For banks - Subscription management

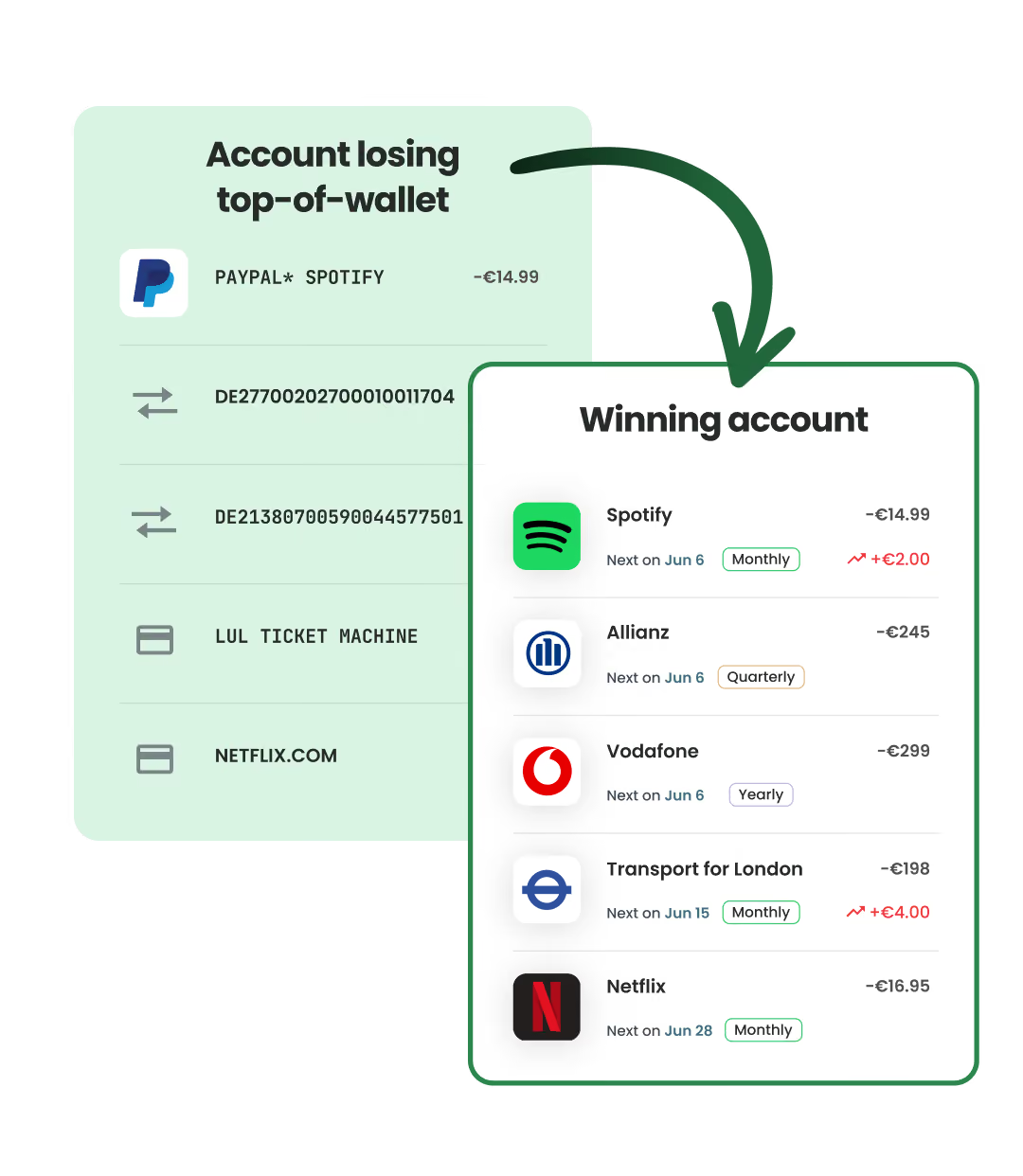

Primary account leakage starts with recurring payments you don't show

Tapix enables banks to turn raw transaction streams into structured recurring payment intelligence with merchant identification, billing pattern detection and compliance-ready data.

