Digital banking in 2026 will be defined by tighter regulation, higher UX expectations, cleaner data structures, and the slow disappearance of card-centric logic. Banks that treat data quality and transaction clarity as their core product layer move faster than institutions that still operate through legacy feeds and fragmented interfaces.

The trends below reflect real product movements rather than speculative predictions.

1. Transactions as the primary interface

Modern banking apps are now the front door to the entire banking experience customers are used to. Yet many banks that still anchor their apps around static dashboards, hidden menus or non-interactive balances. Digital-first players recognise that every financial action originates in the transaction feed: budgeting, challenges, categorisation, saving triggers, subscription reviews, dispute flows, carbon footprint estimation, fraud detection and expense claims all begin with a purchase.

Revolut illustrates this shift well. The home feed is a behavioural landing page: transactions dynamically pull in wealth summaries, category distribution, upcoming recurring charges and spending alerts. Users also choose how many transactions they want displayed, turning the feed into a genuinely customisable component rather than a passive list.

Did you know? According to SDK.finance, 39 % of people worldwide now use a banking app as their main way to manage money, with over 3.6 billion online banking users globally.

This change raises the stakes for transaction clarity. Any unclear merchant name, duplicate, miscategorised payment or missing logo interrupts the entire UX layer because the feed is now the primary navigation model. And banks need to keep up.

2. Customisable dashboards are a new default

As transactions move further onto the home screen, users want more control and personalisation. To be precise, more than 70% of customers expect more personalised experience, The Harris Poll says. As such, banks are increasingly expected to allow users to tune:

- Number of visible transactions

- Density vs simplicity of the dashboard

- Whether financial insights appear inline or collapsed

- Widgets such as savings goals, net-worth evolution or subscription summaries

- Visibility rules for sensitive categories (e.g., gambling, health)

As always, Revolut leads by example: users can modify the length of the feed, collapse insights and reorder components to reflect their financial behaviour. This adaptive model reflects a broader principle: the app should fit the user’s life stage, not the other way around.

.webp)

Banks that ignore customisation tend to overload their dashboards with boring, one-size-fits-all modules that do not reflect the real users’ behavioral models. For 2026, the interface must behave like a configurable workspace rather than a fixed list of numbers.

3. A2A payments, Wero and the wallet-centric model

The European market is undergoing a structural transition from card-dominated payment rails toward account-to-account schemes and interoperable wallets.

These are three main reasons for this shift:

- Regulatory pressure (PSD3, PSR) favouring standardised A2A flows

- User familiarity with wallet-based navigation (Apple Pay, Google Wallet, local wallets)

- The emergence of Wero as a multi-country P2P and C2B platform that provides a unified alternative to fragmented local schemes

Merchant adoption of instant payments is rising, and users increasingly manage spending inside wallets rather than card interfaces. For banks, A2A reduces cost of acceptance, simplifies dispute logic and unlocks cleaner transaction metadata.

Did you know? Through a partnership with the EuroPA alliance, Wero now covers 15 European countries and a potential base of over 382 million citizens, positioning it as a strong alternative to global card and wallet giants.

Wallet-centric UX also improves sensitive categories such as gambling: transaction-level clarity, spend caps and real-time introspection become significantly easier when the payment does not disappear into vague card acquirers.

4. Enriched transaction data becomes a mandated minimum

Visa’s Enhanced Merchant Data is joining Mastercard’s AN4569 mandates to push enriched transaction data from a mere advantage to an actual compliance baseline that is expected globally.

Tapix helps banks meet Visa’s Enhanced Merchant Data requirements and Mastercard’s AN4569 standards simultaneously by enriching transactions with richer merchant identity and context. Instead of raw descriptors, Tapix provides clean merchant name, logo, accurate category, and location consistency so transaction clarity becomes an enforceable baseline. This same enrichment layer also powers real in-app features banks are now expected to ship, such as Eco Track CO₂ insights and ATM Nearby discovery, without patching together multiple vendors or unreliable datasets.

With Tapix-enriched transaction-level data, banks can:

- Meet Visa + Mastercard enhanced merchant data standards at scale

- Standardise categories beyond MCC codes for reliable PFM and dispute clarity

- Deliver Eco Track carbon footprint views per transaction and monthly impact summaries

- Add ATM Nearby maps with fees, opening hours, and practical cash-access guidance

Mandates directly influence:

- Merchant naming standards

- Merchant logos

- Category accuracy

- Location consistency

- Subscription identification requirements

Banks must now ensure that the naming displayed to users is clear and accurate. Raw strings like “DRIAT 00219 PAY*” are no longer acceptable, not because of UX preference but because they break core regulatory expectations around clarity and dispute understanding.

The next step is recurring-payment intelligence: banks must identify subscription patterns early, accurately and consistently, especially given proposed EU rules on subscription transparency and cancellation simplicity.

