Withdraw cash from the wrong ATM in central Prague and you can pay tens or hundreds of crowns more than you should. Independent operators like Euronet apply withdrawal fees that vary by card type and country of issue, with foreign cards consistently charged the most. The fees are not the only problem - it's the density of these ATMs and the lack of clear information about them that turns an ordinary cash withdrawal into a costly guessing game.

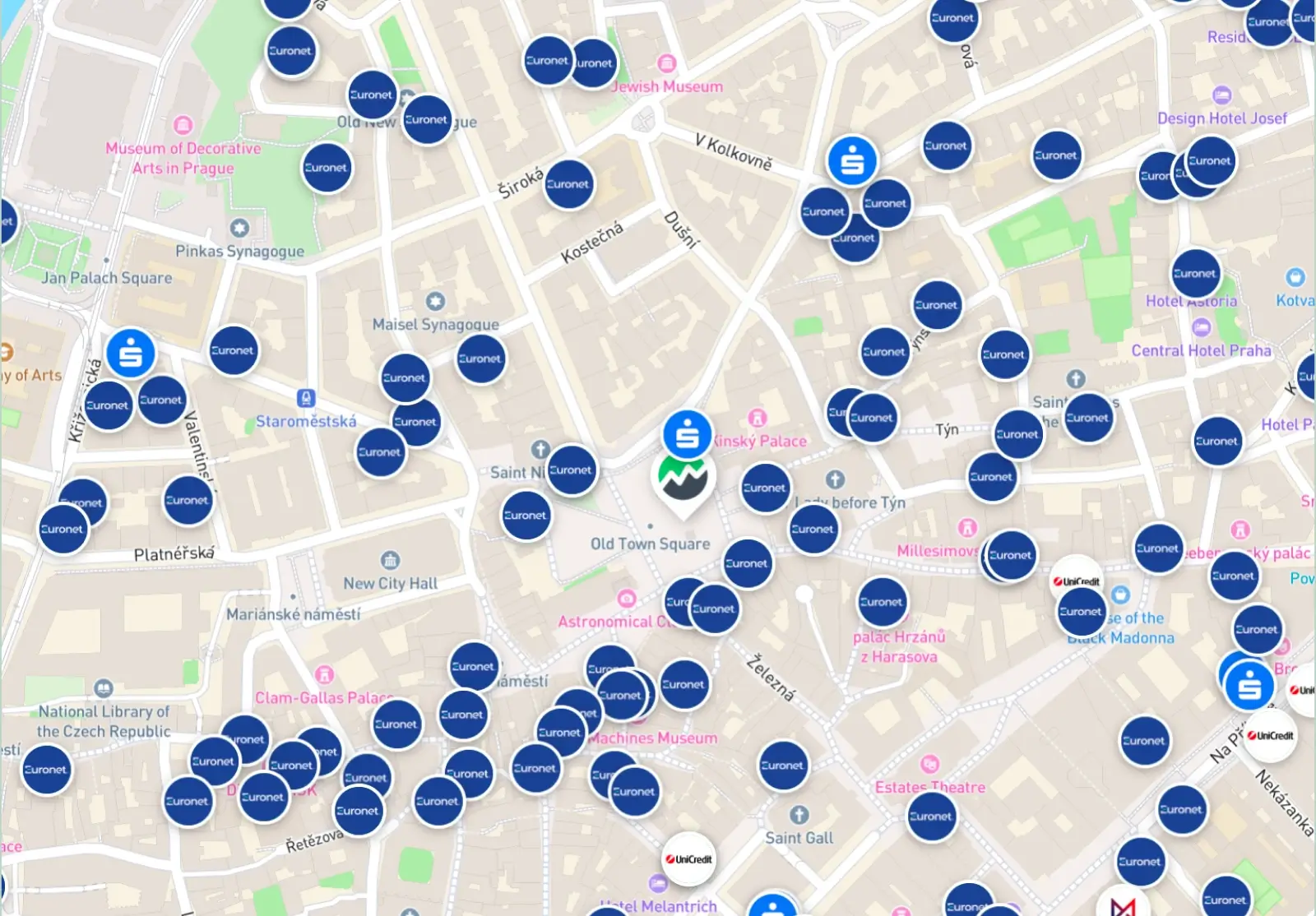

According to our data, Euronet operates 718 of the 1,605 ATMs in Prague - roughly every second machine in the city. The concentration is dramatically higher in transit hubs and tourist zones: at Prague’s main train station, non-bank ATMs make up 87% of all available machines, and in the historical centre, more than 63%. For a visitor stepping off a train with no time to compare options, the chance of landing at an independent ATM is overwhelming.