The feature gap is driving deposit leakage

Customers don't leave. They leak. Clients rarely close their accounts. They start moving money to an app where managing it feels easier. Once enough recurring payments follow, primary status is gone.

As an incumbent bank, you have a key advantage: customers have their salaries paid into your accounts and use them to manage their regular bills automatically. If you also provide clear visibility and control over all recurring payments, you protect a relationship that fintechs cannot easily replace.

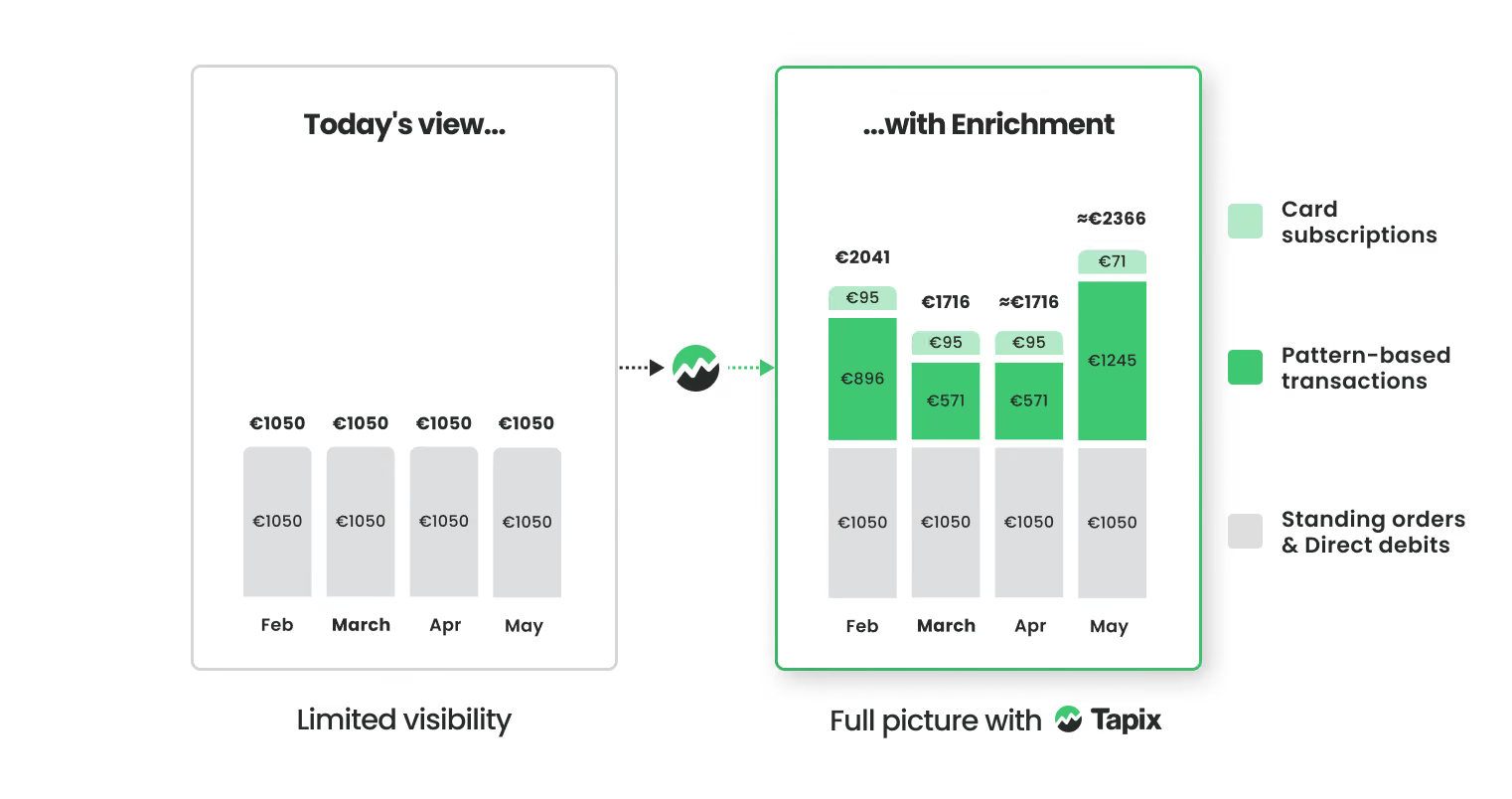

From a flat balance to the full recurring picture

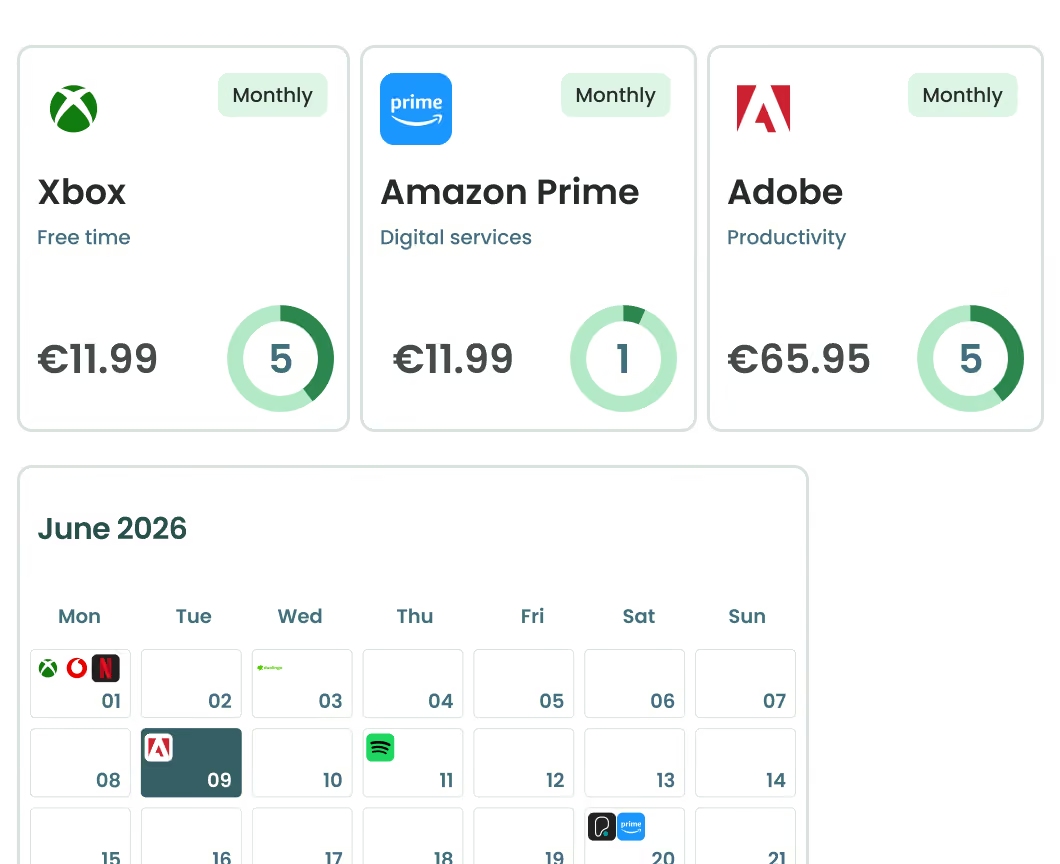

A flat monthly balance hides how much is really tied up in recurring payments. Tapix breaks it open, surfacing card subscriptions, pattern-based transactions, standing orders, and direct debits, so you and your customers see the true commitment behind every payment.

Turn recurring payments into strategic advantage

Tapix Recurring Payment Intelligence identifies and classifies every recurring transaction – subscriptions, direct debits, instalments, and standing orders – with pattern detection and continuously validated data.

Establish transparent recurring control

Pattern recognition gives you a complete, accurate view of what's truly recurring, not just the obvious subscriptions. You see what each customer is really committed to.

