealth of data fields available from the real-time authorization stream - POS entry mode, condition code, terminal type and merchant category code. Enrichment covers merchant names and categories, store locations, payment channels, payment methods, digital wallet type, card on file, recurring payments and many other attributes.

Fiserv fits banks already running on the Fiserv core that want enriched transaction data without procuring a separate vendor. The integration overhead is minimal because the data is already inside the Fiserv estate.

Where Fiserv is lighter: Fiserv's enrichment is not designed to be plugged into a bank running on a different core, and European or APAC coverage is thin. For banks not on Fiserv infrastructure, the practical answer is usually a different vendor.

Plaid Enrich

Plaid is the dominant transaction data infrastructure in the US, and Enrich is its standalone enrichment product.

Enrich is powered by machine learning that enriches 500 million transactions daily, with enhancements covering standardised merchant names, helpful details such as location and website, accurate categorisation, and counterparty identification including marketplaces like Doordash and payment terminals like Square. Plaid's overall Transactions product reports over 90% categorisation accuracy.

Plaid Enrich fits US-primary fintechs and banks, particularly those already using Plaid for account aggregation. The developer experience is mature, the API is well-documented, and the counterparty identification is genuinely useful.

Where Plaid is lighter: Plaid's enrichment depth and bank coverage drop noticeably outside the US. European local merchants, region-specific payment schemes, and non-English merchant strings are weaker than what European specialists offer. For a US-led fintech expanding into Europe, this often means pairing Plaid with a second vendor.

Side-by-side

How to choose the right one

Three questions you should be asking to narrow the field:

Do I also need bank account aggregation, or is my transaction feed already mine?

A bank issuing its own cards already owns the transaction feed and needs only enrichment - a specialist API like Tapix fits. A fintech building on multi-bank data needs aggregation plus enrichment, and a bundled vendor like Tink, Plaid, or Salt Edge becomes more efficient.

What problem am I solving with enrichment?

UX clarity (cleaner statement, recognisable merchant logos) is one thing. Analytics depth (segmentation, cross-sell, behavioural scoring) is another. Compliance and dispute reduction is a third. Each leads to a different vendor archetype: specialist API for analytics-grade data, network rails for dispute prevention, aggregation-bundled for PFM-on-multi-bank-data.

Which geographies and payment types matter most?

Card-only in the US: Plaid is the obvious answer. European retail banking with bank transfers and local schemes (iDeal, Blik, Wero): a specialist like Tapix or a European-strong aggregator. Multi-region banks needing depth in 100+ markets: very few vendors qualify, and the specialists pull ahead.

If enrichment is foundational infrastructure for your product, the specialist option is usually the right call. If it is one requirement among many, and the team prefers a single vendor for connectivity and enrichment, a bundled platform may be enough.

Learn what the cost of data inaccuracy is in digital banking.

The wrong choice usually shows up six months in, when push notifications still display raw terminal strings, "Other" remains the largest spending category, and the analytics team is rebuilding categorisation in-house. Most of those failures are not the vendor's fault. They are the result of treating enrichment as a downstream cleanup rather than a piece of transaction infrastructure that everything else depends on.