A pattern that repeats across Europe

The Prague picture is not unique. ATM network composition varies sharply by country, and that structure largely determines what users experience at the moment of withdrawal.

"The structure of ATM networks differs significantly depending on who operates the infrastructure, and so does the user experience," says Ivan Dovica, co-founder and co-CEO of Dateio, the company behind Tapix. "In Great Britain, where ATMs are operated by banks, retailers, and specialised operators, independent ATMs make up 75.6% of the entire network in London. The opposite example is the Netherlands, where ING, ABN AMRO, and Rabobank merged their ATMs into a joint network called Geldmaat. In Amsterdam, independent operators make up only 20.5%."

The implication for banks is straightforward: the chance that a customer travelling abroad will end up at an unfavourable ATM depends almost entirely on the country they happen to be in. Without information delivered inside the banking app, that risk is invisible to the user until the fee appears on the statement.

Dynamic currency conversion: a second layer of cost

Beyond the withdrawal fee itself, foreign-card users run into dynamic currency conversion (DCC). The ATM offers to convert the amount into the card's home currency using its own exchange rate - typically less favourable than the rate the user's bank would apply.

Bank-operated ATMs tend to handle DCC transparently, giving the user a clear option to decline and withdraw in local currency. Independent operators offer DCC aggressively and often present it as the only path to complete the withdrawal. Euronet, for instance, charges what it calls a "conversion fee" on top of the standard withdrawal fee, and the exact amount or the rules for applying it are difficult to find even in the operator's customer support pages.

For someone withdrawing on a foreign currency card, the combined effect can push the cost of a single transaction up by as much as 12%.

Missing and unreliable information about ATM features

Cost is only part of the story. Even basic information about what an ATM offers, such as contactless withdrawals or barrier-free access, is incomplete or wrong across the data sources most people rely on.

In Prague, 15% of machines advertise contactless withdrawals, but Tapix verification confirms only 87% of those claims. The discrepancies are sharper for accessibility data: advance information on barrier-free access is available for only one in ten ATMs in the city, and of those, only 63% are actually accessible in practice. A wheelchair user planning a withdrawal based on publicly available maps stands a roughly one-in-three chance of arriving at a machine they cannot use.