Protect Revenue and Strengthen Primacy

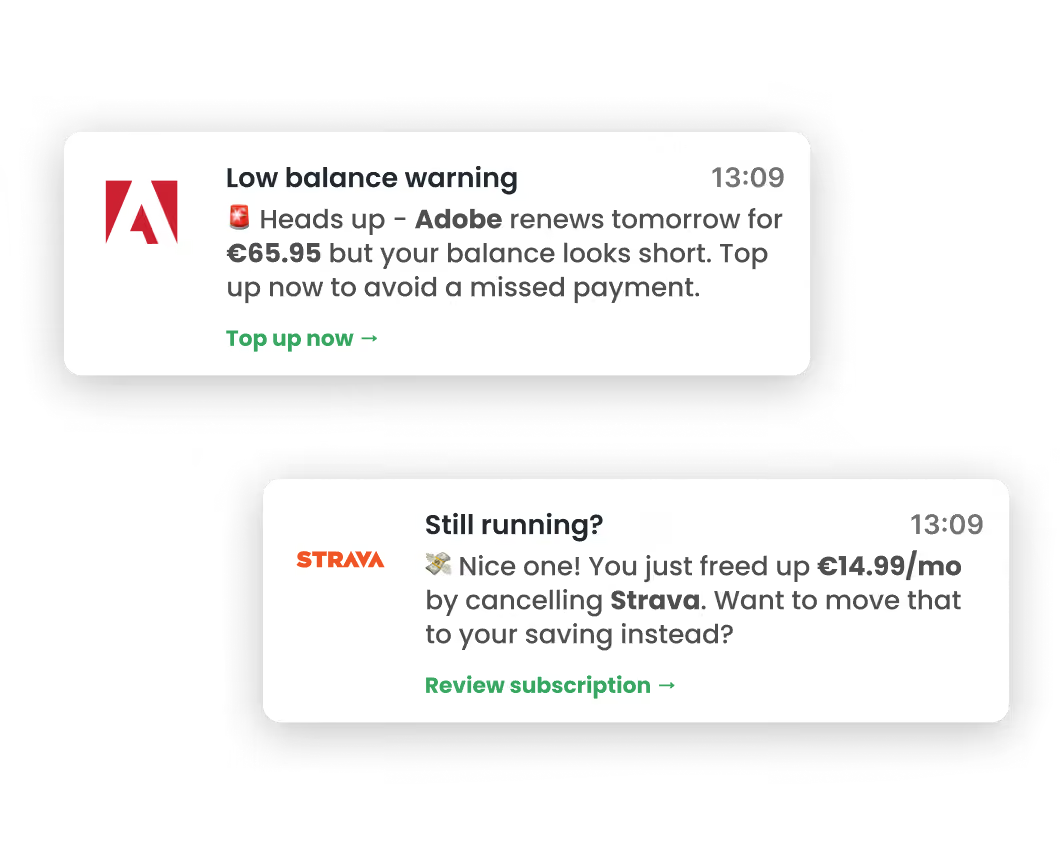

Knowing each renewal's date, amount, frequency, and whether it's automatic lets you act before a payment fails. Fewer declines, steadier deposits, and customers who keep you first.

Enable predictive financial intelligence

Recurring patterns make what's coming predictable. Act early, whether that's a payment about to fail or a subscription worth flagging.

Features are only as good as the data

Consistent, high-quality transaction data enables building a clear, scalable customer experiences across markets at production scale with:

What recurring payments enrichment unlocks?

Tapix helps elevate the transaction experience to the same level of excellence customers expect from Europe's digital leaders such as Revolut or bunq.

Deposits that stay put

Give customers a reason to keep managing money in your app. When recurring payments are visible, predictable, and easy to track, the incentive to open a second account drops.

Grow revenue and liquidity

Increase deposit stability and transaction income by helping customers stay ahead of upcoming charges.

Build trust and financial confidence

Deliver transparency and control over subscriptions to reduce surprises, improve satisfaction, and lower churn to digital-first competitors.

Unlock monetisation and intelligence

Leverage structured recurring payment behaviour to gain a complete view of the customer for business opportunities.

Built for enterprise architecture teams

.webp)

.webp)

.webp)

.webp)

Tapix operates as a structured data enrichement layer delivered via secure API integration. Review the detection logic, data attributes, integration patterns, and security approach in the technical overview.

Péter Vouszka

Head of Digital Banking at OTP Bank

Recurring payment detection FAQ

Frequently asked questions about how Tapix detects subscriptions, direct debits and recurring payments from transaction data.

Yes. We identify recurring payments across all payment types — not just cards (Visa, Mastercard). That includes bank transfers (standing orders, direct debits) and pattern-based recurring charges with no auto-renewal, like highway tolls and transport coupons.