All of this depends on the quality of the merchant-identification layer. Without enriched and normalised data, banks cannot comply, cannot sustain AI features and cannot deliver reliable dispute flows.

5. CO2 tracking becomes a product feature

Sustainability has moved into the core product roadmap. Customers now expect banks to show the real impact of their spending patterns.

Raiffeisenbank Czech Republic is a good example. In collaboration with Tapix, the bank integrated Eco Track into its mobile banking, displaying merchant-level carbon footprint estimates to more than 1 million active mobile users. The project was recognised as a Game Changer for sustainable banking and responsible finance.

Eco Track turns high-level ESG commitments into something tangible in the app:

- Each transaction receives an estimated CO2 footprint at merchant level

- Customers see the impact of lifestyle choices over time

- Banks can connect green products, such as sustainable cards or loans, directly to real spending behaviour

With this natural integration, Eco Track becomes a real-time feature that influences how people spend, save and choose products, while positioning the bank as an active partner rather than a passive reporter.

6. Telcos, banks and super-app logic

The boundaries between banking, payments and connectivity are disappearing. In Europe, several premium banking packages already include eSIMs, roaming bundles or global data access. This reflects a shift to treating connectivity as part of the financial-service stack.

.jpg)

At the same time, in Asia and parts of Africa, telcos and digital wallets are entering lending, savings, credit scoring and merchant services. The direction is the same: a service hub where payments, digital identity, telecom utilities and financial features interlock.

This does not mean Europe will suddenly adopt a formal “super-app,” but the path is already visible. Banks add travel connectivity, wallets add credit and telcos add payments. The 2026 product reality is convergence without formal declarations.