What banks can do about it

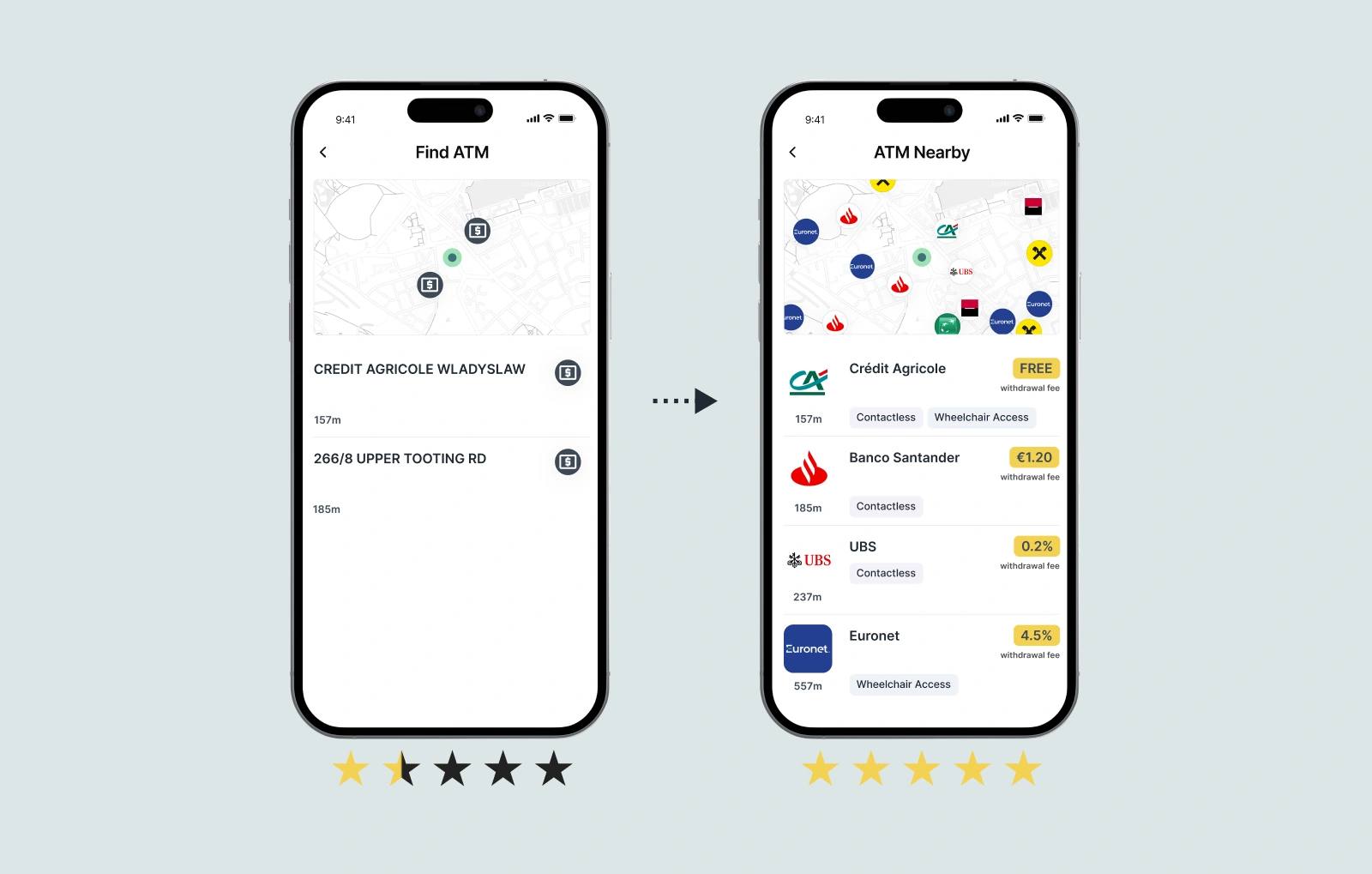

The information that would protect users exists. It is simply not consolidated, verified, or surfaced where users need it: inside their banking app, at the moment they're looking for a place to withdraw cash.

Tapix's ATM Nearby module addresses exactly this gap. Rather than relying on static maps or a single operator feed, it aggregates inputs from nearly 400 sources in real time - official bank lists, operator networks, card schemes - and runs them through a verification and cleaning process that eliminates duplicates and non-existent machines.

For each ATM in the user's vicinity, the service surfaces:

- Location, distance, and current operational status

- Operator and expected fees (including for independent operators that charge more)

- Support for contactless withdrawals

- Barrier-free access, verified rather than self-declared

- Opening hours

The service covers ATMs across nearly all of Europe and extends to Singapore, Dubai, Colombia, and Egypt - the destinations where local equivalents of Euronet are hardest for an ordinary traveller to recognise. Raiffeisenbank was the first bank on the Czech market to integrate it into its app.

Cash transparency as a competitive feature

ATM transparency is not yet a standard banking app feature, which is precisely why it differentiates. The banks that integrate verified ATM data signal something specific to their customers: that the bank's interest aligns with theirs, even when the user is withdrawing money outside the bank's own network.

For banks weighing where to invest in app features, the value calculation is straightforward. Cash withdrawals abroad are a known friction point, the data to fix it already exists, and integration is a simple back-end exercise.