No. Network data fields can carry errors, so we don't rely on any single parameter. Instead, we combine multiple data approaches with human review and internal expertise to maximize accuracy.

Yes. Card-on-file and recurring payments are two different ways of looking at a customer's payment commitments. You can read more abput concepts regarding subscription managment in our article here.

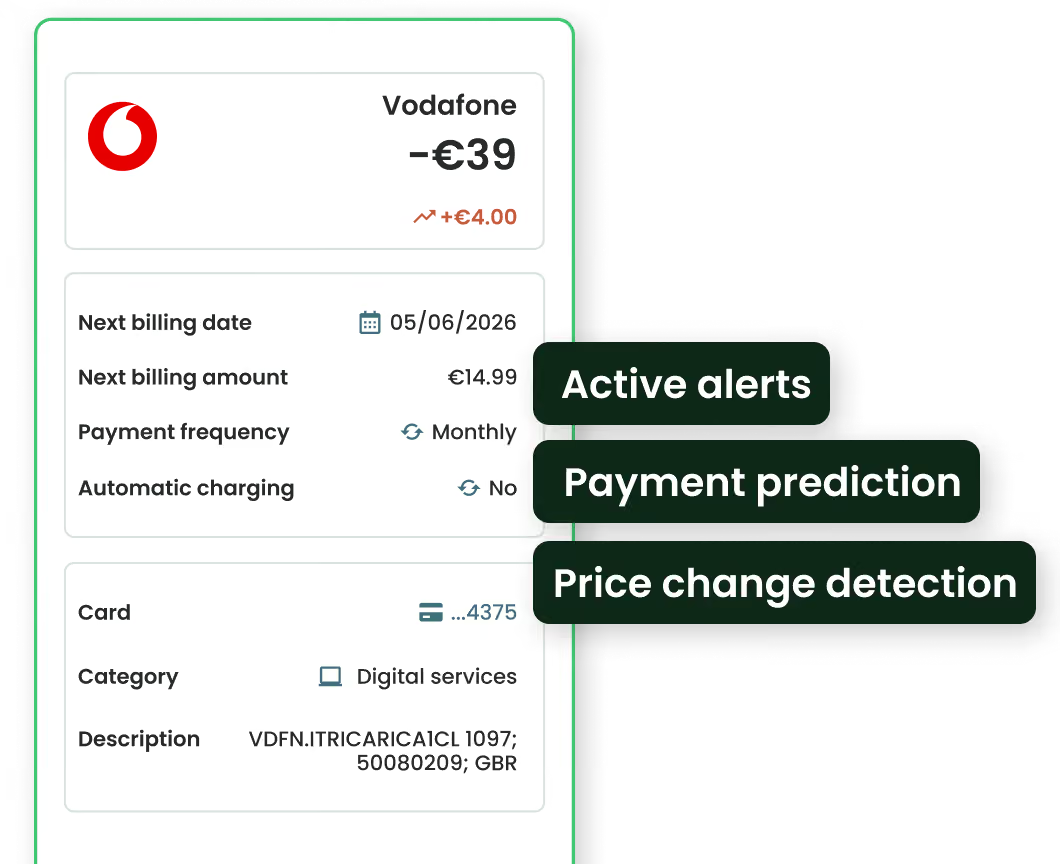

For each recurring payment we return: frequency, next billing date, next-amount type (same, approximate or unknown), and an automatic-charging flag. It’s the perfect data set for building advanced subscription dashboards.

It turns a passive statement into a planning tool. Showing what's coming lets you warn on low balance before a renewal fails, cut surprise "friendly-fraud" disputes, and position the bank as the customer's planning partner.

Yes. Once we identify a transaction as recurring, we add the predicted next billing date and amount indication directly to it — so you can surface upcoming charges to customers before they happen.