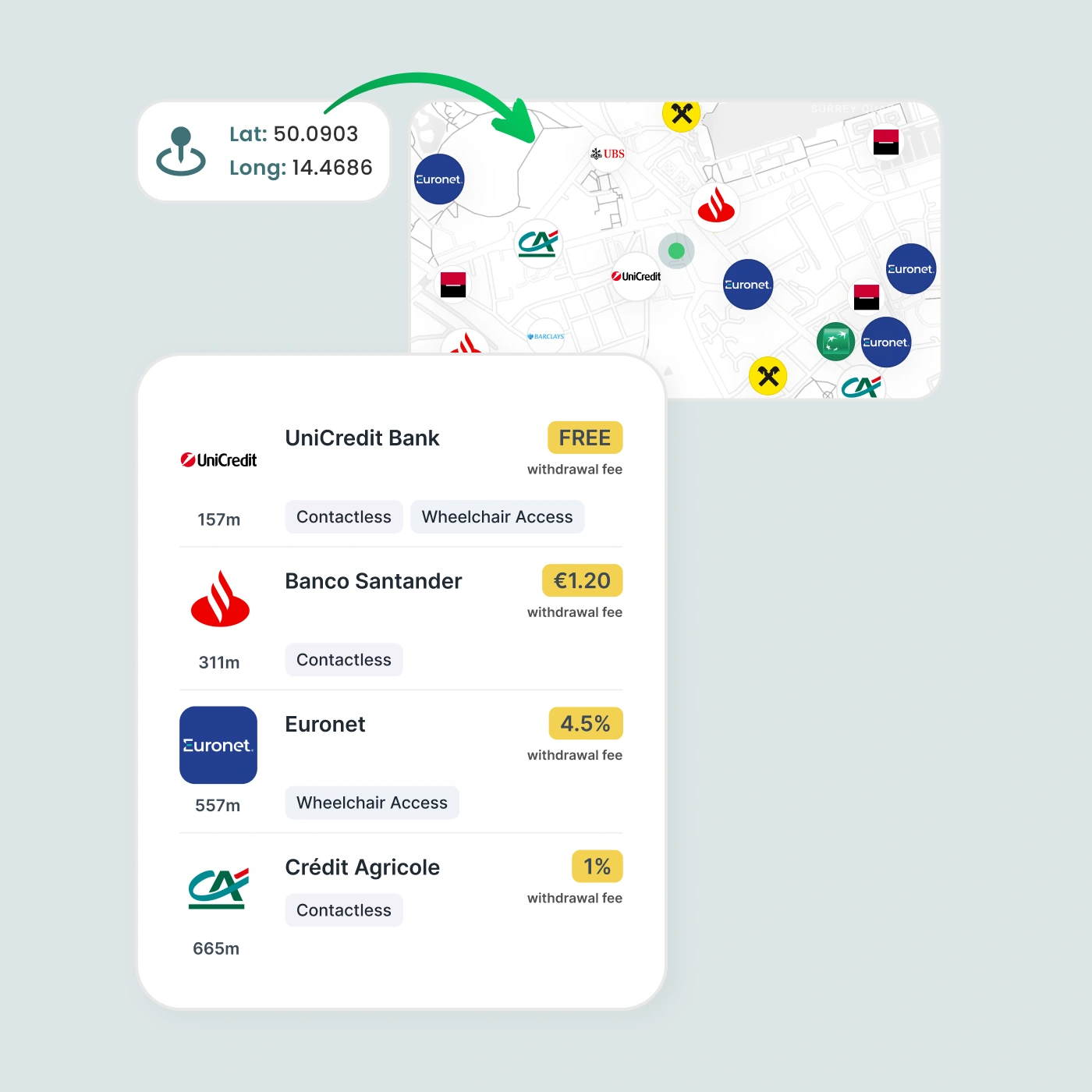

7. Cash remains relevant with ATM locators

Despite growth in digital payments, cash continues to play a strong role, especially in segments such as travel, SMEs and older demographics. Banks that treat cash access as an afterthought create unnecessary friction for otherwise digital customers.

Two things change in 2026:

- ATM discovery becomes an in-app feature

- New players reimagine ATM design and functionality

Revolut’s branded ATM rollout in Spain is a visible example. The company is deploying 50 machines in Madrid and Barcelona with plans to reach around 200 ATMs across Spanish cities before expanding to other European markets from 2026 onward. These ATMs are integrated with the app, support fee-free withdrawals for Revolut customers and even dispense physical cards, narrowing the gap between digital onboarding and offline usage.

For other banks, there is also an option to enrich their own app with a feature like ATM Nearby, which includes interactive maps with fees and opening hours, or clear rules on withdrawal limits and currencies.

Cash access becomes another touchpoint where data, UX and physical infrastructure meet.

8. Sponsorships move to product-led branding

Financial institutions are abandoning sponsorships that live solely outside the product. The new standard is integration: the partnership must show up inside the banking app with benefits tied to actual product usage.

Modern sponsorships include:

- Card-linked discounts

- Access perks (events, travel, rentals, loyalty tiers)

- Dynamic merchant branding inside transactions

- Exclusive experiences unlocked by payment behaviour

- Co-branded card editions

- In-app onboarding flows linked to the sponsor

Revolut’s partnerships in automotive, sports and lifestyle categories follow this path. Brand value is now measured by in-app engagement and activation volumes.

Did you know? According to BrandFinance, 91 of the 100 most valuable banking brands globally already invest in sports sponsorships to build brand equity and reach new audiences

9. Kids banking and Gen Z as a strategic segment

No more waiting until customers are 18. Banks that want to stay ahead now build relationships through each of your life cycles since dedicated kids and teen products have become a core growth and lifetime-value strategy.

Did you know? In 2024, GoHenry users earned £280 million in pocket money, with an average of £9.62 per week per child

Many products follow this demand:

- GoHenry pioneered the paid kids-banking model in the UK and US

- Starling Kite offers a free debit card and app for 6–15-year-olds, with parental controls and gambling-merchant blocks by default

- Revolut Kids & Teens provides accounts for ages 6–17, with in-app controls for parents and teen-initiated onboarding in some markets

- bunq offers high-interest child savings accounts (up to about 2 % p.a.) and goal-based saving features designed specifically for kids

- Kard in France focuses directly on teen accounts and family supervision, with over 200,000 families onboarded

Traditional banks are also building structural mechanisms to connect with Gen Z. Česká spořitelna’s Future Mindset Board selects six people under 30 from almost 2,500 applicants and involves them directly in shaping the bank’s strategy. Raiffeisenbank, in parallel, uses research, youth-focused campaigns and advisory initiatives such as NextGen Squad and financial-literacy partnerships to involve younger customers and understand their expectations of mobile banking.

Kids and teen banking is now a serious product category. It monetises the full lifecycle, from the first pocket-money card through student accounts to adult credit and investments, with transaction data forming the thread that connects each step.

10. Cards transform into strategic brand surfaces

Even as digital payments dominate, physical cards remain one of the strongest physical brand expressions. For neobanks with no branches, the card is the only tangible object the customer ever sees. It becomes a critical symbol of identity and trust.

Fintech Branding Studio analysed 25 leading neobank cards and shows how design choices are used deliberately to communicate brand strategy:

- Vertical orientation that matches mobile-focused layouts

- Ultraminimalistic face with no printed numbers

- Premium materials (steel, matte composite, translucent polymers)

- High-contrast or signature colours as brand identifiers

- Limited-edition designs tied to sponsorships or cultural events

- Embedded textures or surface effects for tactility

This reflects a shift in brand philosophy: the card is not a functional payment tool - it is a brand artifact that extends digital identity into the real world. Strong card design reinforces perceived reliability, premium positioning and emotional attachment. And for digital banking, emotion is everything.

What to know more? Go beyond banking with us!

In 2026, digital banking is no longer just about “having an app” but how intelligently that app turns transactions, data and partnerships into everyday value for its users. The institutions that win will be those that treat enriched payment data as their core infrastructure to power clear transaction feeds, configurable dashboards, instant A2A flows, sustainability insights, AI assistants and product-led sponsorships.