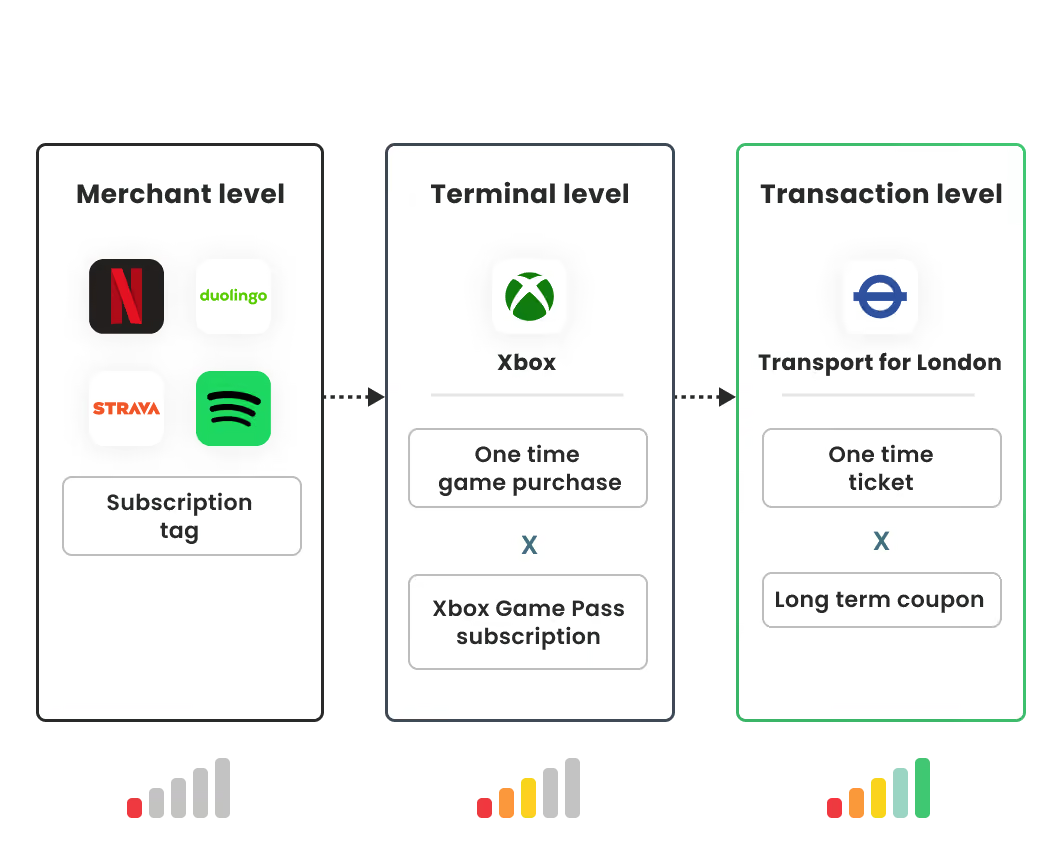

We separate them by pattern, not by merchant. Take YouTube: one transaction might be a one-off movie rental, another a recurring YouTube Premium subscription. We assess each transaction on its own behaviour, so mixed-billing merchants are handled correctly.

From our own database. We don't depend on direct connections with merchants or on any single data-message field — the intelligence is built and maintained entirely on our side.

Both. Covering the top global brands (e.g., Netflix, Spotify) is the easy part; our focus is granular, market-by-market coverage. On a single market we typically see hundreds to thousands of merchants offering different billing plans, and we work to capture them all.

Little to none for known merchants. Because coverage is cumulative and shared across clients, once a merchant is established in our database we recognise it for you — often from an early charge, without waiting for your own repeat pattern. Only a merchant that's brand-new to us needs a second sighting.

Continuously. We run regular updates and data-quality controls on a daily basis, so new merchants and refreshed information flow through to all clients automatically.

No — that typically sits with your payment processor. We can share best practices from integrations we've already supported. Keep in mind that blocking a payment isn't the same as canceling a subscription. To actually cancel, customers need to go to the merchant's site. You can make this easy by redirecting them using the merchant URLs Tapix provides.

The Visa mandate has two parts: listing and blocking subscriptions. We fully cover the listing side and help you build blocking together with your payment processor. But the mandate is only the floor — there's far more opportunity to build a great product on top of the minimum Visa requirements.

See Tapix in action

30-minute walkthrough with a live demo tailored to your business model and transaction data. See how Tapix turns raw payment records into real inputs using sample data that reflects your real-world scenarios.